Fund managers are hoping that South Korea can take a leaf out of Japan’s book and implement corporate governance reforms to close the ‘Korea discount’.

Corporate governance reforms have brought Japan’s 20-year bear market to an end and propelled its stock market to all-time highs. Now fund managers are wondering whether a similar phenomenon could happen in nearby South Korea, where poor corporate governance has led to an entrenched ‘Korea discount’.

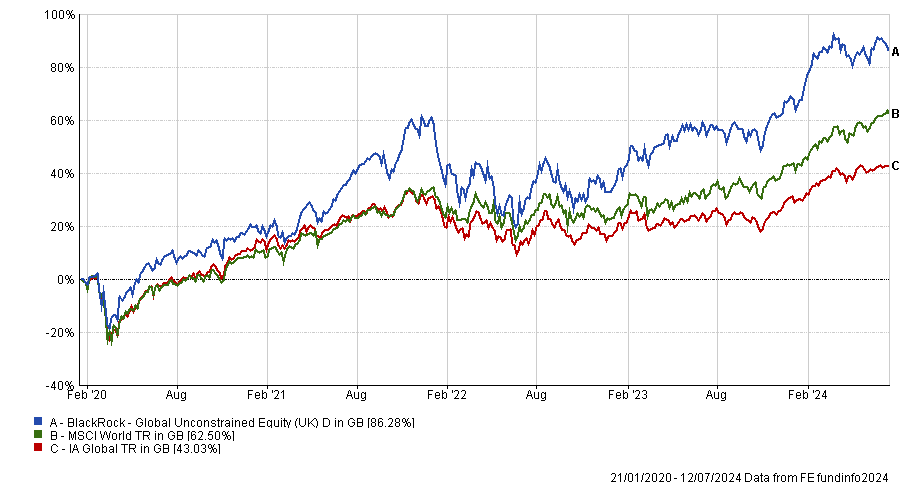

Korean management teams have not historically given much thought to capital efficiency and balance sheet management, said Ben Preston, head of Orbis Investments’ global sector research team, but “they’ve looked across the water to Japan” and seen a rising stock market and international investors pouring money into Japan’s economy.

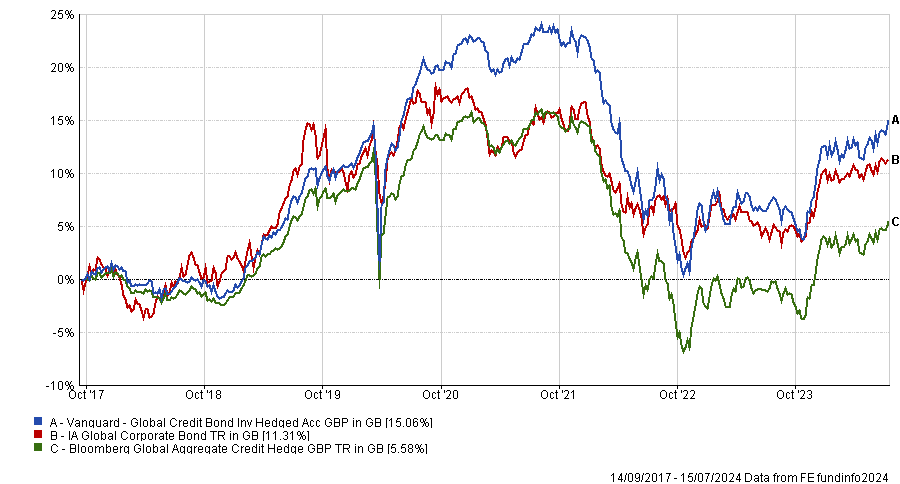

Performance of Korean and Japanese equities vs global over 10yrs

Source: FE Analytics, performance in sterling terms

South Korea’s Financial Services Commission introduced the Value Up program on 26 February 2024 to encourage companies to voluntarily improve their corporate governance standards and transparency, and to better align the interests of controlling and minority shareholders. These measures aim to “unlock hidden value”, Preston said.

Elli Lee, a portfolio manager at Matthews Asia, said the Value Up program is “far-reaching” and “ambitious”, but shareholders are disappointed by the voluntary nature of its proposals.

“Most shareholders were hoping for stronger enforcement and for other reforms including stricter fiduciary responsibility for boards of directors and even a lowering of inheritance tax, which is seen by many as a key reason why South Korea’s large corporates are reluctant to improve capital efficiency and shareholder value,” she explained.

About 90% of companies in Korea have controlling shareholders that prioritise their own interests at the expense of minority shareholders, said Jonathan Pines, lead portfolio manager of Federated Hermes’ Asia ex-Japan strategy.

For instance, “when a founder of a company dies in Korea, the stock price generally rockets”, he said. Prior to that, controlling families have an incentive to depress the share price to minimise inheritance tax, which in Korea is 60%.

As another example, the ex-wife of SK Group’s chairman was awarded a huge divorce settlement a couple of weeks ago and the company’s stock price rose in reaction.

Both of these anecdotes “tell the same story – that it is within the power of directors to raise share prices and they don’t do it. It tells you in South Korea that something is broken and you get all these strange side effects as a result,” Pines explained.

As part of Value Up, financial authorities have proposed revising the Commercial Act to make corporate directors responsible for protecting minority shareholders’ interests. If this is enacted, Pines thinks it would be a game changer, but there has been heavy resistance from the Chaebol (large industrial conglomerates controlled by a single family).

Meanwhile, “a huge number of companies are trading on very cheap price-to-earnings multiples,” Pines said. Some smaller companies are trading well below net cash, “which is crazy because the company could pay the entire market cap as a dividend”.

Non-voting common shares are on a 75% discount to common shares (whereas in the US, the average discount is about 2%).

As a value-oriented fund manager, “you see all these amazing things and you think, I’m going to make a fortune in this market because there’s incredible value”. However, he warned that Korea could be a value trap because the ‘Korea discount’ has persisted for a long time.

Despite Pines’ reservations, his Asia ex-Japan strategy has progressively built up an 18% overweight position in Korea versus its benchmark. “We’ve never been this overweight Korea,” he said.

The fund has an equally large underweight to India, which has “a great top-down story” such as favourable demographics and economic growth, but is “the most expensive market in the world,” he said. “Korea is the opposite. The market is rewarding India too much and penalising Korea too much.”

Valuations are so cheap in South Korea that Pines believes the potential upside outweighs the downside risk. “If a stock is trading below cash, we think to ourselves, we can’t really lose,” he said.

There are plenty of catalysts. Since the Covid pandemic, the number of Koreans owning shares has increased dramatically to about half the population, so more people are interested in share prices and are pushing for reforms.

Preston argued that Value Up could spur a gradual stock market recovery so, in addition to South Korea’s attractive valuations, “you’ve got change in the air”.

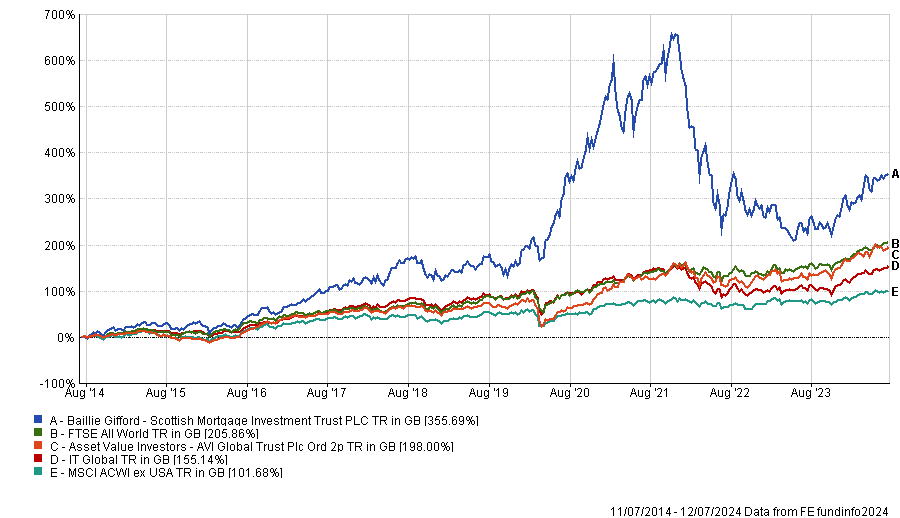

The Orbis Global Equity fund had about 15% in Japan a year ago but has taken profits and built a 15% position in Korea instead. Orbis owns several Korean banks – the one industry not dominated by controlling shareholders. As such, it has outperformed other sectors, but valuations are still attractive with several banks trading at half their book value. They are priced as if “something terrible is going to happen”, Preston said.

Orbis owns KB Financial Group, which he said is “the biggest and the best”, as well as Shinhan Bank, Hana Bank and Woori Financial Group.

South Korea also has a thriving tech sector with Samsung Electronics, SK Hynix and Micron all making memory chips. Orbis owns Micron and has exposure to SK Hynix.

Orbis and Hermes both hold Samsung Fire & Marine Insurance, whose management is “amenable to doing the right thing,” Pines said.

Why investors ignore Asia at their peril…

June ushered in the eighth consecutive month of net inflows into emerging market funds, with Asia (ex-China) taking the lion’s share. So why have investors been adding Asian equities to their buy lists? Well, recent performance has certainly played its part, with the MSCI Asia Pacific Index chalking up a healthy total return of almost 9% in sterling terms, in the first half of 2024.

But this ignores the bigger picture: put simply, the region is becoming increasingly difficult to ignore. It is home to around 60% of the world’s population and generates almost half of the world’s GDP (on a purchasing power parity basis). And it’s the growth story in particular that has been grabbing the attention of investors, with Asia forecast to generate more than twice the GDP growth of the G7 countries, thanks to three key mega-trends.

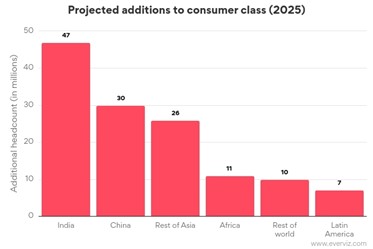

The first is the shift in the global consumer class from West to East. Asia has been the primary driver of growth since 2000 and India is forecast to contribute more to the newly-minted consumer class than Africa, Latin America and the rest of the world combined in 2025, as shown in the chart below.

This burgeoning middle-class will drive a significant increase in domestic consumption, enabling economies to reduce their dependence on export-led growth and proving a boon for consumer products firms such as Samsung, Toyota and JD.com.

Source: The World Consumer Outlook 2025, World Data Lab

Next on the list is the ‘re-shoring’ trend, prompted by the disruption to supply chains during the pandemic and ongoing geopolitical tensions, with Vietnam, Malaysia and Thailand benefiting from this so-called ‘China plus one’ strategy. And as a key supplier of nickel to electric vehicle manufacturers, Indonesia has demonstrated its ability to maintain strong relations with both the Chinese and North American markets.

Finally, Asia is well-positioned to ride the tailwinds of the net-zero transition and roll-out of artificial intelligence (AI). China is a global leader in clean energy and installed as much solar power as the rest of the world combined in 2022. It is also a leader in battery cell manufacturing and home to a booming electric car industry, with China accounting for nearly 60% of new car registrations in 2023, according to the IEA.

And on the AI front, Asia boasts the largest semiconductor foundry in the world in TSMC (which supplies Nvidia, Apple and Advanced Micro Devices, amongst others) and is tapping into soaring demand for chips as the ‘picks and shovels’ of the AI revolution.

In fairness, it has not been all plain sailing, with Japan only recently emerging from its ‘lost decades’, a prolonged period of economic stagnation, and China continuing to grapple with structural issues. That said, the broader macroeconomic backdrop is supportive as Asian economies haven’t faced the inflation-led macroeconomic problems of the West, nor their record levels of public debt.

However, treating the region as a homogenous unit ignores one of its key selling points as a diverse universe of sectors and countries, from the more mature economies of Singapore and Hong Kong to their high-growth neighbours in India, Thailand and Indonesia. Valuations also look relatively undemanding, with the MSCI Asia Pacific Index trading on a forward price-to-earnings ratio of 14.2x, some 30% below that of the MSCI World Index (as at 28 June 2024).

The investment case for Asia may be compelling but it is worth acknowledging the challenge for retail investors due to the breadth and complexity of the region, together with a relative lack of equity research. One option is an actively-managed Asian fund that provides a ready-made, diversified portfolio created by managers with the expertise to exploit pricing opportunities in relatively inefficient markets.

One such example is Schroder Asia Pacific, which is managed by Richard Sennitt and Abbas Barkhardor, who have a combined experience of nearly 50 years working in Asian and emerging markets teams at Schroders. They are supported by the 40-plus strong Schroders research team based in six offices across the region.

The managers are bottom-up stock pickers, aiming to hold a portfolio of around 60 ‘quality’ companies with sustainable earnings, sound balance sheets and good corporate governance. The trust’s tilt towards Taiwan and India has helped to drive superior returns, delivering a one and five-year total net asset return of 13% and 31% respectively (as at 12 July 2024).

Alternatively, investors looking for country-specific exposure could cast their eyes over Ashoka India. It is the top-performing trust in the AIC India & Indian Subcontinent sector over the past five years, with a net asset value total return of 160%, with recent performance boosted by its overweight position in small and mid-caps.

Japan continues to be among the top-performing countries and Schroder Japan aims to deliver capital growth from a diversified portfolio of around 60-70 companies. The trust has achieved a five-year net asset total return of 50% and recently announced an enhanced dividend policy with 4% of the average net asset value to be paid in dividends each year.

Due to its higher volatility, Asia is best suited for investors willing to take a longer-term view. However, given its ever-increasing dominance on a global scale, this may be an opportune time for investors to review their portfolio allocation: the sun may not be setting on the West but it is certainly rising in the East.

Jo Groves is an investment specialist at Kepler Partners. The views expressed above should not be taken as investment advice.

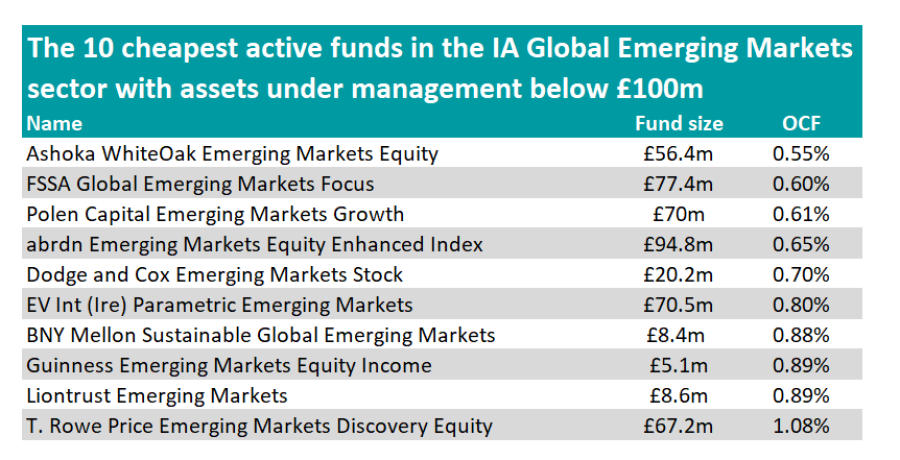

Trustnet researches the cheapest active funds in the IA Global Emerging Markets sector with less than £100m under management.

Small funds face fewer liquidity constraints than larger strategies, enabling them to explore less liquid opportunities.

Emerging market equities typically have a lower liquidity profile than developed markets, so a case can be made for choosing smaller funds.

However, higher fees are a common feature of smaller funds because they lack the scale to spread costs across a large pool of investors.

As such, Trustnet has found nine active funds in the IA Global Emerging Markets sector with less than £100m in assets and fees under 1%.

Source: FE Analytics

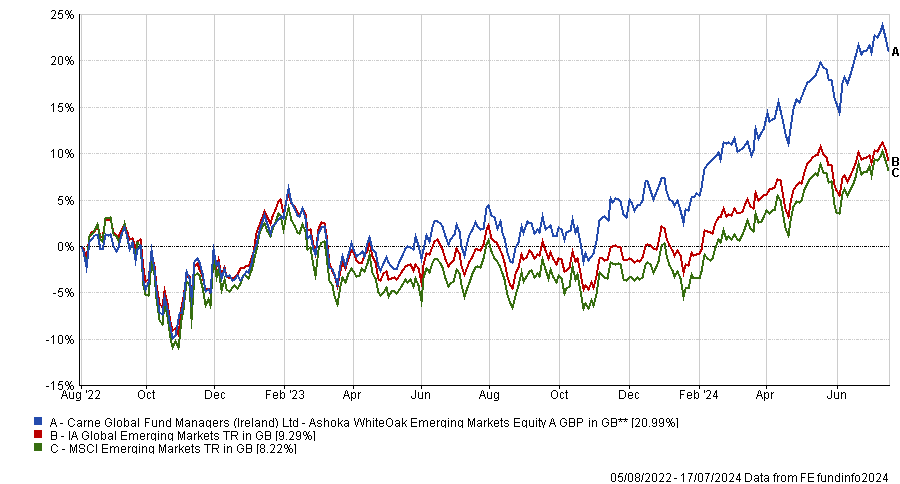

The cheapest small fund in the IA Global Emerging Markets sector is the $73.2m (£56.4m) Ashoka WhiteOak Emerging Markets Equity fund, which charges 0.55%.

The fund is relatively new, having been launched in 2022, building on the success of Ashoka India Equity, and is also available as an investment trust.

Manager Prashant Khemka and his team use a valuation framework called ‘OpcoFinco’, which enables them to analyse companies through the prism of return on investment capital and then to quantify the value of return on incremental capital.

Performance of fund since launch vs sector and benchmark

Source: FE Analytics

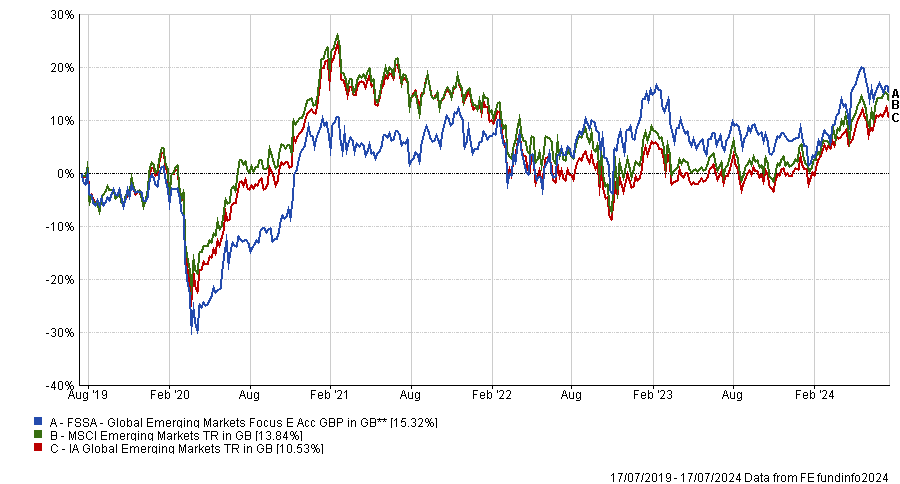

Next is the £77.4m FSSA Global Emerging Markets Focus fund, managed by Rasmus Nemmoe and Naren Gorthy, which charges 0.60%.

The fund follows a similar process to its peers in the FSSA range, employing a bottom-up approach with an absolute return mindset and an emphasis on quality and stewardship.

Analysts at Rayner Spencer Mills Research said: “The team looks for founders and management teams that have high governance standards and are well aligned with minority shareholders. These will be strong franchises with the ability to deliver sustainable and predictable returns comfortably in excess of the cost of capital.“

Performance of fund over 5yrs vs sector and benchmark

Source: FE Analytics

The fund sits in the second quartile of the IA Global Emerging Markets sector over five years and has been a top-quartile performer over three years.

In third place is the $90.8m (£70m) Polen Capital Emerging Markets Growth fund, which levies 0.61%.

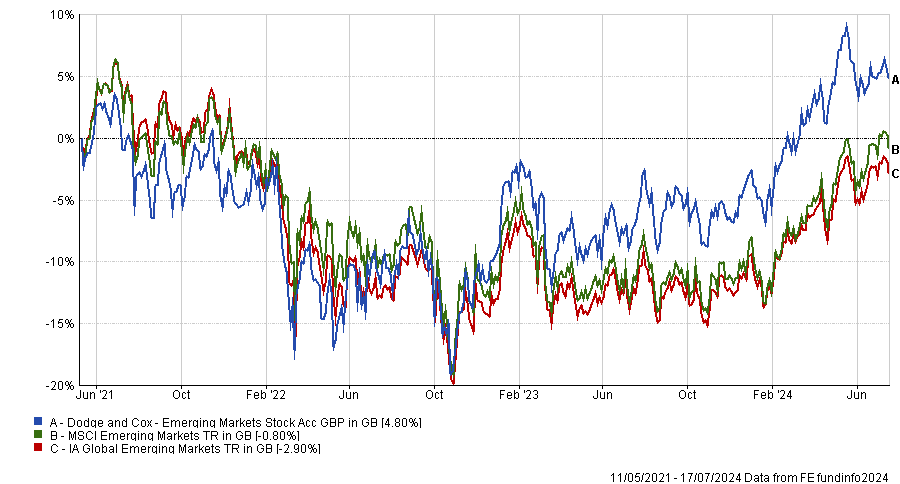

Another inexpensive minnow is the £20.2m Dodge and Cox Emerging Markets Stock fund. It follows Dodge & Cox’s house style of investing in stocks that appear to be temporarily undervalued by the market but have a favourable outlook for long-term growth.

It is also overweight small- and mid-caps relative to the benchmark and boasts an active share of 78.8%.

Performance of fund since launch vs sector and benchmark

Source: FE Analytics

While the fund has a short track record, having been launched in 2021, it sits in the top quartile of the sector over three years.

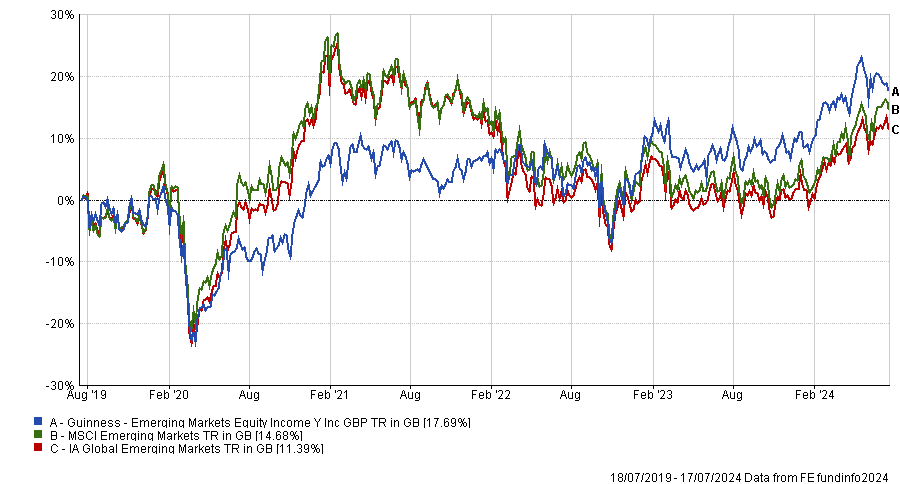

Finally, the £5.1m Guinness Emerging Markets Equity Income fund stands out in the list due to its income mandate.

Managers Edmund Harriss and Mark Hammonds aim to provide investors with exposure to dividend-paying businesses across emerging markets.

They focus on companies with a market cap of at least $500m (£385.4m) that have proven their ability to achieve higher returns on invested capital, are well positioned to continue doing so and are capable of growing their dividends.

Performance of fund over 5yrs vs sector and benchmark

Source: FE Analytics

The fund sits in the sector’s second quartile over five years but is a top-quartile performer over three years.

The government aims to boost pension pots for defined contribution scheme savers by £11,000.

Chancellor Rachel Reeves has launched a pensions review to increase defined contribution (DC) schemes’ investments in the UK economy, grow pension pots and tackle waste in the pensions system.

This new Pensions Bill, confirmed in the King’s Speech, aims to encourage defined contribution (DC) schemes to raise their domestic exposure by £8bn collectively.

As DC schemes are set to manage around £800bn in assets by the end of the decade, the government believes that even a 1% shift of assets into domestic investments could help grow the UK economy and build vital infrastructure.

Meanwhile, the government aims to increase pension savers’ pots by more than £11,000 through further consolidation of DC schemes and broader investment strategies to deliver higher returns.

The Pensions Bill also introduces a ‘value for money’ framework to promote better governance and higher returns for DC schemes.

This review will also examine ways to “unleash the full investment might” of the £360bn Local Government Pension Scheme (LGPS) and address the £2bn spent on fees.

Reeves said: “The review is the latest in a big bang of reforms to unlock growth, boost investment and deliver savings for pensioners..”

These initial plans are the first phase in reviewing the pensions landscape and will be led by pensions minister Emma Reynolds.

The Chancellor and the pensions minister will chair a roundtable with the pensions industry today to initiate industry engagement for the review.

Reynolds said: “Over the next few months the review will focus on identifying any further actions to drive investment that could be taken forward in the Pension Schemes Bill before then exploring long-term challenges to ensure our pensions system is fit for the future.”

So far, the pension industry has welcomed the government’s ambitions.

António Simões, group chief executive of Legal & General Group, said: “Driving pensions capital into areas such as science, technology and infrastructure can help support better returns for millions of retirement savers, as well as stimulate much needed long-term growth for the economy.”

Andy Briggs, chief executive officer of Phoenix Group, added that this review, especially the focus on pension adequacy, is “vitally important” as only one in seven people in the UK are saving enough for a decent standard of living in retirement.

The next phase, starting later this year, will explore additional steps to improve pension outcomes and increase investment in UK markets, including assessing retirement adequacy.

Additionally, the Chancellor will chair the first Growth Mission Board on Tuesday, supporting the government’s aim to achieve the highest sustained growth in the G7.

New measures have already been announced to fix the planning system, create a new National Wealth Fund and overhaul the listings regime to boost UK stock exchanges.

Investors confirmed their preference for global passive funds over the UK and active management.

Losing a few pounds just before the summer might be good for the beach but not necessarily for funds, especially if they are left skinnier by unsatisfied investors deciding to cash in and walk away.

FE fundinfo fund flows data covering the second quarter of 2024 shows a skinnier UK and an ever-fatter pool of global funds – particularly index trackers.

Between April and June, investors reinstated their preference for global passives over actively managed domestic strategies, further cementing a trend that seems more and more impossible to counter.

Below, we reveal the IA funds that have seen the largest market movements in the second quarter of 2024.

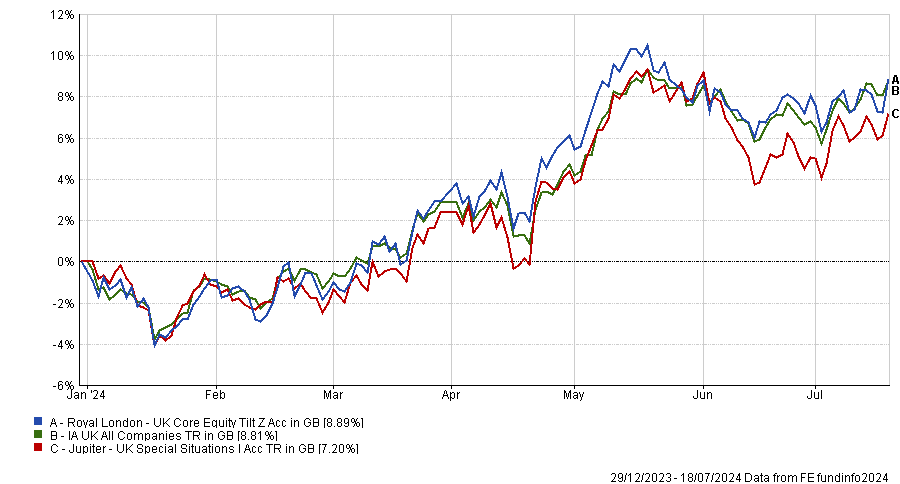

All the main losers across the key Investment Association sectors – those that have seen redemptions greater than £500m – had a focus on the domestic market.

Two were in the IA UK All Companies sector – Royal London UK Core Equity Tilt and Jupiter UK Special Situations – and one, Aviva Inv Corporate Bond, in the Sterling Corporate Bond sector. However for at least two of these, idiosyncratic reasons rather than broader market considerations might have moved the needle.

On the opposite side of the spectrum, three other funds gained inflows greater than £500m, all of which were passively managed. Two invest globally and one in Europe, as the table below shows.

Source: Trustnet

The biggest outflow was that of Royal London UK Core Equity Tilt, from which investors withdrew £1.4bn.

Before August 2021, the strategy was called Royal London FTSE 350 Tracker, but then it changed its mandate to include a carbon control strategy into the process and now aims to maintain a carbon intensity that is at least 10% lower than its benchmark, the FTSE 350 index, whilst also considering a company’s ability and willingness to transition and contribute to a lower carbon economy.

Since then, the fund’s size has shrunk by 17%, with the steepest drawdowns happening between February and June 2023 and in May this year. A spokesperson for the fund said this was an internal move, with the money leaving the fund being retained in the firm’s other ranges.

Square Mile analysts rate the fund, basing their conviction upon “the suitability of the index tracked, the management group's commitment to operating passive strategies, the size of the fund, the fund's cost and its good historic record of tracking the index”.

“Alongside this, we are confident in the team’s ability to improve the responsible investment and ESG credentials of the fund, particularly given the strong responsible investment team at Royal London,” they said.

Turmoil around the managing team of Jupiter UK Special Situations has lost the fund £503m, as manager Ben Whitmore is set to leave the firm and to be replaced by FE fundinfo Alpha Manager Alex Savvides by the autumn.

Square Mile has suspended its rating of the fund as the passing of the baton takes place and so has RSMR. While experts were torn as to whether to stick with the fund or not, investors were more resolute to pull money out – since the beginning of the year, assets under management (AUM) dropped more than 35% from £2.2bn to the current £1.4bn.

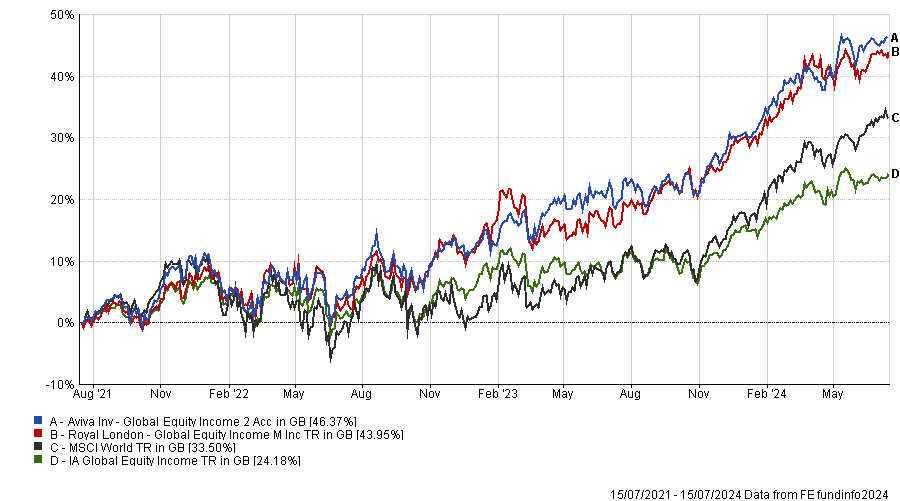

Performance of funds against sector over the past year

Source: FE Analytics

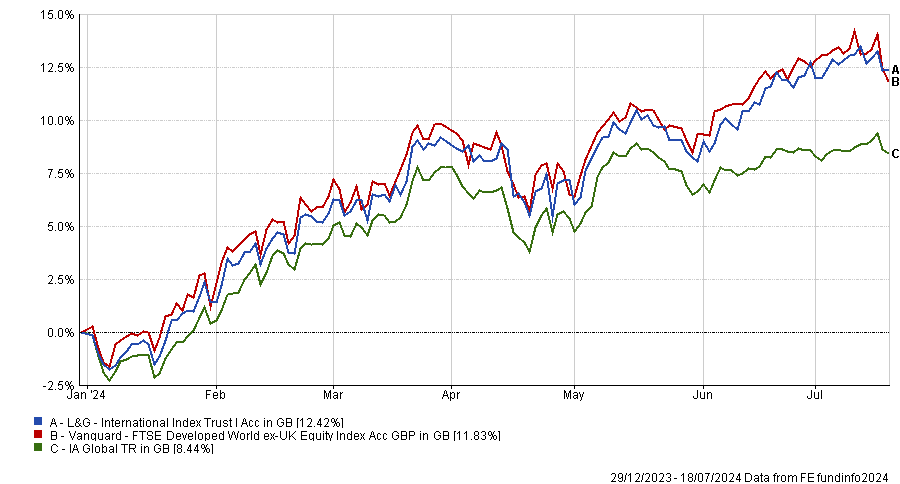

Turning to funds that attracted more than £500m, unsurprisingly two of the three that made the list were in the IA Global sector – and all were index trackers.

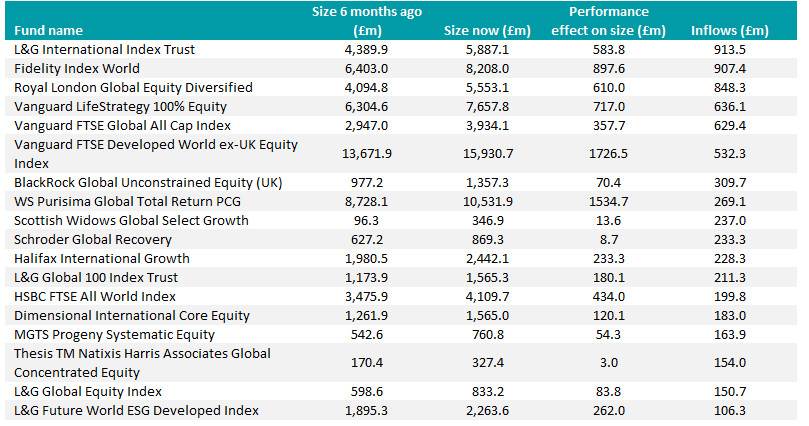

The £15.9bn giant Vanguard FTSE Developed Europe ex-UK Equity Index gained £581.3m from keen investors while also building up £384.2m from performance – the best result of all funds listed here.

The vehicle has the maximum FE fundinfo Passive Crown rating of five and is highlighted by FE Investments analysts for its fully physical process with lending – meaning that it replicates the performance of its benchmark, the FTSE AW Developed ex UK Net index, by direct ownership of all the underlying securities and compensating for the trading costs through stock lending.

Another fund that convinced investors was the L&G International Index Trust, another product physically replicating an index, the FTSE World (ex UK), but that does not engage in stock lending.

RSMR analysts said: “The lack of securities lending in retail facing products is a standout feature of LGIM passive products. The team believes that it should minimise retail customers’ exposure to additional risks and keep their index funds as transparent and easy to understand as possible,” they said.

“This fund can be used as a core holding across a range of client risk profiles.”

Performance of funds against sector over the past year

Source: FE Analytics

Finally, the fund that gained the most in investor’s faith was iShares Continental European Equity Index (UK).

It tracks the European market as defined by the FTSE World Europe ex UK index, and with Europe being tipped as the market that could overtake the US, investors piled in with north of £850m.

Square Mile analysts praised it for the suitability of the index tracked, the management group's commitment to operating passive strategies, the size of the fund, the fund's cost and its good historic record of tracking the index.

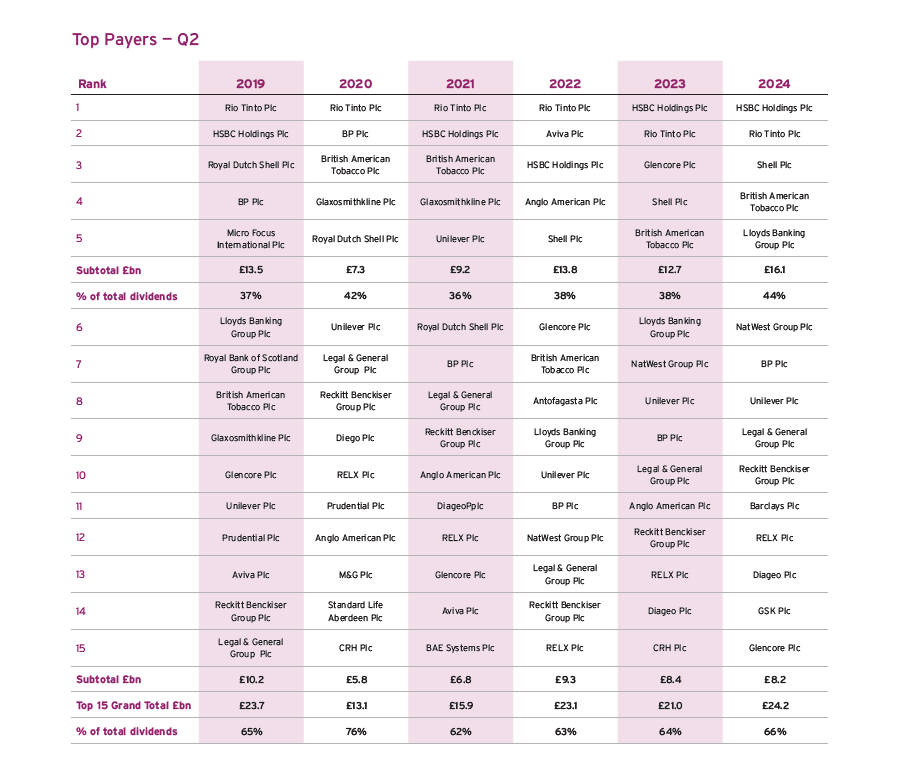

The bank paid the fourth largest one-off dividend in 17 years but forecasts for the rest of the year have been revised down.

HSBC paid out some £9.3bn in dividends this quarter, representing 25% of all payouts between April and June, according to Computershare’s recent Dividend Monitor Report, but the underlying picture for UK dividends is weaker than expected.

One-off special dividends totalled more than £4.1bn in the second quarter of 2024, more than the previous six quarters combined, headlined by HSBC’s £3.1bn, the fourth highest one-off dividend in 17 years. This majority of this payment came from sales proceeds of HSBC’s Canadian branch.

Other big specials between April and June included software company Ascential, which paid out £450m, and Pinewood Technologies (£358m).

Source: Computershare

As seen above, this payment made HSBC the leading dividend payer this quarter, beating out companies such as Rio Tinto, Shell and NatWest.

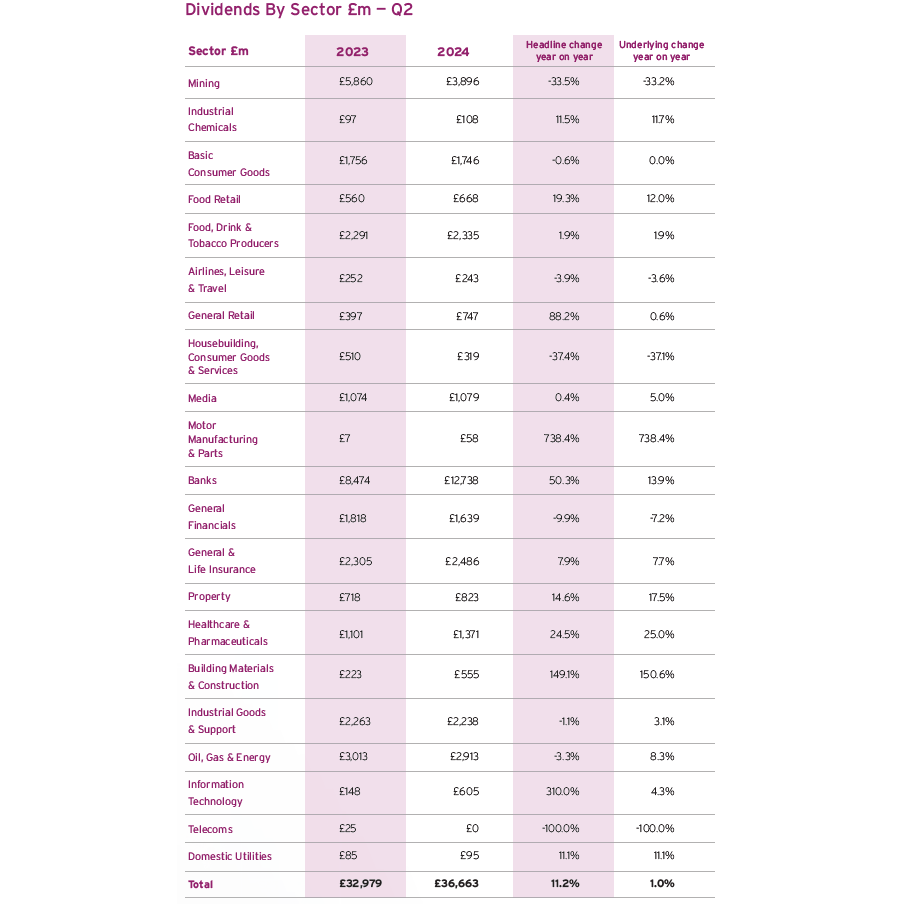

More widely, Computershare’s research indicates that most sectors also had great success in this period, with 16 out of 21 industries increasing their dividend payouts over the three months.

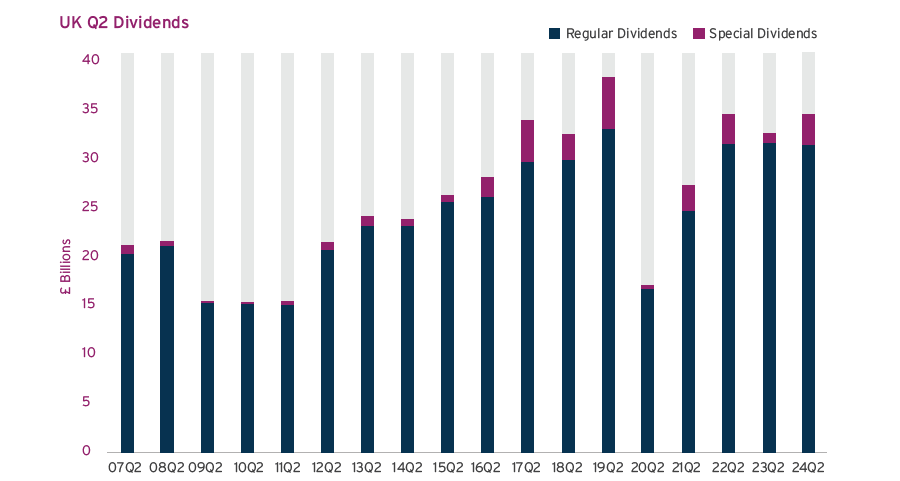

This surge in special dividends, has contributed to an 11% rise in dividend payouts from last year, with the market paying out a total of £36.7bn, the third highest second quarter in the report’s history.

Source: Computershare

The banking sector as a whole was one of the strongest contributors to dividend growth last quarter. Banks distributed a total of £12.7bn in the three months, 50% more than last year, with banks such as Lloyds and NatWest among of the top 10 payees in the period.

The insurance sector also contributed to a positive picture in the quarter. Businesses such as Direct Line restored payouts after the 2023 cancellation, and Aviva and L&G also made “healthy increases” the report noted.

Other sectors such as healthcare also improved notably in this period, with payouts rising by 25%, due to significant increases and for companies such as Haleon.

Mark Cleland, chief executive of issuer services for the United Kingdom, Channel Islands, Ireland and Africa (UCIA) at Computershare noted the UK economy has started to pick up, resulting in higher profits. Consequently, sectors are paying more in dividends and spending more cash on share buybacks, resulting in greater optimism towards the market.

Despite these positive results, Computershare’s underlying growth forecast for the rest of the year has settled at just 0.1%, well below the initial estimate of 1.5%.

Cleland attributed this to large cuts in other sectors, which masked the wider market strength. These cuts were so significant that the combined contribution of some of the biggest sectors such as banks, oil and healthcare was necessary just to offset the drag.

As an example, the decision by Vistry to scrap dividends in favour of share buybacks had an impact, as did cuts from companies such as Barratt Developments, which suffered from a tough housing market. In total, housebuilding dividends fell by 37% year-on-year.

Easily the most influential sector shaping this lower forecast for underlying growth, however, was the mining sector, which faced a difficult quarter characterised by a second year of consecutive spending cuts.

Despite making up £1 of every £11 of UK dividends since 2015, the mining sector was responsible for a third of the market’s volatility, with dividend payouts dropping by £2bn to just £3.8bn in total last quarter.

This decline was attributed primarily to companies such as Glencore, whose total payout was £1.5bn lower than the second quarter of last year.

“The mining sector has helped drive faster growth for UK dividends over the longer term, but the highly cyclical nature of the industry means it has introduced much more volatility into each year's overall UK dividend picture” Cleland said. “The gravitational pull of mining companies on UK dividends is hard to escape”.

Moving into the rest of the year, Cleland noted that the volatility of the mining sector will act as the major obstacle to further progress.

Dividend payouts in the mining sector are expected to decline by $3bn in total by 2025. Mining is still the second largest sector in terms of dividends, meaning this will have a big impact on the wider dividend picture.

This largely offsets the underlying growth of the wider market, but Cleland noted that this is not currently cause for concern. Overemphasising the mining sector obscures the significant progress made by many other sectors.

Source: Computershare

Indeed, if the 'mining effect' were removed from the dividend report, underlying dividend growth for the period would have reached 8.6%, a much more impressive figure.

Cleland concluded: “The second quarter figures show that most sectors are delivering growth, and we expect that to continue in the second half of the year”, with banking, insurance and oil expected to be the drivers of further growth.

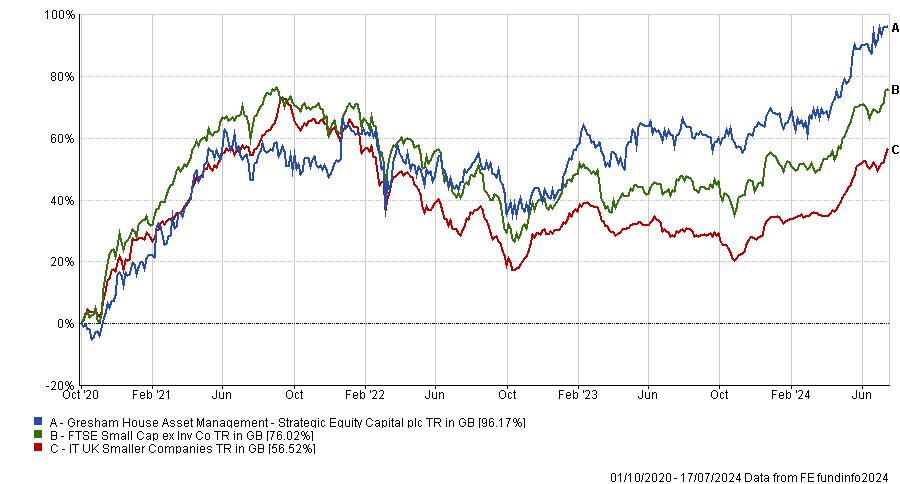

Mergers and acquisitions are “part of life” for smaller companies, but the Strategic Equity Capital manager expects the current M&A frenzy to calm down.

Private equity firms have capitalised on low valuations in the UK stock market to acquire a spate of small- and mid-cap companies, prompting concerns about the ‘smid’-cap sector shrinking.

However, FE fundinfo Alpha Manager Ken Wotton disagrees, believing M&A to be a cyclical phenomenon unlikely to persist at the current pace.

Besides, mergers and acquisitions constitute one of the strategies he uses to create value for Strategic Equity Capital, the investment trust Wotton has managed since 2020.

Performance of fund since Wotton’s appointment vs sector and benchmark

Source: FE Analytics

Below, Wotton explains why at least 75% of his fund is held in just 10 companies and how he sometimes intervenes to prevent M&A transactions.

Could you explain your investment strategy?

We describe it as taking a private equity approach to investing in public markets. When we invest in a company, we expect to hold it for three to five years, and because of that time horizon, we think of ourselves as owners of the business rather than holders of shares.

We do more due diligence than the typical public market investor. We try to build high conviction investment cases on the individual holdings.

We take a very concentrated portfolio approach and typically have around 20 holdings in the fund, with 75% to 80% of the value of the fund in the top 10. The next 10 holdings are toehold stakes where we look to potentially increase our investment in the future.

Because we take larger equity stakes in the companies we back, we have a platform for active engagement with their management teams and boards, enabling us to add more alpha.

What characteristics do you look for in a business?

We want to find businesses that are growing. Ideally, they are benefiting from structural growth drivers in their market or have self-help levers allowing them to gain market share even if the overall market isn't growing.

We're also looking for businesses that are profitable, have good margins and can turn profits into cash. Typically, they don't have much financial gearing, because we're trying to find low-risk situations.

We also want to back high-quality management teams. We might complement that by introducing non-executive directors who have the right skills and capabilities to help our investee companies.

There are certain sectors we avoid. We don't invest in oil and gas, mining, banks or real estate. That’s because we want businesses that are not overly impacted by external cyclical factors.

Why should investors buy your trust?

It provides an idiosyncratic, low correlation play on UK small-caps. The businesses we hold are not well researched, not well known and the market they operate in is less efficient.

Because UK small-caps are currently out of favour, we think there's a structural discount for businesses that have the size we're targeting. If we can apply our resources and expertise to find the right companies, there's an opportunity to get a really attractive return.

We try to help our companies tell their stories more effectively and do certain things to get recognised. Even if they are not re-rated, we can make returns through earnings growth and cash generation.

The M&A market is an alternative option for value realisation. Because of the stakes we take in our businesses, we have influence over that and can typically enable an M&A transaction to happen if we think it's a good price. However, we will stop the transaction from happening if the price is bad.

We don't want all our companies to be taken over, but it is an option for value creation.

Several UK small-cap companies are being taken over by private equity firms; does that worry you?

Not really, M&A is a part of life when investing in smaller companies and it's always been a feature of the fund. More than a quarter of the names we've ever owned have ended up being taken out.

We're at a point in the cycle where the disconnect between equity valuations and private markets is such that there's an arbitrage opportunity, which is attractive to private equity and corporates, but that won’t stay around forever.

We were in the opposite situation three years ago. In fact, 2021 was the biggest year for initial public offerings (IPOs) in the UK in a decade. Private equity and venture capital funds IPO-ed their businesses rather than buying businesses from the market. That’s why I think it's a cyclical phenomenon.

What have been your best and worst performing stocks over the past 12 months?

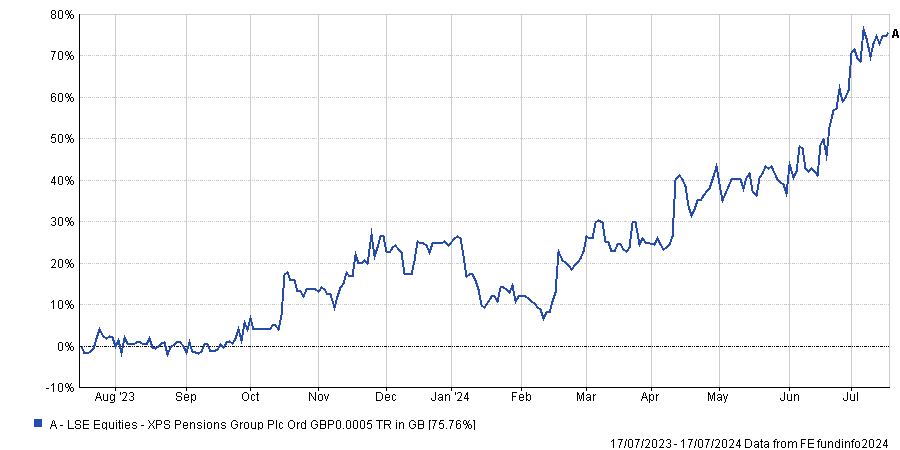

Our best performer has been XPS Pensions Group, which is an actuarial consultancy business and pensions administrator. It's our largest holding and has all the financial characteristics that we like.

It operates in a non-cyclical market because regardless of whether the economy is growing, trustees of pension funds require actuarial valuations and advice on how to comply with regulation.

Over the past 12 months, the share price has performed very strongly because XPS Group has had a series of upgraded forecasts and accelerating earnings growth.

Performance of stock over 1yr

Source: FE Analytics

The worst performer has been R&Q Insurance Holdings, which is a specialist insurance business.

Its historic business model was balance sheet-based. The company made money by acquiring books and legacy liabilities from other insurers or corporates and then running off those books more profitably.

R&Q Insurance Holdings has been switching to a fee-for-service model, akin to the fund management industry. It means getting third-party capital to acquire these books of business through fund vehicles and then getting a fee for managing them. That's a better quality of earnings and less capital intensive business model.

Unfortunately, some issues in the legacy part of the business came to the fore and caused a profit warning, which has inflicted stress on the balance sheet.

Performance of stock over 1yr

Source: London Stock Exchange

What do you do outside of fund management

I am into electronic music, so I like DJing.

Trustnet reveals which regional equity funds investors are backing and ditching this year.

Investors have been making extensive use of cheap passive funds to increase their exposure to regional equity markets during the first half of this year, according to fund flow data from FE Analytics.

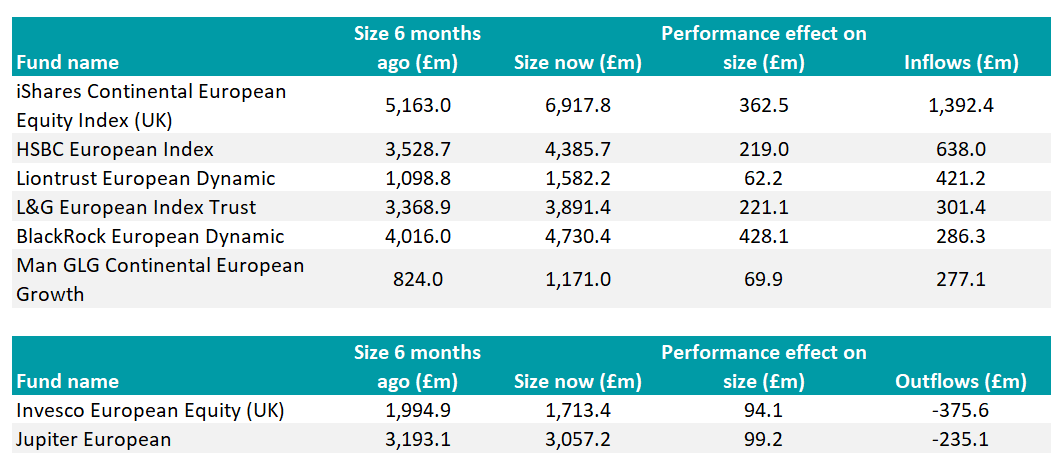

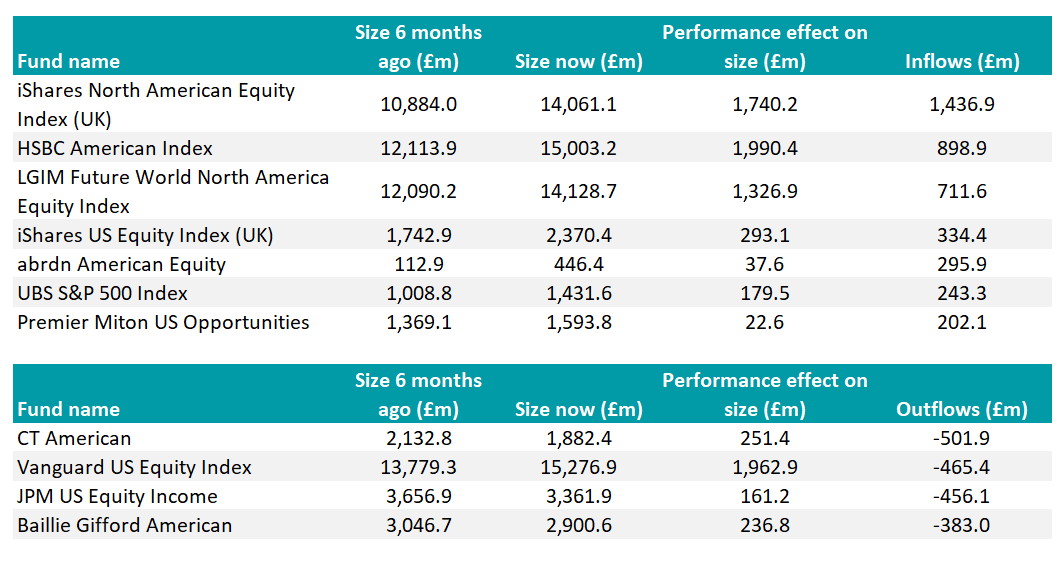

BlackRock’s iShares range of passive regional strategies proved the most popular with investors, who funnelled £1.4bn apiece into iShares Continental European Equity Index (UK) and iShares North American Equity Index (UK) during the first six months of this year.

They also ploughed £925m into iShares Japan Equity Index (UK), £353m into iShares Pacific ex Japan Equity Index (UK), and almost £200m apiece into iShares Emerging Markets Equity Index (UK) and iShares Emerging Markets Equity ESG Index (UK).

European equities

Investors increasing their exposure to Europe ex-UK chose passive funds managed by HSBC Asset Management, Legal & General Investment Management and Vanguard.

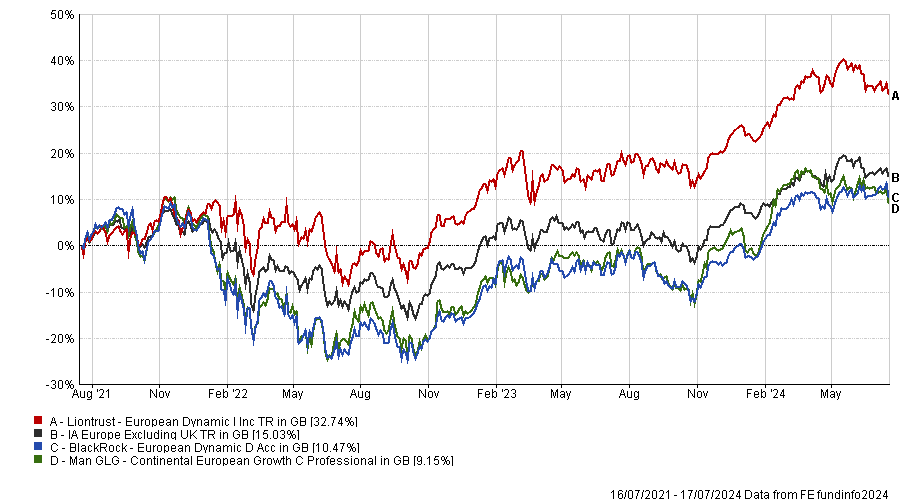

The most popular active funds were Liontrust European Dynamic, BlackRock European Dynamic and Man GLG Continental European Growth, which took in £421m, £286m and £277m, respectively.

Of these, only Liontrust European Dynamic beat the average fund in the IA Europe Excluding UK sector over three years, losing less than the others in the 2022 bear market. All three funds beat their peer group over five and 10 years.

Performance of funds vs sector over 3yrs

Source: FE Analytics

Managed by James Inglis-Jones and Samantha Gleave, the £1.5bn Liontrust European Dynamic fund is a top-quartile performer over three and five years but slipped to the second quartile in the past 12 months.

Its largest holdings are Novo Nordisk, which has a dominant position in the diabetes and weight loss drug market, and ASML, whose lithography technology is used to mass produce semiconductor chips.

Meanwhile, investors took £376m out of Invesco European Equity (UK) and £235m from Jupiter European.

Invesco European Equity achieved top-quartile performance over three years but slipped to the fourth quartile in the past 12 months and its five-year track record has lagged the sector average.

Jupiter European is fourth quartile over one and three years but FE Alpha Manager Mark Heslop, who has been running the fund with Mark Nichols since 2019, has a stronger long-term track record.

Funds attracting or shedding more than £200m in 1H 2024

Source: FE Analytics

Source: FE Analytics

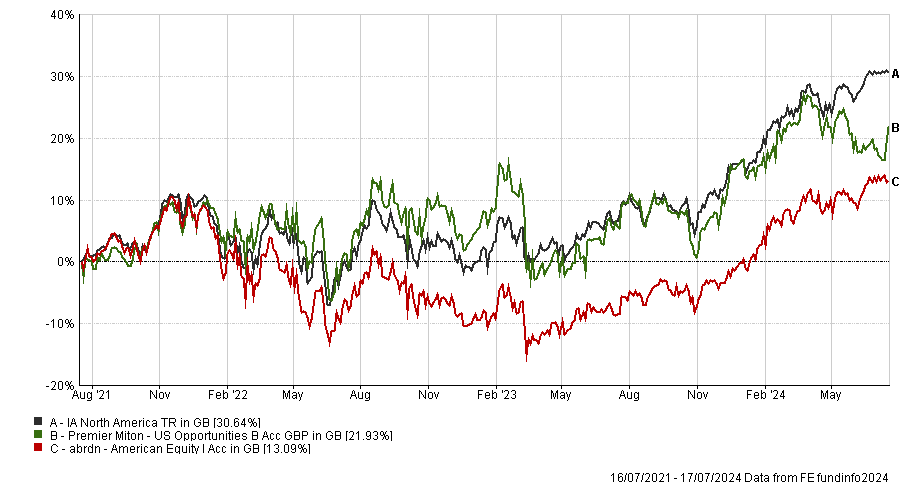

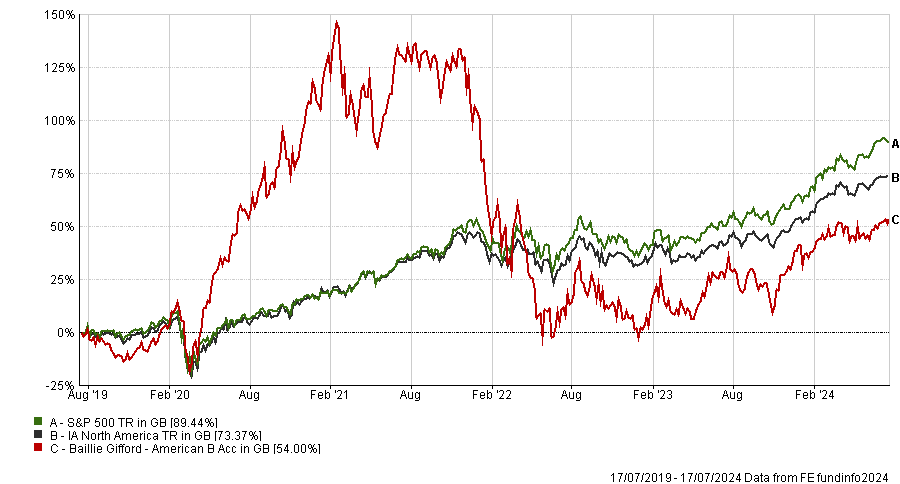

North America

Given how well the major US benchmarks and their largest sector, technology, have performed this year – and how efficient the US large-cap market is generally believed to be – it is no surprise that investors gravitated towards cost-effective passive strategies.

HSBC American Index gained £899m in inflows and LGIM Future World North America Equity Index took in £712m, on top of the £1.4bn flooding into iShares North American Equity Index (UK). However, investors took £465m out of Vanguard US Equity Index.

Funds attracting or shedding more than £200m in 1H 2024

Source: FE Analytics

Just two actively managed funds received more than £200m in inflows: abrdn American Equity and Premier Miton US Opportunities. Both funds lagged their peer group average over three years, as the chart below shows.

Performance of funds vs sector over 3yrs

Source: FE Analytics

Three active funds suffered significant outflows: CT American (shedding £502m), JPM US Equity Income (£456m) and Baillie Gifford American (£383m). The latter spiked during the Covid recovery but then gave back most of its gains, as the chart below illustrates.

Performance of funds vs sector and benchmark over 5yrs

Source: FE Analytics

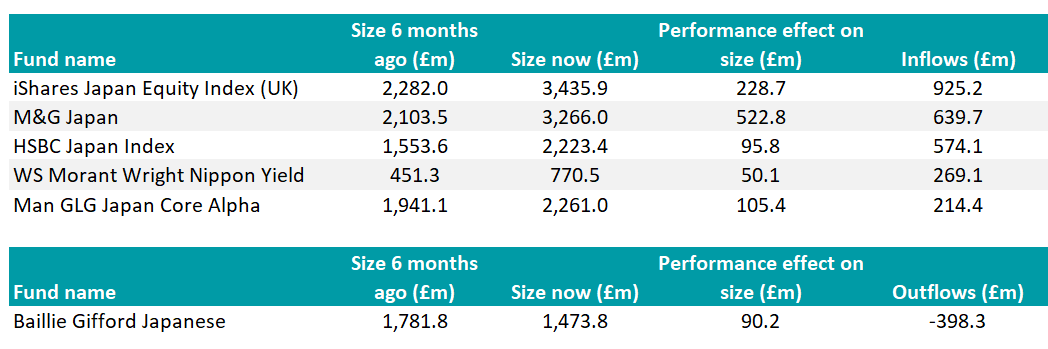

Japan

Investors bought into Japan’s equity rally, selecting M&G Japan, Man GLG Japan Core Alpha and Morant Wright Nippon Yield – complemented by passive strategies from iShares and HSBC.

Performance of funds vs sector over 3yrs

Source: FE Analytics

The Tokyo Stock Exchange’s reforms are targeting companies trading at a price-to-book value below one, and to find them, investors need to look at mid-caps, said Rob Starkey, a multi-asset portfolio manager at Schroder Investment Solutions. That is Morant Wright’s “hunting ground”, he added.

Value managers such as Man Group are also well placed to find cheap companies that will benefit from corporate governance reforms, he argued. Schroders uses Morant Wright Nippon Yield and Man GLG Japan Core Alpha in its multi-asset and model portfolio solutions.

Baillie Gifford Japanese was the only fund in this region to see significant outflows, with investors pulling £398m in reaction to poor performance.

Funds attracting or shedding more than £200m in 1H 2024

Source: FE Analytics

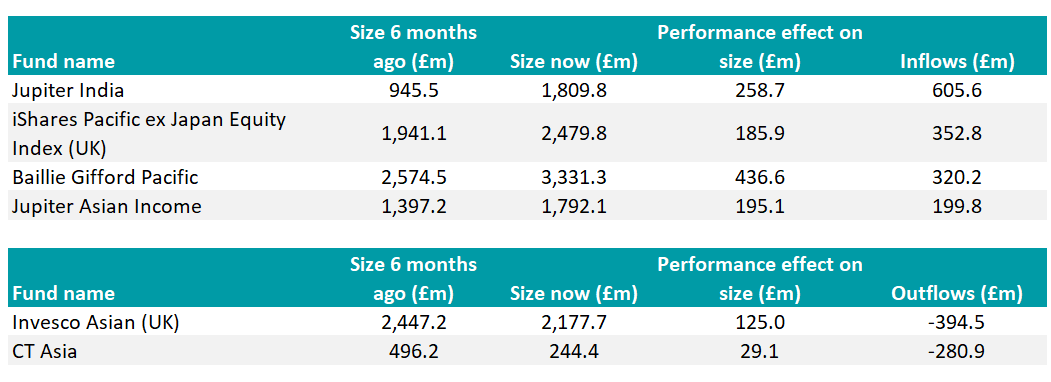

Asia Pacific

For their Asian equity allocations, investors put £320m into Baillie Gifford Pacific for growth and gave £200m to Jupiter Asian Income for stellar performance plus dividend yields, whilst also allocating to passive strategies from iShares and abrdn.

Jason Pidcock’s £1.9bn Jupiter Asian Income fund is a top-quartile performer over one, three and five years, beating its peers by avoiding China completely and favouring Australia, Taiwan and India.

Jupiter India was also popular with investors seeking exposure to one of the world’s best performing markets. It took in £606m during the first half of this year.

Funds attracting or shedding more than £200m in 1H 2024

Source: FE Analytics

At the other end of the spectrum, investors took £395m out of Invesco Asian (UK) and £281m from CT Asia.

Performance of funds vs sector over 3yrs

Source: FE Analytics

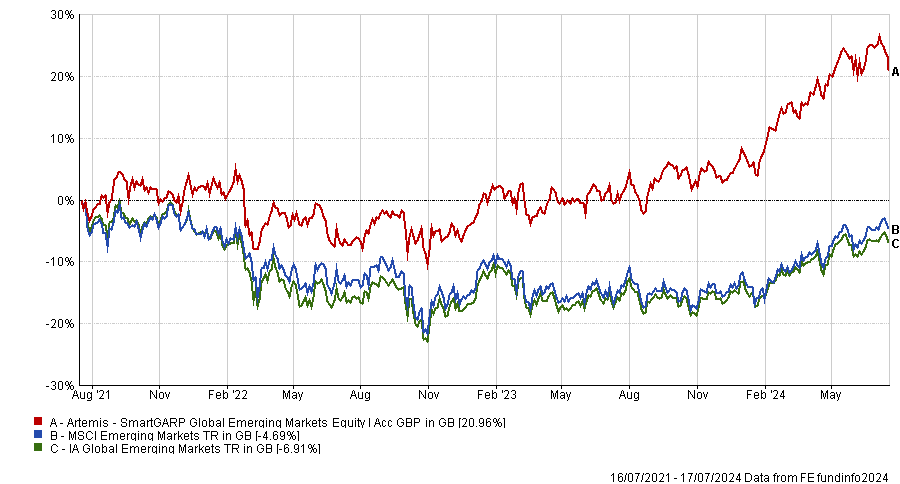

Emerging markets

Investors chose a combination of active and passive funds for emerging markets. Royal London Emerging Markets ESG Leaders Equity Tracker was the most popular strategy, bringing in £332m.

Artemis SmartGARP Global Emerging Markets Equity was the top choice amongst actively managed funds, gaining £229m. No funds had outflows over £200m.

Performance of fund vs sector and benchmark over 3yrs

Source: FE Analytics

Artemis has combined its portfolio managers’ stock-picking abilities with quantitative tools to generate “phenomenal performance”, Starkey said.

Investors were undeterred by the resignation of former fund manager and leader of the SmartGARP strategy Peter Saacke, who left the firm at the end of June to become a maths teacher.

Funds attracting or shedding more than £200m in 1H 2024

Source: FE Analytics

Trustnet reveals which investment companies in alternative sectors are top-quartile performers, with yields above government bonds.

Perhaps more than any other area of the market, those assets listed as alternatives have a crucial role in portfolios. In most cases they need to provide returns but also diversification away from the more vanilla equities and bonds. For some, such as those in retirement, income will also be a key priority.

A range of investment trusts with exposure to debt, property, infrastructure and renewable energy are ticking all the boxes – delivering top-quartile total returns over three years, a steady income stream and diversification away from investors’ equity and bond allocations. Below Trustnet reveals the best.

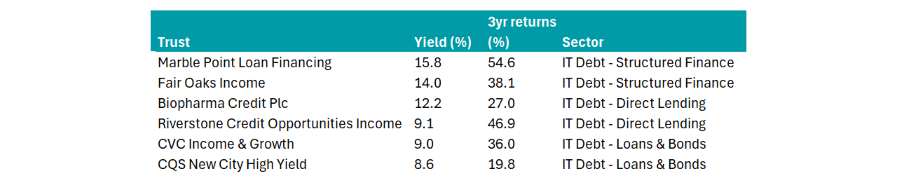

Debt strategies

Six trusts across the three IT Debt sectors (Direct Lending, Structured Finance and Loans & Bonds) meet the criteria.

Marble Point Loan Financing was the best performer from a total return perspective, returning 54.6% over three years to 17 July 2024 and paying a 15.8% annual dividend yield (as of April 2024).

Total returns and yields of debt trusts

Source: FE Analytics, trusts’ factsheets

While falling interest rates should provide a boon for most debt strategies, QuotedData analyst Matthew Read singled out CQS New City High Yield as “the best-positioned of its peers to benefit” because it has locked in decent yields in advance of rate cuts.

The trust is “consistently one of the highest-dividend-yielding funds in its peer group and, over the longer term, is also one of its best-performing,” Read continued.

“It has benefitted from an uplift in capital values as the headwind of higher interest rates that weighed on bond valuations in 2022 and 2023 has turned tailwind.”

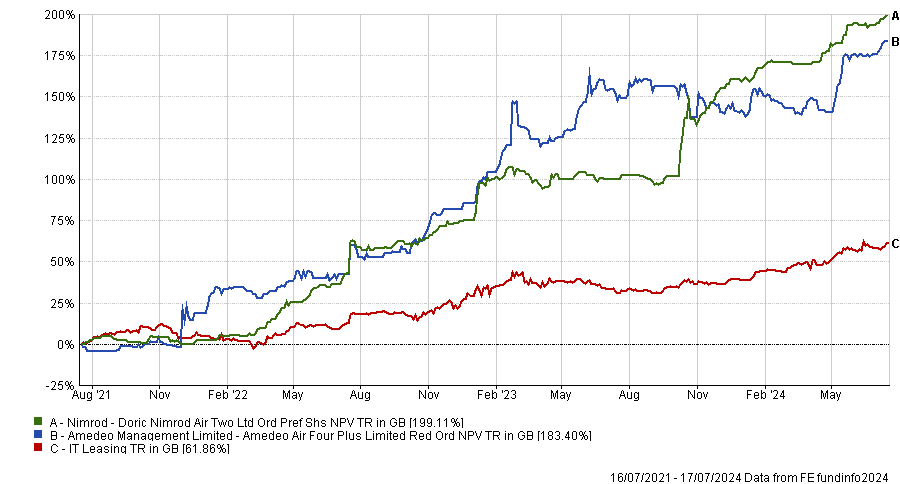

Leasing

Two trusts in the leasing sector delivered impressive three-year total returns and high yields.

Amedeo Air Four Plus and Doric Nimrod Air Two are paying out 19.4% and 15.3% respectively, with three-year total returns of 99.4% and 119.5%. Amadeo has a market capitalisation of £125.4m and Doric is slightly larger with £145.6m.

Total returns of trusts vs sector over 3yrs

Source: FE Analytics

Both trusts acquire, lease and sell aircraft and they benefited from a strong recovery in air passenger traffic last year.

Amadeo’s chairman Robin Hallam said: “Demand for travel remains strong and constraining factors are related to capacity. Manufacturers cannot make up the shortfall in supply of aircraft, engines and parts which occurred between 2019 and 2022, which means lease rates and values for in demand aircraft are rising, especially if they are off lease and immediately available.”

Infrastructure

Four trusts investing in renewable energy infrastructure delivered top-quartile, positive returns for the three years to 18 July 2024 and yields above 4%.

The NextEnergy Solar fund had the highest yield of the group at 10.2%, followed by Bluefield Solar Income with an 8.8% payout, Greencoat UK Wind (7.4%) and Foresight Solar (6.3%).

The top performer over three years was Greencoat UK Wind, which returned 24.5% and is expected to benefit from the Labour government repealing the ban on onshore windfarms.

Performance of trusts vs sector over 3yrs

Source: FE Analytics

As Tommy Kristoffersen, manager of EdenTree Green Infrastructure, explained: “Last week, new chancellor Rachel Reeves arguably did more for onshore wind development in England in 72 hours than previous governments had done in over a decade by removing the restrictive clauses which had made onshore wind development nigh on impossible since 2015, marking a significant advancement in renewable energy support and opening up a pipeline of investment potential.”

Peter Hewitt, who manages the CT Global Managed Portfolio Trust, expects the value of Greencoat UK Wind’s assets to rise now the sector has a “clearer road ahead” and the government is making “positive noises”. The £3.2bn trust is trading on a 13% discount.

Real estate investment trusts

Three trusts in the UK commercial property sector and two property debt strategies delivered top-quartile, positive total returns over three years and yields above 4%.

The best performer was Starwood European Real Estate Finance, up 22.3% over three years. It pays a 6% yield. Next in line was Alternative Income REIT, which returned 17.5% over three years and yields 8.7%.

Cheyne Capital Management’s Real Estate Credit Investments had the highest yield of 9.8%, although its three-year total return was just 9.2%. AEW UK REIT yields 7.96% and returned 10.2% over three years.

The fifth trust on the list, Schroder Real Estate Investment Trust, returned 8.1% over three years and yields 8.2%.

Four more REITs were top-quartile performers in their sectors but they lost money over three years as the interest rate hiking cycle took its toll, so they have been excluded from this study.

Going forward, however, a range of tailwinds including imminent interest rate cuts and the Labour government’s housebuilding initiatives and planning reforms should boost the property sector.

Hedge funds

Gabelli Merger Plus was the best performing strategy in the IT Hedge Fund sector over three years to 17 July 2024 (up 46.1% whereas the sector was flat) and it has a 5% distribution yield.

The trust invests in cash-generating franchise companies, selling at a significant discount to Gabelli’s appraisal of their private market value. The trust generates returns when the prices of its investee companies rise due to corporate events such as mergers, acquisitions, takeovers or leveraged buyouts.

Interest rate cuts, elections and markets in different stages of the economic cycle may make investing tricky in the coming months, the wealth manager warns.

The world is going through a period of uncertainty. Although the perils of Covid appear to be over, geopolitical tension, wars, elections and sluggish macroeconomics are all things investors may be concerned about for the remainder of 2024.

Hetal Mehta, head of economic research at St. James's Place (SJP), believes there are some important areas that will shape markets over the remaining six months.

The first is economies worldwide, which are in various stages of either recovery of repricing. “Recession risks have subsided, but the conditions necessary for strong economic acceleration are not yet present,” she said.

The overall picture is an improving one, with global economic uncertainty broadly returning to pre-Covid levels.

Heading around the world, in the US a ‘soft landing’ scenario of inflation gradually reducing and growth picking up remains on the cards, but issues persist. “Inflation is on a gradual decline, but services inflation is still elevated and higher commodity prices are filtering through to the economy,” he added.

However, the upcoming US election adds a layer of uncertainty that could affect market volatility, said Mehta. She believes the result is “too close to call”.

In the UK meanwhile, the new Labour government is likely to leave high-level policies unchanged and will have little ability to “borrow or grow its way out of trouble” as inflation and wages are still “too high for comfort”.

For emerging markets, China still looms large, she noted, with “scepticism about Chinese stimulus”. However, inflation is less of a concern here.

Justin Onuekwusi, chief investment officer at SJP, said interest rates will play a big role for the rest of the year.

“Central banks face high-stakes decisions. After years of hiking interest rates, attention is turning to how quickly and easily central banks can reverse course,” he said.

In June, Canada became the first country in the G7 to cut rates, with the European Central Bank opting to follow suit soon after.

It is a different story in the UK, where inflation has fallen to 2% but the Bank of England’s key metric – service sector inflation – remains at 5%.

This is even worse in the US, where the Federal Reserve is contending with 3% inflation. Onuekwusi said here it was “even stickier, which could cause the Fed to be “even more cautious”.

Even if rates do fall, however, investors should not expect them to go back to the ultra-low era of the recent past.

How SJP is investing

Onuekwusi noted that higher interest rates should be good for equities, but not those that are heavily indebted. “Focusing on companies that are less sensitive to higher interest rates, especially those with strong balance sheets, low debt levels and solid cash flows, can be prudent,” he said.

Robin Ellis, director of portfolio strategies at SJP, added that markets are likely to be more volatile, but still able to deliver “attractive risk-adjusted returns”.

The firm is underweight the US, although it remains the largest regional allocation across the firm’s Growth Portfolios, as well as the Polaris and InRetirement ranges.

"This boils down to recent high performance and valuations. We believe it is wise to diversify more into other global markets to balance future risks and returns. Specifically, we increased our allocations to developed markets outside the US, which we feel are well placed to provide good returns from a cheaper starting point,” he said.

On bonds, Onuekwusi said interest rates have upped yields and made bonds attractive, particularly if central banks are slow to cut. Fixed income therefore “once again provides effective diversification”, he added.

This also impacts alternatives, where “the bar for incorporating alternatives into our portfolios has been raised” as the risk-reward potential for owning these assets instead of bonds is lower.

Ellis noted the firm’s multi-asset ranges are “more constructive” on the outlook for government bonds, both in terms of yield and diversification, moving this allocation towards neutral at the expense of corporate bonds, which have “continued to benefit from strong demand and supportive credit conditions”.

“Following robust performance and a tightening of spreads across corporate bond markets, we have now reduced our positioning to neutral,” he concluded.

If you are looking for undervalued stocks, you will find them in Japan.

Although the Japanese equity market is the second largest among the world's developed markets, it still has the inefficiencies of an emerging market. For investment managers, there are many opportunities to generate alpha.

Large, but inefficient

As the world's second-largest stock market in a developed nation after the USA, the Japanese stock market offers investors a large and broadly diversified investment universe.

At the same time, however, it exhibits inefficiencies that are otherwise only found in the equity markets of emerging countries.

If a market is very inefficient, i.e. many companies are misvalued, this naturally creates investment opportunities for market experts. The chances of an investment manager outperforming a corresponding benchmark index are much higher in the Japanese equity market than in other parts of the world.

One reason for the inefficiency of the Japanese stock market is that, although Japan is home to several global market leaders in various industries and is therefore internationally positioned, it is also a very local market in many respects.

For international investors, many nuances are lost when talking to Japanese companies due to language and cultural barriers alone.

Inefficiencies are also caused by the low coverage of the Japanese equity market by analysts. There is a considerable amount of good coverage on the mega caps in Japan. But this coverage decreases significantly the smaller the stocks become, even though the Japanese equity market is dominated by companies with a medium market capitalisation. As a result, the Japanese equity market is less well covered on both the sell and buy side.

There are also historical reasons for the lack of interest from international investors.. In 1989, the Japanese stock market was the largest market in the world and made up around 45% of the MSCI World Index. Eight of the 10 largest companies in the world were Japanese banks, which is why Japan was a well-known and overvalued market for a long time.

After the bubble burst, a devaluation followed that went far beyond what would have been justified by the relative earnings growth of Japanese companies. As a result, Japanese equities are now trading at a significant valuation discount to their counterparts in other developed markets, and international investors are still heavily underweight Japanese equities despite the recent revival of interest.

A new view of Japan is needed

The existing narrative surrounding the Japanese stock market needs to change. In terms of earnings per share (EPS) growth, for example, Japan has outperformed not only Europe and Asia ex Japan, but also the US over the past 10 years.

There is another success story in the area of corporate governance. Under prime minister Shinzo Abe, structural reforms had already been initiated to improve the capital efficiency of listed Japanese companies and to strengthen the focus on shareholders.

These reforms have recently received further impetus from initiatives by the Tokyo Stock Exchange (TSE). These efforts are now bearing fruit. The data shows that Japanese companies have indeed improved their corporate governance in recent years and this is already having a positive impact on company performance.

As a result of decades of deflation, Japanese companies have also significantly reduced their debt levels, as debt would incur real costs in a deflationary environment. Around 45% of companies in the MSCI Japan Index that do not belong to the financial sector now have a net cash position. In addition, the non-financial sector's net debt to equity ratio is now lower than in the rest of the world and only half the historical highs.

However, these successes are not being recognised by global investors because they have not yet been reflected in spectacular returns, as is the rule with similar developments in the US.

In Japan, we see that profits are rising, but multiples are continuing to shrink. This is completely different from the US, where multiples are climbing along with earnings. For this reason, many investors are overlooking the fundamental improvement.

Return of inflation

And there is another factor that is having a positive effect on the Japanese economy and the country's stock market: the return of inflation. Following the end of the deflationary phase, Japanese companies and private households are now rethinking.

Companies are investing more again and are also prepared to take certain risks for strategic reasons, which is reflected in an increasing number of mergers and acquisitions, among other things.

There is a similar change in private households. The mindset of many Japanese, characterised by decades of deflation – as little debt as possible, as little consumption as possible, restraint in investments – is gradually reversing.

Consumer spending is increasing and investments in their own stock market have multiplied, supported by government subsidies.

The size of the market, its inefficiency, undervaluation, attractive companies and changing consumer attitudes – together these factors create an attractive environment for investors. If you are looking for undervalued stocks, you will find them in Japan.

June-Yon Kim is lead portfolio manager for Japanese equities at Lazard Asset Management. The views expressed above should not be taken as investment advice.

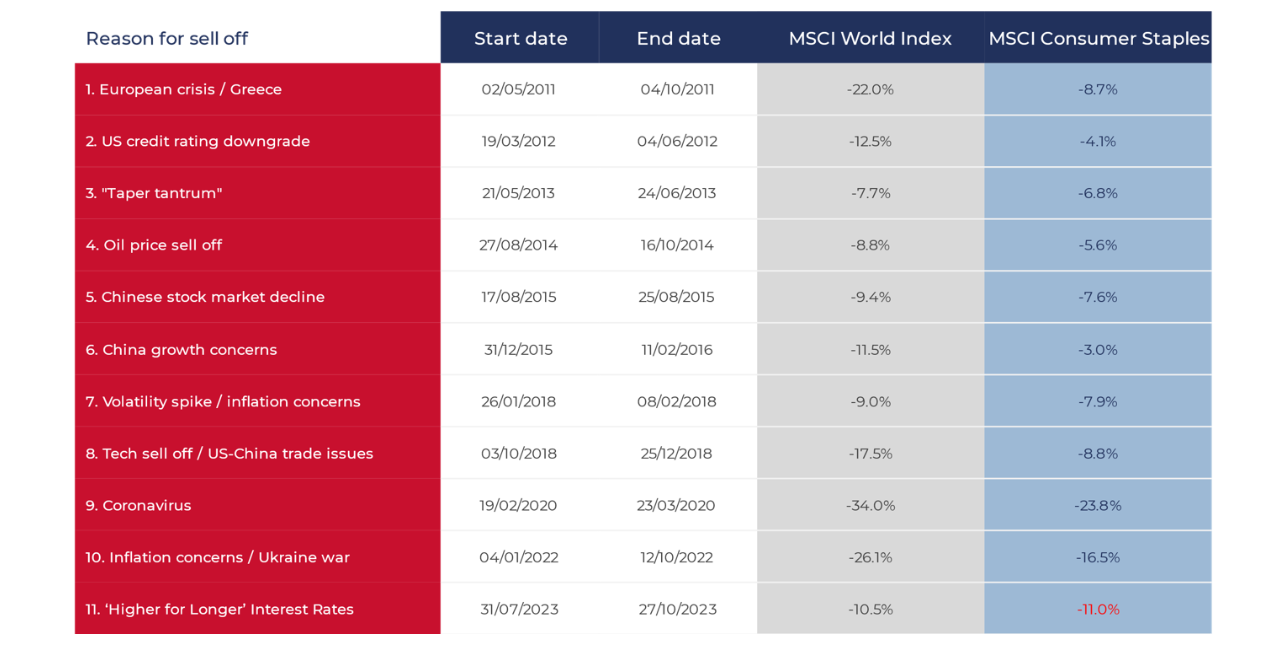

With valuations at attractive levels and margins expected to increase, this could be a buying opportunity for the consumer staples sector.

Consumer staples stocks have underperformed the broader market recently but the sector’s long-term credentials are compelling and, with valuations at historically cheap levels, this looks like an attractive entry point, according to global equity managers.

The MSCI World Consumer Staples sector has traded at an average premium of 15% to the MSCI World for the past two decades and 20% for the past 10 years. These are stable, high-quality businesses so they arguably justify a higher multiple, said Ian Mortimer, manager of Guinness Global Equity Income.

The sector outperformed during the bear market of 2022 and briefly got to a 30% premium but it has de-rated since then.

This year, it has fallen far behind the MSCI World due to technology’s dominance in the index and because investors have been rewarding growth, Mortimer explained.

Performance of consumer staples vs broader market over 20yrs

Source: FE Analytics, performance data in sterling terms

Today, the global consumer staples sector trades at less than a 5% premium to the broader market. “If you are a believer in reversion to the mean then you could see the upside potential of that premium going back to where it has been historically,” Mortimer said.

The $5.9bn Guinness Global Equity Income fund has been overweight staples since inception with a 15-20% average allocation due to these companies’ healthy dividends, high returns on capital, earnings growth and ability to outperform in falling markets. It currently holds 25% in staples versus 7% for its benchmark.

During the past couple of years, as inflation has increased, companies have passed on higher costs to their customers by raising prices. Now that input costs are coming down, companies are unlikely to reduce their prices in lockstep, so they have the potential to generate excess earnings.

“The margin picture has improved substantially year-over-year, and this expansion looks set to continue,” Mortimer explained.

Consumer staples companies usually grow their dividends in line with their earnings growth, so by 3-4% a year, but recently dividends have grown at about 5%, reflecting companies’ stronger earnings, he said.

Mortimer also likes the downside protection that consumer staples companies provide. The sector has a relative downside capture of 78% and has outperformed in all but one of the past 11 significant drawdowns.

Consumer staples outperform in most downturns

Sources: Guinness Global Investors, Bloomberg, data in US dollar terms

Below, three global equity managers pick out a consumer staple they are banking on.

Lindt

The £448m Evenlode Global Equity fund initiated a new position in Lindt this year. The premium chocolate maker had been on Evenlode’s watch list for a long time but portfolio manager Chris Elliott said it has always been “reassuringly expensive”. However, the cocoa price has shot up during the past six months, weighing on Lindt’s share price, which provided Evenlode with a buying opportunity.

Lindt is well positioned because it has hedged its cocoa supply for the rest of this year and into next year. The company possesses significant reserves of cocoa and it is more dependent on South America for its production (whereas most cocoa suppliers source from Africa.)

Share price over 12 months in Swiss francs

Source: Google Finance

Colgate-Palmolive

Within the diverse consumer staples sector, household, toiletry and health product producers have the best sustainable growth prospects, according to Gerrit Smit, manager of the Stonehage Fleming Global Best Ideas Equity fund. “These are everyday need products with less economic risk,” he said.

Smit holds Colgate-Palmolive, whose portfolio of items that everybody needs generates “very stable and certain organic growth”. Its main brands have “a high loyalty factor”, he added.

The company’s Hills Pet Nutrition business provides “further profitable organic growth” and has the potential to expand its distribution, both in the US and elsewhere, he added.

Share price over 12 months in dollars

Source: Google Finance

Mondelez International

Guinness Global Equity Income – an equally-weighted portfolio – holds a variety of consumer staples, including Diageo, Nestlé, Procter & Gamble, Danone, Unilever, Reckitt Benckiser, The Coca-Cola Company and PepsiCo.

Cadbury owner Mondelez International is one of the cheapest, Mortimer said, due to the increase in cocoa prices and concerns over its input costs.

Share price over 12 months in dollars

Source: Google Finance

Mondelez has tried to increase its margins by cutting costs, removing layers of management and improving operating efficiency, with early indications that these efforts are bearing fruit, he said.

Trustnet looks at the multi-asset funds attracting and shedding the most money in the first half of the year.

Only six multi-asset funds across the IA Mixed Investment 40-85% Shares, IA Mixed Investment 20-60% Shares and IA Mixed Investment 0-35% Shares and IA Flexible Investment sectors received more than £200m of inflows in the first half of the year.

Vanguard LifeStrategy 80% Equity was by far the most sought-after multi-asset fund during that period, with investors pouring £845.3m into this popular low-cost passive investment solution.

In addition to inflows, the fund's performance in the first six months of the year enabled it to grow its assets under management by £866.3m

Vanguard LifeStrategy 80% Equity now boasts a size of £12bn, making it the second-largest fund in the IA Mixed Investment 40-85% Shares sector after its stablemate, Vanguard LifeStrategy 60% Equity.

IFSL YOU Multi-Asset Blend Balanced came in a distant second, with investors adding £324.1m to the fund.

It was the only multi-asset fund outside of the IA Mixed Investment 40-85% Shares sector to attract more than £200m of inflows.

Source: FE Analytics

Investors also contributed between £200m and £300m to HL Growth, Coutts Managed Ambitious, MGTS Progeny ProFolio Model 50-70% Shares and BNY Mellon Multi-Asset Balanced.

At the other end of the spectrum, Baillie Gifford Managed shed the most in client assets, as investors withdrew £520.6m.

The fund sits in the top quartile of the IA Mixed Investment 40-85% Shares sector over 10 years, but it is the sector’s worst performer over three years.

Like most Baillie Gifford funds, it follows a distinctive growth style that thrived in the post-global financial crisis era but suffered when inflation and interest rates began rising in the second half of 2021.

WS Ruffer Total Return also shed more than £500m in the first half of the year.

Ruffer took a bearish view on equity markets that did not materialise, which dragged on its performance.

However, the fund’s five-year returns were better, placing it in the top quartile of the IA Mixed Investment 20-60% Shares sector.

Trojan, which focuses on capital preservation, lost £451.8m in the first half of this year, as its low allocation to equities proved detrimental.

Deputy manager Charlotte Yonge explained her wariness toward equities at the beginning of the year, noting that they were not priced for the recession she was expecting.

The fund has a significant tilt toward fixed income but also holds gold, which has surged due to election uncertainties in 2024, wars and economic instability. As a result, the fund’s performance helped to compensate for the outflows.

Source: FE Analytics

Investors also withdrew £485.1m from Vanguard LifeStrategy 40% Equity, the largest fund in the IA Mixed Investment 20-60% Shares sector.

Finally, three funds from Quilter Investors shed more than £200m in the first half of the year.

Trustnet finds that close to 20% of UK funds are ahead of the IA Technology & Technology Innovation sector over three years.

More than 60 UK funds are boasting three-year returns higher than the average tech fund, data from FE Analytics shows, as the domestic market comes back into favour.

Tech stocks have been the darlings of the market for an extended period, with the so-called Magnificent Seven (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta Platforms and Tesla) surging in recent years. At the same time, the UK market has been unloved as investors were put off by Brexit, a lacklustre economy and political infighting among multiple Conservative governments.

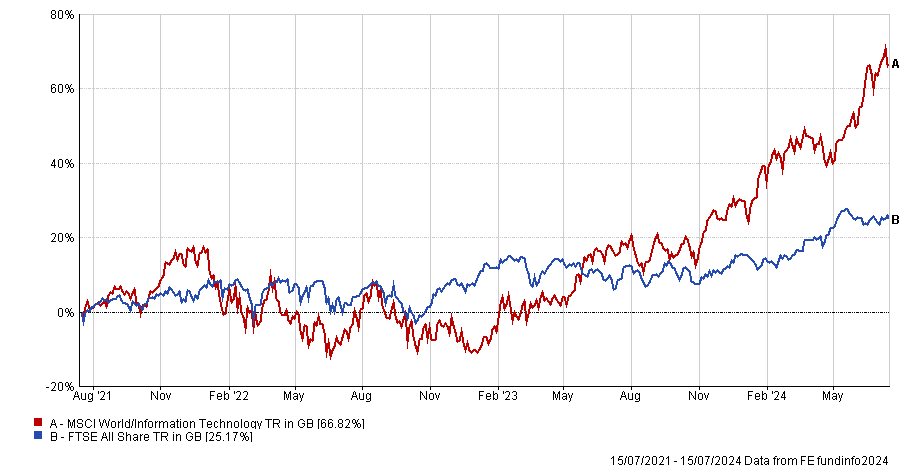

Given this, it should come as little surprise that the FTSE All Share is far behind the likes of the MSCI World Information Technology index. Over the past three years, the FTSE All Share made a total return of 25.2% while the global tech index gained close to 67%.

Performance of UK equities vs global tech over 3yrs

Source: FE Analytics

However, the Investment Association sectors focused on these stocks paint a different picture.

IA Technology & Technology Innovation is still in the lead, with its average member sitting on a 25.8% total return over the past three years. But the IA UK Equity Income sector isn’t too far behind with a 21% average return. IA UK All Companies is up 10.1% while the average IA UK Smaller Companies fund is down 13.2%.

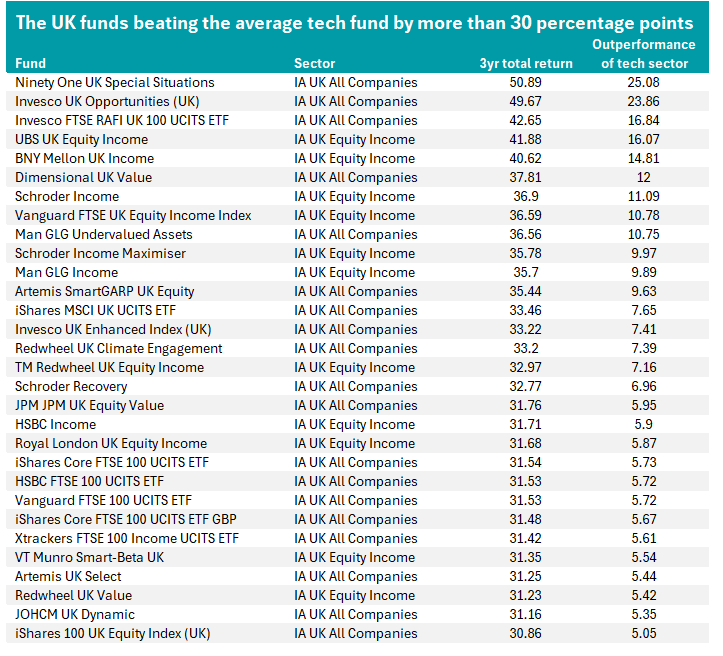

Within the UK equity sectors, quite a few funds have managed to beat the average IA Technology & Technology Innovation strategy over three years: 65 out of 346 funds (or 18.7%) with a long enough track record.

The 30 UK funds that have beaten the IA Technology & Technology Innovation sector by at least 5 percentage points can be seen in the table below. At the very top is Ninety One UK Special Situations; its 50.9% three-year return is 25 percentage points ahead of the average tech fund.

Managed by Alessandro Dicorrado and Steve Woolley, the £485m fund has a value approach that looks for ‘cheap’ companies. These tend to be stocks that are down 50% from their peak relative to the FTSE All Share over the past seven years.

Analysts at Rayner Spencer Mills Research said Ninety One UK Special Situations is a good option for investors seeking exposure to value stocks but should be paired with a growth fund rather than being the only UK holding in a portfolio.

“This is a concentrated fund with a significant bias towards value stocks,” they added. “It is likely to underperform in markets driven by growth-orientated companies, particularly when sentiment is less valuation sensitive. When there is a rally in value stocks, this fund should be a major beneficiary and outperform the market and peer group.”

Source: FE Analytics. Total return in sterling between 16 Jul 2021 and 15 Jul 2024

Although value investing was out of favour for an extended period following the global financial crisis, it has had moments of strong outperformance in recent years. The MSCI United Kingdom Value index is up 43.2% over three years, compared with a 17.8% gain from the MSCI United Kingdom Growth.

This dynamic means that many of the funds at the top of the above table follow the value style, especially as the UK market tends to have a value tilt thanks to high allocations to sectors such as banks, energy, consumer staples and industrials.

Indeed, all of the funds that have beaten the IA Technology & Technology Innovation average by more than 10 percentage points – Invesco UK Opportunities, Invesco FTSE RAFI UK 100 UCITS ETF, UBS UK Equity Income, BNY Mellon UK Income, Dimensional UK Value, Schroder Income, Vanguard FTSE UK Equity Income Index and Man GLG Undervalued Assets – as well as many of those that follow have a value bias.

A general uptick in the UK market, thanks to attractive valuations, improving macroeconomic data and the expectation of political stability, could also explain why some UK funds have been able to beat the average tech fund.

BlackRock – the world’s largest asset management house – recently went overweight UK equities, saying: “We see the Labour Party’s landslide UK election victory increasing the likelihood of a two-term government. The potential for long-term policy implementation should bring relative political stability, in our view.

“We think perceived stability can help improve sentiment – especially among foreign investors who own more than half of UK shares.”

The divergence in performance among underlying tech stocks is also a factor: not all parts of the tech market are soaring.

The bulk of the gains in recent years have been driven by the Magnificent Seven, so funds that avoided these companies have struggled. In recent months, some of these companies have even started to underperform.

Within the IA Technology & Technology Innovation sector, the best fund over three years is up around 85% (iShares S&P 500 Information Technology Sector UCITS ETF) while another four made total returns in excess of 60%. However, the worst performer is down more than 35% (WisdomTree Cloud Computing UCITS ETF) and another three have lost over 10%.

This diverging performance has had the effect of dragging the sector average down to the level that some UK funds have been able to beat, although no UK funds have been able to outperform the best tech funds.

Experts suggest where to put your cash if the Republican candidate wins the next election.

Markets are anticipating a victory for Republican presidential candidate Donald Trump in the upcoming general election, according to experts.

The recent assassination attempt, while a horrific episode, has reinvigorated the party at a time when president Joe Biden has come under pressure from fellow Democrats for his seemingly ill health.

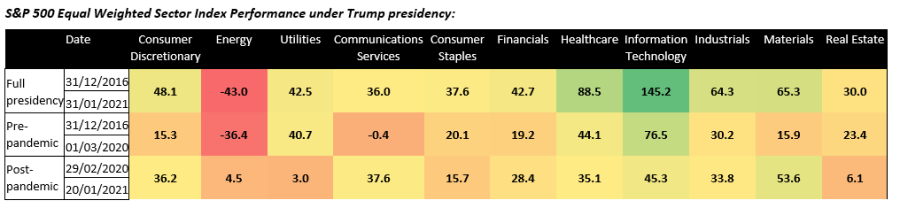

Should Trump regain the presidency, markets could be rocky, but his previous term in power was one that could give investors hope. Indeed, although his first time in office was full of uncertainty, markets performed quite well, with all bar one S&P 500 subsector making gains, as the below chart shows.

Source: Shore Capital

James Yardley, senior research director at Chelsea Financial Services, said defence stocks should thrive under Trump, who is expected to push for increased military spending.

“This focus on bolstering military capabilities, coupled with growing global security concerns, could create a strong tailwind for defence companies,” he said.

While the sector is largely admonished by environmental, social and governance (ESG) strategies, Yardley said the debate around the sector “is evolving”, and more investors “recognise the importance of security and defence in today's geopolitical climate”.

“This shift could lead to broader investment in defence stocks, potentially making them an attractive option in a Trump-led global economy,” he said.

Meanwhile, further down the market capitalisation spectrum, small-caps may do well under Trump as his ‘America First’ policies should encourage more spending on domestic goods.

Any potential increase in tariffs, particularly on goods from China, will likely benefit as a protectionist stance “could shield them from international competition and potentially boost their market share”.

Here, he likes the Artemis US Smaller Companies and T. Rowe Price US Smaller Companies Equity funds, which are “particularly well-positioned to benefit from this trend”.

“Furthermore, small-cap stocks tend to outperform in a falling interest rate environment, which will likely begin early into Trump's term,” Yardley said.

However, stocks that did well last time under Trump may continue to shine if he is re-elected, said Greg Eckel, portfolio manager of Canadian General Investments.

Leading the way during his previous tenure was technology, which gained 145%, with a particular rise during the final year when the Covid pandemic turbocharged online sales.

Eckel said the tech surge should continue

Healthcare names also thrived during his previous term, despite the former president’s efforts to overturn Obamacare and attempts to reduce the cost of pharmaceuticals.

This time around, however, investors should “be wary and expect a volatile environment irrespective of the next administration as the US healthcare industry is extremely complicated and highly prone to changes in government policy,” said Eckel.

Instead, investors may want to consider US industrials, which could benefit from “commitments to infrastructure build”, which seem to have “bipartisan support”.

Not all were convinced that US stocks would shine under Trump, however. Raphael Olszyna-Marzys, international economist at J. Safra Sarasin Sustainable Asset Management, said a possible “erosion of checks and balances” under Trump could hinder long-term economic growth, with bond yields expected to rise higher if there were to be a “Republican clean sweep”.

“The dollar might initially strengthen under Trump but could weaken over time,” he said, while equities “may gain from tax cuts initially but suffer later due to Trump’s broader policies impacting corporate profitability”.

“Overall, we believe Trump’s policies are likely to result in slower economic growth, higher inflation, increased bond yields, and a weaker dollar in the medium to long term,” said Olszyna-Marzys.

“In the short term, a looser fiscal policy stance could temporarily boost the economy, potentially lifting equity prices. Additional tariffs under Trump might initially strengthen the dollar, though this effect would likely diminish over time.”

Changing the rules might seem too clever by half, but are an effective way to mitigate some issues.

As Rachel Reeves moves into Number 11 Downing Street, she faces a fiscal conundrum. Her party’s manifesto pledged ‘no return to austerity’, yet she is inheriting plans containing significant spending cuts, and her room for manoeuvre is limited.

She’s pledged not to increase the four taxes that raise most revenue, and to retain fiscal rules that limit her scope to borrow. Squaring this circle won’t be easy. However, the situation is better than the gloomier prognoses suggest, and we’re still happy holding UK government bonds.

How did we get here?

A little history helps to explain Reeves’ bind. Since the late 1990s, the UK government has set itself fiscal rules designed to keep borrowing within sensible limits. The precise form of these rules has changed many times, as they have been overtaken by events.

But this time, the Starmer administration has pledged to retain the same key rule (the ‘fiscal mandate’) as its predecessor. This rule states that public debt must be projected (in the Office for Budget Responsibility (OBR) official forecasts) to fall relative to the size of the economy in five years.

The spectre of the market turmoil that followed former Prime Minister Liz Truss’ ill-fated ‘mini-Budget’ has quelled any appetite for big changes to this framework any time soon.

Fiscal rules are great in theory. However, in practice, they sometimes have significant unintended consequences. The debt rule has been no exception, which requires debt to be projected to fall relative to the size of the economy only in the fifth year of the forecast (and not over the period as a whole).

This meant Reeves’ predecessor Jeremy Hunt could offer tax cuts ahead of the vote, while meeting the rule by pencilling in spending restraint after the election. This respected the letter of the law, but not the spirit of it, kicking the can down the road for the next government.

Adjusted for inflation, the plans that Labour is inheriting leave spending per person on public services unchanged over the next five years. Since spending on the NHS is highly likely to rise by much more than inflation, that implies sharp inflation-adjusted cuts elsewhere.

Areas such as justice and local government, which are already under severe strain, in principle face reductions of more than 2% a year. That’s before factoring in the desire to raise defence spending to 2.5% of GDP.

The Institute for Fiscal Studies describes these plans (inherited from the previous government) as ‘fiscal fiction’ and argues they are not possible “while maintaining the current range and quality of public services”.

The new government will be unable (even with a large majority) and unwilling to push through what would be austerity 2.0. Doing so would do more harm than good, given signs that public services are still reeling from the impact of the pandemic on top of the original austerity programme.

Hospital waiting times are far longer today than in the early 2010s. Local government funding remains much lower now than in 2010 (after adjusting for inflation), contributing to problems including the growing number of car accidents caused by potholes. The justice system is under pressure too, with the backlog of Crown Court cases the longest on record.

Potential solutions

Therefore, Reeves needs to find a way to increase planned spending. In doing so, she faces several constraints. Labour has consistently emphasised its commitment to fiscal rules and included them explicitly in its manifesto. This limits her ability to borrow to fund more spending.

The party also promised in its manifesto not to raise the rates of income tax, national insurance, VAT and corporation tax — which together account for two-thirds of all government revenue.

The chancellor hopes that stronger economic growth will lend her a hand. If the economy performs better than the OBR’s projections, all the trade-offs she faces become much easier. Economic expansion lifts revenues without the need to raise tax rates.