Infrastructure has plummeted over the past few years, but experts believe a resurgence is on the cards.

Infrastructure was once seen as a must-have alternative for investors who were suffering through the era of low interest rates in the 2010s, but has fallen by the wayside more recently.

This culminated in a disastrous 2023, when the asset class dropped as central banks hiked rates to deal with rampant inflation.

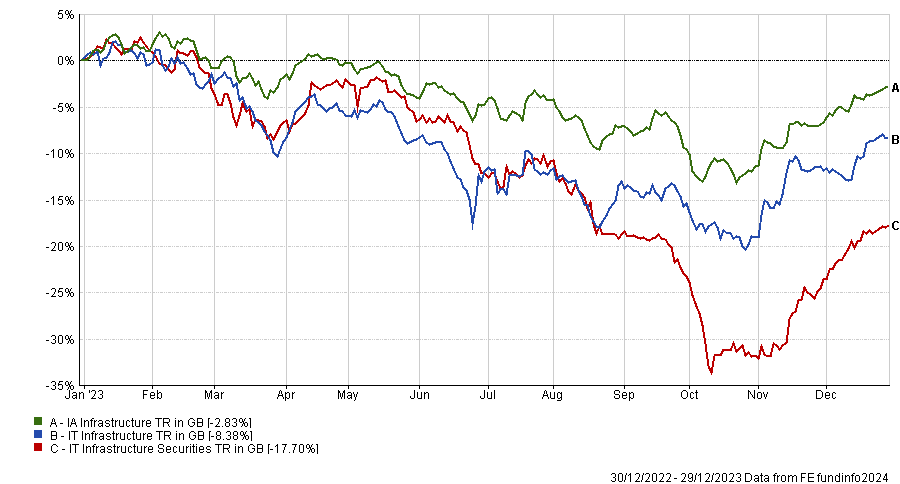

Indeed, looking at the main infrastructure sectors in both the Association of Investment Companies (AIC) and Investment Association (IA) universes, all made a loss last year, ranging from 2.8% (IA infrastructure) to 17.7% (IT Infrastructure Securities).

Performance of sectors in 2023

Source: FE Analytics

Returns have continued to underwhelm in 2024, with the IT Infrastructure the best of the trio, up 0.6%, while IA Infrastructure is down 1.1% and IT Infrastructure Securities has dropped 0.9%.

Thuy Quynh Dang, portfolio manager on the global listed infrastructure team at Cohen & Steers, said the main issue for the asset class has been the macroeconomic picture.

“While global economic growth continued to slow, it was generally stronger than expected over the course of 2023. This, combined with falling inflation, lessened the appeal of infrastructure’s defensive qualities,” she said.

Several factors were involved but perhaps the main one was the yields available to investors from other assets. Over the past decade, bonds have yielded very little with rates nailed to the floor, but now investors can make 5% or more from cash and low-risk government bonds – yields that were previously only achievable through alternatives such as infrastructure.

“In 2023, for the first time in years, interest rates rose to levels that made fixed income investments a viable alternative to higher-yielding equities,” she said.

Additionally, inflation caused companies’ costs to rise, while elevated rates and higher borrowing costs hurt sectors that tend to have more debt, such as utilities, she added.

Yet the impact of rate rises is now priced in, according to Dang. Even if rates remain higher for longer, she said markets expect a 7.8% total return from the infrastructure sector, with some areas such as renewable energy infrastructure in particular potentially making even more.

Jeremy Anagnos, portfolio manager of Nordea’s Global Listed Infrastructure strategy, was even more bullish, suggesting the asset class could “eclipse” the 8-10% returns it made over the past decade.

Infrastructure has historically performed well during periods of above-average inflation and high interest rates, he noted, highlighting the performance between 2000 and 2007, when the yield from 10-year US treasuries ranged from 3.8%-5.1% and infrastructure delivered a double-digit annualised return.

As such, “with low debt refinancing needs and healthy balance sheets, we think infrastructure can perform well if US risk-free rates remain in the 4%-5% range,” said Anagnos.

If this is reversed and rates start to fall – as is still expected at some point either this year or in early 2025 – the returns from infrastructure could be even stronger.

“Performance during the rate reversal trade over November and December, a period in which infrastructure delivered a 14% return, is a good indication of what investors could expect under such a soft-landing scenario. During this period, infrastructure kept pace with equities and nearly doubled the returns of fixed income,” said Anagnos.

Lastly, infrastructure should do well in a scenario where there is more market uncertainty (either through central banks wavering on rates or from geopolitical risks). After all, it has “saved investors about 30% of the downside in a negative market”, he noted.

Shannon Saccocia, chief investment officer of private wealth at Neuberger Berman, added that companies should do well regardless of the interest rate environment, as there remains a need for these assets.

Infrastructure is a broad term that includes bridges, roads, tunnels, power grids, hospitals, schools, data centres and ports, among numerous other areas.

“Whatever the great economic and investment themes of the next generation turn out to be, and however complex their nuances, without infrastructure they are not going to happen,” she said.

Japan isn’t as cheap as it used to be, but investors can still find value if they know where to look.

Sentiment towards Japan has improved significantly of late and there has been a big pickup in overseas flows into the Japanese equity market.

This is on the back of an “extremely strong” relative performance, according to Hawksmoor portfolio manager Ben Mackie.

“Some of that performance has come from multiple expansion”, he acknowledged, meaning that “on a simple price-to-earnings basis, Japan has become more expensive”.

Nonetheless, there is still a lot of value in Japan for investors and active managers who know where to look.

“The headline index valuation has definitely increased and you can no longer say that the overall index is as massively cheap as it used to be. It’s not expensive either, but it has definitely re-rated,” he said.

“You can think about it in terms of the proportion of the Japanese equity market trading on less than 1x book value, for example. Here, there's still a significant proportion of the market that is trading on cheap valuations.”

Performance of sector over 1yr

Source: FE Analytics

Mackie believes there are three key theme driving Japan’s equity market recovery: earnings growth, multiple re-rating and the self-help story of improving corporate governance. .Companies are increasing dividends, buying back their own shares and “really thinking about shareholder returns in a different way than they previously did”.

What has happened so far, however, is that a lot of the market leadership has been in the large caps, whereas now valuation dispersion is more interesting further down the market-cap spectrum. Investors can still find “lots of value in the smaller companies area, which is where the dispersion is particularly high”, he pointed out.

For this reason, Mackie and the other co-managers at Hawksmoor have taken some profits from large caps, where the valuation argument “isn't quite as compelling as it was”, to follow the returns down the market-cap spectrum in favour of smaller companies.

Hawksmoor’s exposure to Japan is “very significant”, spanning from 7% in more cautious funds to 12% at the higher end of the risk spectrum. By comparison, the MSCI World index has 5.9% in Japan.

One of Mackie’s favourite vehicles is the Nippon Active Value trust, whose activist approach works particularly well with smaller companies.

Performance of fund against sector and index over 1yr

Source: FE Analytics

“The trust is about taking meaningful stakes in smaller companies and then engaging with management to drive change, be that at the operational, strategic or the capital-allocation level,” he explained.

“What is really nice is that it's an idiosyncratic driver of returns, with a portion of businesses being sold and realising lots of shareholder value in a way that is independent of the rest of the market.”

Because the trust’s net asset value (NAV) is only £334.9m, it can't be a massive part of Hawksmoor’s portfolio from a liquidity perspective, Mackie said, although the praised the trust’s efforts to grow its assets by merging with abrdn Japan and Atlantis Japan Growth.

“They've been very active in terms of merging with other struggling Japanese trusts. They have grown the market cap and the liquidity of the vehicle, which is pretty commendable, and have done a very good job with it.,” he said.

To achieve a blend of styles, Mackie is using the FE fundinfo five Crown-rated Arcus Japan fund for more generalist, large-cap exposure.

Performance of fund against sector and index over 1yr

Source: FE Analytics

It is run by FE fundinfo Alpha Manager Mark Pearson, who actively turns the portfolio by selling shares that have re-rated and going back into cheaper areas of the market. Mackie described him as “very much a value manager”.

The vehicle’s top 10 holdings include Panasonic, Rakuten and Mitsubishi and currently, it makes up approximately 1.9% of Hawksmoor’s portfolios.

The next fund is Alpha Manager Carl Vine’s M&G Japan Smaller Companies, in which Hawksmoor has an average 1.7% position.

Performance of fund against sector and index over 1yr

Source: FE Analytics

This is a “more pragmatic and balanced strategy”, that is looking for stock-specific risks to be the main driver of returns.

FE Investments analysts commended the fund’s managers for their in-depth bottom-up process, “which enables them to identify strong opportunities in their 250 stocks universe whilst making proactive and quick investment decisions”.

The fund has a “highly dynamic portfolio, which regularly shifts sector and small-cap exposure relative to its benchmark while exhibiting a slight value tilt and while being a small and mid-cap fund,” the analysts added.

Finally, Hawksmoor also owns Polar Capital Japan Value to re-reinforce the bias to small-caps.

Performance of fund against sector and index over 1yr

Source: FE Analytics

The fund applies a value-based stock-picking approach, investing in a concentrated portfolio of 40 to 50 large, medium and small capitalisation companies.

Experts are mixed on whether this level of dominance can continue, however.

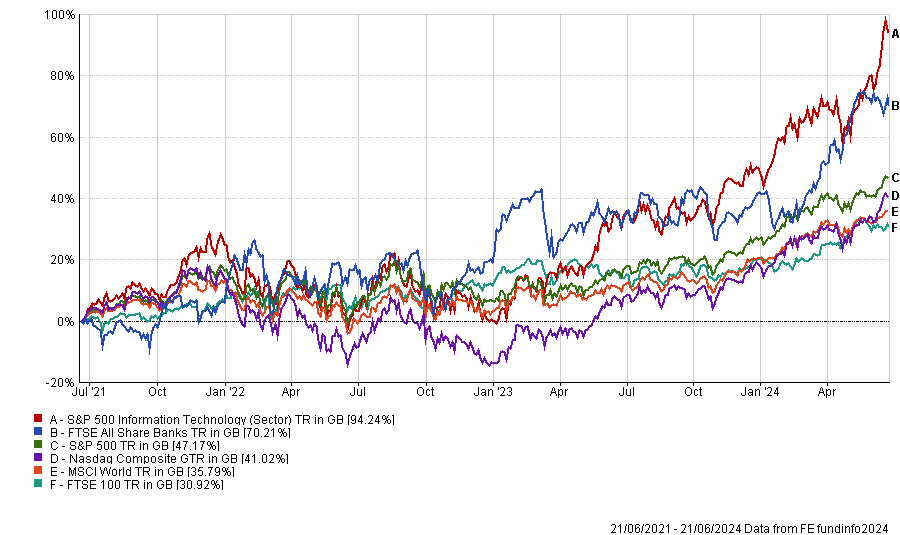

UK banks may not garner as much attention as the mighty Nasdaq or the mainstream S&P 500 index but they have proven to be a more rewarding investment than the US tech-heavy markets over the past three years.

This may come as a surprise, especially given the recent strong returns of the so-called Magnificent Seven stocks (Amazon, Alphabet, Apple, Meta, Microsoft, Nvidia and Tesla) and the powerful narrative surrounding artificial intelligence (AI).

Yet, the FTSE All Share Banks index has returned 70.2% over the past three years, while the Nasdaq Composite and the S&P 500 have ‘only’ made 41% and 41.2% respectively over the same period. The S&P 500 Information Technology, which is a pure technology index, was the exception to the rule as it slightly outperformed domestic financials.

Performance of indices over 3yrs

Source: FE Analytics

UK banks were arguably not the most obvious candidates to outperform the two popular US indices, as they have faced the double whammy of being listed on the unloved UK stock market and belonging to a sector that has faced numerous regulatory headwinds across developed markets since the global financial crisis (GFC).

Graeme Forster, portfolio manager at Orbis Investments, said: “This prolonged water torture peaked in 2020 as UK short and long yields collapsed to zero in the wake of Covid. Bank shares collapsed with them, hitting historically low valuations.”

While the post-GFC era has been torturous for UK banks, tech-dominated indices have thrived in this environment, reaching new highs amid Covid lockdowns.

Julian Bishop, co-lead portfolio manager of the Brunner Investment Trust, said: “This was due to a combination of excitement around the pace of digitalisation around Covid and low interest rates, which theoretically increase the present value of longer-duration growth stocks.

“The Nasdaq subsequently saw a correction in 2022, but has since recovered and is now enjoying new highs once again as the narrative around AI continues to build.”

However, the rapid rise in interest rates has been a turning point for UK banks, as their profitability is highly sensitive to interest rates.

Bishop added: “As interest rates have risen, banks have been able to charge customers a higher interest rate.

“They have also received far more interest income on their deposits at central banks. As depositors will have noticed, these higher interest rates have not been passed on to current accounts which still pay a meagre amount.

“The net result is a significant increase in net interest income at the banks, most of which is pure profit. Given the much improved balance sheets at most European banks, this has allowed large dividend payments and buybacks.”

Performance of indices over 15yrs

Source: FE Analytics

Although the explosive gains we’ve seen over the past three years are not likely to be repeated, Forster believes that UK banks could continue to deliver above-normal performance.

He explained valuations remain subdued and capital discipline has improved, while regulatory pressure is unlikely to get worse.

“A key determinant for the shares will be whether interest rates settle comfortably above zero, which will depend on the path for inflation. My view would be that inflation over the next decade will be structurally higher than the previous one,” Forster added.

He also liked Irish banks, which he said were an even more attractive investment option, noting that they have performed in line with, or better, than UK banks over the past few years while also having a better chance of delivering returns exceeding their capital costs in the future.

Foster explained: “This view is based on a general rationalisation within the Irish market, a direct result of an extremely punitive post-GFC regulatory environment.

“Lending into the Irish economy has become prudent and rational, leading to a healthier demand for loans from credit-worthy borrowers and a robust profitable banking system.”

Performance of indices over 3yrs

Source: FE Analytics

Not all are as hopeful for the domestic banks, however. Bishop does not believe that UK banks will continue to deliver the same level of outperformance going forward. Assuming conditions remain favourable, he expects them to continue paying dividends, but with a more modest level of growth.

Yet, he also expressed some concerns about the prospects for US tech names. He concluded: “The Nasdaq’s key constituents, on the other hand, will need to continue to post impressive growth rates and augment their barriers to entry to satisfy the elevated expectations that come with far higher multiples.”

James Penny, chief investment officer of TAM Asset Management, expects UK equities to rally if Kier Starmer triumphs at the ballot box.

A change in government next month could be the impetus investors need to return to the UK equity market, reversing the outflows of recent years and driving the UK stock market higher, according to James Penny, chief investment officer of TAM Asset Management.

“A change of the political guard breathing fresh life and vigour into Whitehall might just prove the catalyst this UK stock market needs for both international and domestic investors to get off the sidelines and start investing into one of the cheapest UK markets we have seen in recent times,” he said.

“A new government with a real bit between their teeth to get cracking and implement change could be what brings life into the stock market.”

The FTSE All Share tends to perform better during the 12 months after a general election if the keys to 10 Downing Street change hands, according to a study by AJ Bell of all 16 general elections since 1962.

The FTSE All Share rose by an average of 12.8% in the year after an election when the government changed hands, but inched up only 0.9% when an incumbent won, as the chart below shows.

Capital return from the FTSE All Share (%)

Sources: AJ Bell, LSEG Datastream

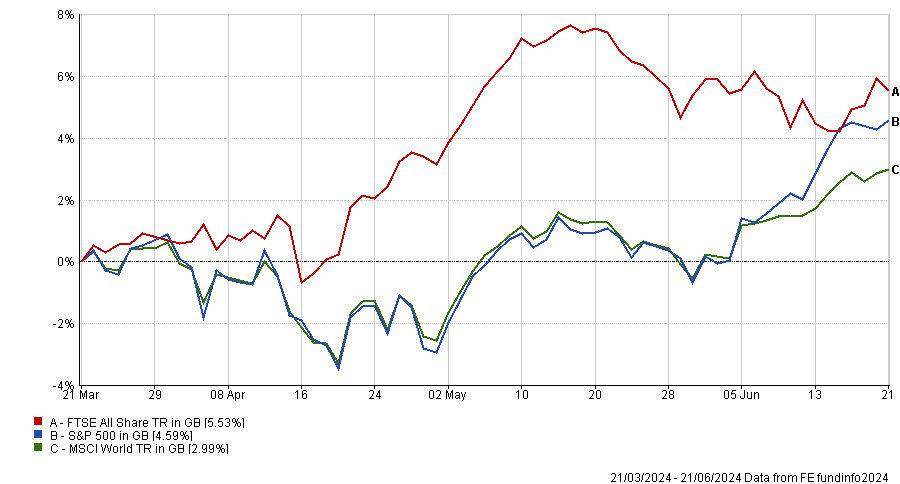

UK equities have already performed strongly this year, even beating the mighty S&P 500 in the past three months, as the chart below shows. Yet Penny thinks valuations are still cheap and the market has much more upside.

Performance of UK vs US and global equities over 3 months

Source: FE Analytics

Penny said: “We expect Labour’s potential victory to be met with a strengthening market. Bolt on the potential for rate cuts from the Bank of England, which would add further fuel to the rally, and even a rally back to our view of fair value would present a real opportunity for outperformance and alpha against increasingly US-heavy benchmarks.”

TAM has a 5-6% allocation to UK equities, slightly above global benchmarks. “We like the quality of the companies in the UK. We like the prices that we're paying for those companies. It's got a good income narrative and in a world of inflation, income is becoming important. Advisors need a decumulation piece to their proposition and the UK is a good market for that,” Penny explained.

He prefers to use active managers in the UK who can find high quality companies with strong management teams at attractive valuations. Some of the best managers in the industry are running UK equity funds, he added.

Redwheel UK Income is a core holding. Penny described the fund’s managers, Ian Lance and Nick Purves, as “an experienced team delivering a sound strategy, focusing on income and capital growth”.

It was the fifth-best performing fund in the IA UK Equity Income sector over five years and the second-best over one year to 21 June 2024. (Incidentally Redwheel UK Value, which is managed by the same people, performed even better.)

Performance of fund vs sector and benchmark over 5yrs

Source: FE Analytics

TAM also holds CRUX UK Special Situations, which invests in undervalued companies whose growth prospects are underappreciated by the market or which are in distressed situations where the market has lost confidence and overreacted on the downside.

The fund’s manager, Richard Penny, is “a competent and experienced active manager in a complicated market”. He previously ran a similar strategy at Legal & General Investment Management and has built a long-standing track record.

“Redwheel’s income and UK large-cap tilt dovetails nicely with the CRUX fund, which is a higher volatility vehicle designed to invest further down the cap scale. Owning them together gives us a better blended approach to the UK all-cap market,” TAM’s Penny said.

There is consensus among active UK equity managers that valuations are at record low levels and, as such, “there are opportunities everywhere for alpha to buy good companies trading on pence in the pound”, Penny continued.

“It's been painful to be a UK manager, really painful. You've got to love the UK market to want to stick with it. But a lot of these guys have been through boom and bust in the UK and are really positive about the direction for the UK going forwards,” he concluded.

In an uncertain world, diversification and price remain paramount for investors.

Many column inches and headlines have been dedicated to the decision by several high-profile UK investors to materially change their allocations to UK assets in favour of US assets.

Articles despairing the continued demise of London as a world leading financial centre to patriotic criticism for lack of support for 'our domestic market', continue to cause concern for investors. While all fascinating perspectives, we look at it from a slightly different angle.

The most enduring correlation in financial markets is the relationship between the price you pay for an asset and the longer term returns you get from it. A very common mistaken belief is that buying a great business automatically means that you will get great returns.

While it’s true that the US stock market gives investors access to world leading businesses, this comes at a price. Undoubtedly, it’s important to have meaningful exposure to the US, but we know we need to tread carefully.

Right now Microsoft is the most valuable company in the world and therefore arguably the 'best business', but had you bought it at its high in the TMT bubble in1999, you would have had to wait 17 long years to be up on your investment. Price matters.

We believe that the UK stock market could be sitting on the precipice of a re-rating. And rather than a single catalyst in the driving seat, we see a powerful combination of factors coming into play at the same time.

Valuations

Fundamentally, valuation matters. While the UK does not offer exposure to the big tech firms, there are other sectors that are just as important to get exposure to in a balanced portfolio. And they can be bought materially cheaper in the UK than the US.

Despite the strong recent performance of UK equities, the market remains cheap on both an absolute and relative basis. And crucially, the market is cheap against its own history.

US stocks demand a significant valuation premium to equivalent UK listed assets. The large energy firms are a fine example. Shell and BP are highly efficient energy businesses that are also at the forefront of the energy transition, investing heavily into renewables.

In contrast, US listed energy giants are a long way behind in this inevitable transition and still demand a significant valuation premium. UK businesses from this perspective are being unfairly penalised for investing in the future.

Buybacks and de-equitisation

The operational performance of UK PLCs has been strong, and the market in aggregate demonstrates robust cashflow generation while balance sheets are very healthy.

However, many firms have not seen this reflected in share price appreciation. This means that many are simply buying back and cancelling their stock, increasing both earnings and dividends per share.

A case in point are UK banks. They have been using their strong free cashflows to buy back stock well below book value, with a significant amount of their market capitalisation having been returned to shareholders in the past couple of years.

This has resulted in encouraging share price appreciation. In fact, around half of companies included in the MSCI UK Index have bought back shares in the past year, the highest percentage of any market in the world.

Macro

Inflation has been falling rapidly and it is probable that it will hit the 2% target again later this year. This may give the Bank of England wiggle room to cut rates and this cut may come before the Fed. This policy divergence will draw international attention back to the UK.

Furthermore, UK savings ratios remain elevated at circa 10% and the UK consumer could be in a position to drive a powerful cyclical recovery. This coupled with robust PMI data, the strongest in the G7, leads us to believe that only a small amount of monetary easing could increase consumer confidence and lead to a strong economic rebound.

UK politics

UK politics is no longer the tail risk that has plagued confidence since the Brexit vote. Indeed, the market barely registered the prime minister’s announcement of a 4 July election. This points to a less divisive contest than the US, especially with the opposition holding such a commanding poll lead.

Both Labour and the Conservatives appear relatively business friendly and understand the importance of functioning capital markets. In this sense we anticipate more market reform, with the British ISA likely to be just the starting gun.

Mergers and acquisitions

We’re all aware that overseas investors have started circling around the UK valuation opportunity and we have seen pick up in M&A from both private equity and corporates. Much of this is occurring in the cyclical part of the market, where valuations are particularly attractive, rather than the ‘fallen angels’.

This has largely gone unnoticed as the majority has occurred in the mid- and small-cap stocks. However, the bid for Anglo American is the kind of bell ringing M&A that really grabs attention.

UK firms have recently been generating strong returns and critically, from a risk-adjusted perspective, those returns are coming from different parts of the market to the US.

In an uncertain world, diversification and price remain paramount for investors and the valuation opportunity in the UK market is, we believe, too good to ignore.

Michael Toolan is co-chief investment officer at Brooks Macdonald. The views expressed above should not be taken as investment advice.

CC Japan Growth & Income has been removed after its co-manager retired and its investment firm’s assets shrank.

Fund platform AJ Bell has made the first change to its investment trust recommended list since June 2023 by axing Japan Income & Growth.

The £248m trust has been managed by Richard Aston since its launch in 2015, who co-managed the portfolio alongside Jonathon Dobson until his retirement at the end of April 2024.

Since inception it has been the best performer of the five IT Japan trusts with a long enough track record, making 125.3%, around 30 percentage points ahead of the TSE Topix benchmark and average peer.

Performance of trust vs sector and benchmark since launch

Source: FE Analytics

AJ Bell’s analysts lost faith in the trust however, for two main reasons. The first is that when Dobson retired, Aston took over fund management duties for the Chikara Japan Alpha fund.

Paul Angell, head of investment research at AJ Bell, said: “The fund has considerable differences to the CC Japan Income & Growth franchise, with a focus on small- and medium-sized companies with premium long-term growth prospects.

“As such, Aston’s time will be more thinly spread managing both strategies, particularly given the additional focus smaller companies tend to require.”

The other factor involves the asset management firm, which was rebranded from Coupland Cardiff to Chikara following the retirement of its two founders Richard Cardiff and Angus Coupland at the end of 2022.

The pair sold their stakes in the partnership at a time when the company’s assets under management “continued to shrink”, Angell noted, despite efforts to reverse the trend through the addition of an emerging markets franchise in 2023 led by Jonathan Asante.

The removal leaves Baillie Gifford Japan as the only trust in the IT Japan sector recommended by AJ Bell.

Angell said it benefits from Baillie Gifford’s “embedded investment process”, which has a “strong growth flavour” in line with the firm’s style.

“The strength of the team is another positive and while there has been a recent change with figurehead Sarah Whitley retiring, the succession planning over the years has now come to full fruition,” he said.

“However, investors may require patience with the trust given its significant style bias to growth, as the trust is very likely to significantly deviate from index returns.”

Multi-manager titans Witan and Alliance Trust announced they are to merge.

Alliance Trust and Witan are to join together in the biggest investment trust merger in history and create the industry’s sixth-largest investment company with around £5bn in assets under management.

The announcement, made this morning, comes after Witan had previously announced a strategic review of the £1.6bn trust, brought about by the impending retirement of chief executive officer Andrew Bell.

Alliance Trust’s investment manager, Willis Tower Watson, will manage the combined entity, which will be rebranded as Alliance Witan. Its investment process will be the same as the current £3.4bn Alliance Trust strategy, with different fund managers investing in 10-20 stocks.

The merger will propel the investment trust up the UK market in terms of its size and could potentially mean it is large enough to be included in the FTSE 100.

If this happens, passive funds investing in the FTSE 100 will be forced to buy the trust for the first time, while FTSE All Share trackers will be required to buy much more of the investment company.

While typically viewed as a key benefit for stocks, Darius McDermott, managing director of Chelsea Financial Services, said he was not convinced this would have too much of an impact.

“When you go into an index you get a surge in your share price because the index funds have to buy it, but in the long run it doesn’t matter,” he said.

However, there are reasons for optimism. For Witan shareholders, the charges drop is a significant benefit. At present, Witan charges 0.76% in ongoing charges (OCF), more than Alliance Trust backers are charged (0.64%).

Still, the combined entity will reduce costs further, however, down to a figure in the “high 50s” and McDermott noted that this was “welcome”.

“I would hold for the fee reduction alone if I owned it,” he said. It is worth noting however that investment trust charges are not the same as open-ended funds.

Witan’s shareholders could also benefit from markedly improved performance. Indeed, Alliance Trust has beaten Witan over one, three five and 10 years, with the former trouncing the latter by more than 100 percentage points over the decade, as the below chart shows.

Performance of trusts over 10yrs

Source: FE Analytics

Andrew Courtney, an analyst at QuotedData, suggested a key part of the decision to merge with Alliance Trust may well have been performance.

“[It] is likely in response to Witan’s ongoing poor performance with the trust one of the sector’s worst performers over the past 10 years,” he said.

“The deal with Alliance appears to be a good fit on first blush, given the similarities of the two funds – both are large global funds with multi-manager approaches – and is certainly a positive for both in our view given the benefits of increased efficiency that the combination will bring.”

On the news, shares in Alliance Trust nudged 0.7% higher in Wednesday morning trading, while Witan’s shares jumped 3.3%.

Samir Shah, fund research analyst at Quilter Cheviot, said the deal was “a positive move for both sets of shareholders”.

For those wishing to sell, however, around 17.5% of Witan’s shares will be eligible to be redeemed in cash at a price of 97.5% of the net asset value of the trust, with the remainder rolled into newly issued Alliance Trust shares.

“Both boards should also be recognised for their efforts including offering Witan’s shareholders an opportunity to tender their shares and for introducing measures to increase Alliance Trust’s yield to match Witan’s and maintain their AIC dividend hero status,” added Shah.

Dean Buckley, chairman of Alliance Trust, said the move was a “significant moment” for the investment management industry and represents a “key milestone in the history of the investment trust structure”.

Andrew Ross, chairman of Witan, added: “The companies share similar cultures and a mutual desire to provide a ‘one stop shop’ for retail investors in global equities.”

High yield bonds are less affected by interest rates, but investment grade bonds are a safer bet in credit terms.

With UK interest rates remaining at post-financial-crisis highs, and inflation continuing to nudge lower, fixed income assets still offer attractive levels of prospective returns, even after taking into account the effects of inflation.

Given this backdrop, corporate bond funds are naturally of interest for investors looking to generate additional income to that available on government bonds, money market funds and deposit accounts.

So, how should investors assess their options across credit markets? Is this the time for high yield funds? Or are investors better off with investment grade credit?

Well, as ever, the prospective return profile of any corporate bond fund relies on two risk factors, interest rate risk (duration) and credit risk.

Investment grade funds typically have higher levels of duration relative to high yield funds, as their higher-quality investee companies can issue their debt over longer time periods. This means that the price of investment grade bonds is more sensitive to movements in interest rates.

As, when interest rates rise, the future schedule of income payments on existing bonds becomes less attractive, resulting in a fall in the price of the bonds, and vice versa as interest rates fall.

High yield funds, by contrast, invest in bonds of companies that typically issue over shorter time periods, given their longer-term prospects are less clear to lenders. Movements in interest rates therefore have less of an impact on the return profile of high yield funds.

Credit risk, on the other hand, is naturally higher in high yield funds, as these lower-quality companies are more likely to renege on their repayment schedules. This higher credit, or default, risk necessitates a higher premium for investors to lend to these companies, hence the label ‘high yield’.

The structural benefit of holding high yield bond funds over investment grade bond funds is therefore the lower duration and higher yield on offer, whilst the structural drawback is the higher default risk, and therefore potential for greater volatility and losses during credit events.

Within the current macro environment, if the economy remains stable, interest rates hold and corporate defaults remain low, then high yield bond funds will almost certainly continue to outperform their investment grade equivalents.

However, should interest rate expectations fall and recession concerns build, high yield funds should struggle, and investment grade funds outperform.

Within some of our AJ Bell portfolios (risk profiles 1-4) we reduced our high yield exposure early in 2024, after having a relatively high allocation throughout 2023.

This followed a number of years where it has been the strongest performing area within fixed income markets given its lower interest rate and higher credit risk profile.

Essentially, at this point, we felt valuations had become somewhat tight in the market and that high yield no longer offered the relative value it once did versus other areas of the fixed income universe, particularly if developed market economies struggle under higher interest rates.

Meanwhile, whilst not enamoured by valuations within investment grade corporate bonds, we do continue to prefer them for the resilience they typically offer in economic downturns, alongside their higher exposure to interest rate risk at a time when interest rates are likely at their highs of the cycle.

We do continue to hold high yield within these portfolios, and, short of a large move in valuations, we are unlikely to make any further changes to the allocation in the coming quarters.

For higher risk portfolios that carry a narrower selection of fixed income (risk profiles 5 and 6) we have left the allocation to high yield unchanged as we feel its overall yield retains the ability to provide an ‘equity-like’ return but with lower volatility.

Two active funds we like to use to access the credit markets are the Artemis Corporate Bond and the Invesco High Yield funds.

Well-known bond investor Stephen Snowden and his team have done a fantastic job since the 2019 launch of the Artemis Corporate Bond fund, consistently delivering outperformance for investors from both a sector allocation and security selection perspective.

The fund is typically run with more risk than its index, with the risk allocation fluctuating between interest rate and credit risk depending on the team’s views.

That said, the managers are committed to keeping the fund’s duration within a fairly narrow band (1.5 years) of that of the index. This ensures the fund’s return profile remains equivalent to that of wider fixed-income markets.

Meanwhile, Tom Moore invests his Invesco High Yield fund across a combination of high yield bonds that are more highly rated (BBs), including sectors such as financials, and undervalued bonds he deems to be special situations.

Given the volatility of the latter two components, the fund is typically at the more volatile end of its market. The manager’s positioning in financials has been particularly additive to relative returns over the years, and he continues to see good opportunities in the sector.

Paul Angell is head of investment research at AJ Bell. The views expressed above should not be taken as investment advice.

The fund will complement Invesco’s Summit Growth and Summit Responsible funds.

Invesco has unveiled a fund of funds to help UK financial advisers deliver reliable income streams to their clients, particularly during retirement.

The Invesco Summit Income fund targets an income of 2-3% above the Bank of England Base rate over a 12-month rolling period, to be paid monthly. Invesco said the fund has been launched because of “growing demand for income, particularly from clients in the decumulation stage of retirement”.

Invesco Summit Income will generate income from both natural and enhanced sources, by investing in a wide range of asset classes and geographies. As well as income, the fund will focus on risk management and will use alternative investments in addition to traditional defensive investments such as bonds to dampen volatility.

Investing in both active and passive strategies, the portfolio will have at least 60% in debt securities, cash equivalents and money-market instruments while a maximum of 40% will be in equities, related securities and commodities.

It will be managed by David Aujla, John Burrello, Gwilym Satchell and Alessio de Longis from Invesco’s multi-asset strategies team and is designed to complement the team’s Summit Growth and Summit Responsible fund ranges by adding an income solution.

Aujla said: “As more investors enter the decumulation phase of their retirement journey there is increasing demand for investment solutions which provide steady income streams in an ever-changing landscape.

“We aim to deliver dependable income from a diverse, global range of sources within a tightly controlled risk management framework, so that investors can have the confidence in retirement that they need.”

M&A deals may be ‘a double-edged sword’ for UK investors, who get good immediate gains but can cause long-term problems.

Company takeovers can be an important driver of returns for investors but also represent a prospective danger lurking in the UK’s acquisitions-hungry market, according to experts.

Takeover activity in the UK picked up noticeably in the past few years, with the FTSE 250 particularly targeted by so-called “clever money” – private equity or trade buyers who see value where investors don’t want to look.

Ben Mackie, portfolio manager at Hawksmoor, said: “These deals, which are happening at 40%, 50% premiums to undisturbed share prices, are an indication of the value that exists in the UK. If public investors aren't interested in that value, then private market investors will take advantage.”

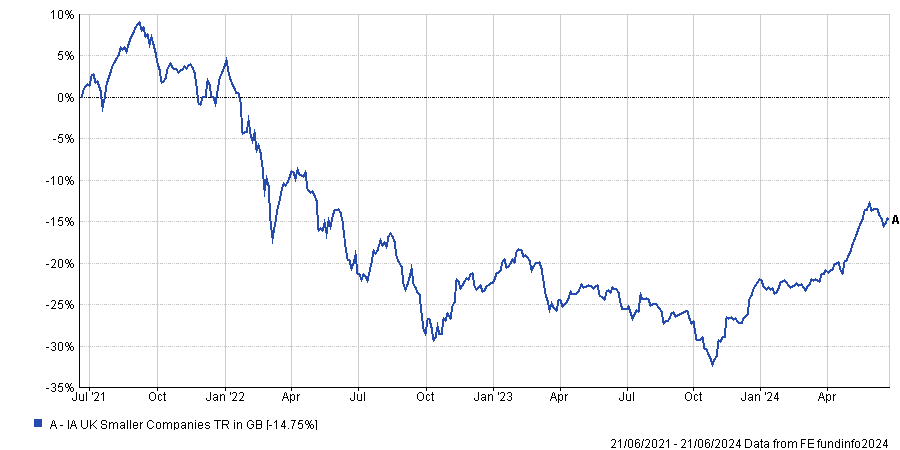

The small-cap end of the UK market in particular has had a terrible run in 2022 from which it has yet to recover, prompting a fund sell-off that still persists today. Pension funds have also turned their back to the domestic market.

Performance of sector over 3yrs

Source: FE Analytics

While takeovers have usually been seen as a blessing that could revitalise an unloved sector, there are enough setbacks for Mackie to describe it as a “double-edged sword”, leading to a smaller public market and a shrinking opportunity set for those who invest in it.

The situation is exacerbated by share buybacks and a reduced number of companies coming to market in the first place.

“If this trend continues, you end up with a small-cap market that doesn't exist in 10 or 15 years’ time,” said Mackie. “That's quite an extreme outcome, but if the trends that we've seen in the past couple of years continue then that might become a reality.”

On this background, UK equity managers find themselves in a tricky position and end up selling companies for cheaper than their intrinsic value.

“If a stock’s intrinsic value is £2 a share and it's currently trading at £1, in theory managers have a big potential upside. But if their funds are selling off because everyone hates the UK and the stock is depressed, it’s tempting when clever money comes along and offers to buy it for £1.50,” he said.

“It’s a 50% uplift on your share, you get liquidity and a lovely boost in your performance. But you're selling something that you still believe is a big discount to the true intrinsic value.”

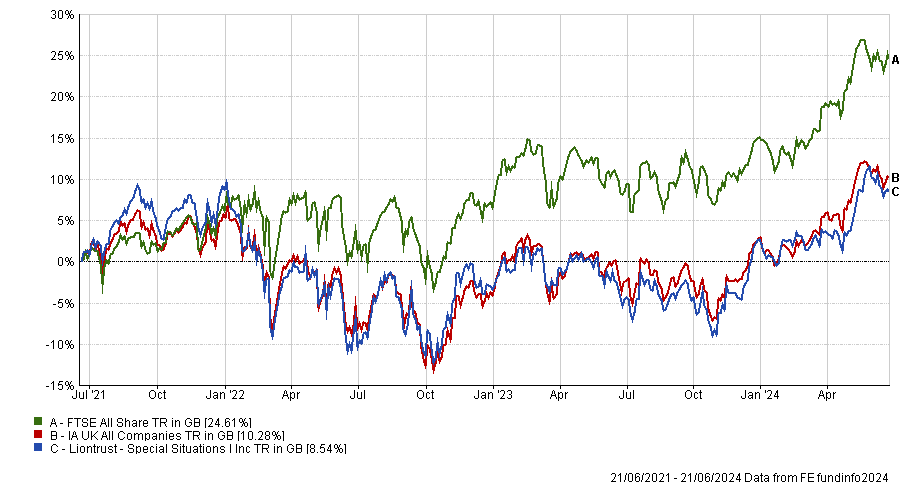

Alex Wedge, FE fundinfo alpha Manager of the Liontrust Special Situations fund, agreed, also describing takeovers as a “double-edged sword”.

Performance of fund against sector over 3yrs

Source: FE Analytics

“While we take a case-by-case approach to evaluating the merits of any incoming bid, there are wider considerations around the health of the UK market,” he said.

“The main examples are the de-equitisation caused by increased acquisition activity and fewer companies coming to market. But the outflows from UK equities are partly to blame for this dynamic, and we have been vocal supporters of policy change.”

That said, Wedge was “encouraged” to see some green shoots in the UK of late, such as Raspberry Pi, which came to market this month and the Liontrust UK Smaller Companies Fund bought a position in.

The Labour party manifesto committing to increase investment from pension funds in UK markets was also a boost, he noted.

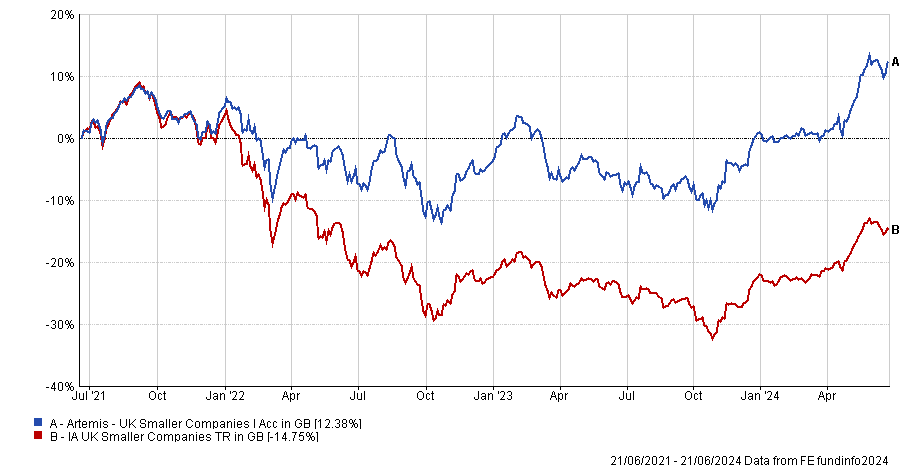

Not all were concerned, however. Mark Niznik and Will Tamworth, co-managers of the five FE fundinfo Crown-rated Artemis UK Smaller Companies fund, were happy to have extra cash from the sale to move on to other opportunities. Their fund has had 29 takeovers in the past five years, at an average premium of 50%.

Performance of fund against sector and index over 3yrs

Source: FE Analytics

“We need to recognise that, whilst it might be galling to sell shares for below what we see as ‘intrinsic value’, this may be in the interests of our investors if we are able to reinvest the proceeds in companies that are being valued at an even greater discount to intrinsic value,” they said.

“Despite all the recent takeovers, there is still plenty of choice. The talk of small-caps not existing in a few years is based on the narrow FT Small Cap index which ignores the small-caps in the FTSE 250 index, the Fledgling index and those on the AIM market.”

The managers also weren’t fazed by the dormant IPO (initial public offering) market, which has struggled as companies have refrained from listing into a market where there is little investor appetite.

“When valuations are low – something that is good for long-term investors – it makes sense that the number of takeovers exceeds the number of IPOs. When valuations correct, as we would expect them to, we would expect a growing number of IPOs thus replenishing the opportunity set. The number of IPOs has always been cyclical,” they said.

What do tractors, airplanes, paint and credit cards have in common? Baillie Gifford is invested in all of them.

Baillie Gifford has made a name for itself for investing in high growth companies with potential to make huge returns but there are some holdings that might surprise investors.

The firm has been among the early backers of some of the world’s largest companies, including high-profile investments in the likes of Amazon and Tesla, which have both soared.

From tractors to paint, there are a number of industries the firm invests in that many may not consider to be of the same calibre, but where the Edinburgh-based asset manager is staking a claim to future spoils. Below Trustnet highlights some of the firm’s more surprising stock picks.

Ryanair

First up is US and Ireland-listed budget airline Ryanair. The travel industry is notoriously cyclical, with profits dependant on the number of passengers carried.

It took a nosedive in 2020 when the world placed into Covid lockdowns, but has started to take flight recently and Baillie Gifford believes the firm is among those that stand to benefit the most from an increase in pent-up demand from travel-hungry consumers.

More recently, higher interest rates and inflation have pushed costs up, but again Ryanair has not suffered, according to Chris Davies, co-manager of the Baillie Gifford Euro Growth Trust. In fact, it is exactly this environment that has helped the stock to rise.

“It takes crises sometimes to accelerate market share and Ryanair’s market share over this crisis has gone up really quickly because all the airlines have retrenched. They’ve had to be recapitalised, issue debt and equity and have got themselves into all sorts of trouble,” he said.

Part of this is its ability to keep costs low. At Ryanair the average fare is about €50, while the average cost per passenger at one of its largest competitors (easyJet) is about €79, the manager said.

This is partially because the firm fits the brief for many during a cost-of-living crisis, offering cheap travel options. Chris Davies, co-manager of the Baillie Gifford Euro Growth Trust, said: “If you look at the average cost per passenger for easyJet it is about €79. That’s the story with Ryanair.”

Additionally, in an effort to keep costs low, the airline has started offering flights “to the back end of nowhere”, but locating them as near-city airports, something that has had “strong demand”, according to the fund manager.

“We’ve held Ryanair as a firm for a very long time. It is a growth business because partly because no one can match it,” said Davies.

Mastercard

Another area far from synonymous with Baillie Gifford is financials, yet the firm is keen on credit card provider Mastercard. Ben Drury, investment specialist at the firm, said it “sits at the heart of the global payments system” and “is the infrastructure upon which other payment applications are built”.

Mastercard should benefit from the rise of online payments around the world and is known as one of the safest and most reliable operators in the space.

“Since [Baillie Gifford] Global Alpha’s purchase in 2011, Mastercard has performed with remarkable consistency, with rising profitability and returns. Capital expenditure is minimal and cash conversion is around 100%,” said Drury.

The investment case for the stock is that the shift away from cash continues and its network remains the infrastructure bedrock for the industry, but there are reasons for even more optimism, said Drury.

“Longer term, there are new payment flows such as business-to-business (B2B), where there is the opportunity for MasterCard to take a leading role in the build out of the next generation, real-time, payment infrastructure. This will unlock the far larger B2B opportunity and create a durable moat that will drive sustained growth over the decade and beyond,” he said.

Kubota and Nippon Paint

Tractors may not be a natural fit for the Baillie Gifford stable, but $17bn Japanese tractor maker Kubota is another the firm is keen on.

Investment specialist Thomas Patchett said: “The focus remains on its inventory levels and its US operation (ride-on mowers for residential use), but the bigger/longer-term opportunity (we believe) exists in the automation of Asian paddy fields – an area of expertise it has finessed through decades of servicing the Japanese farmers.

“A stake in Indian business Escorts provides the company with an attractive entry into what is the world’s largest tractor market. Now trading at a decade low price-to-book ratio, the upside from herein looks increasingly exciting.”

The other shocking Japanese name invested in is Nippon Paint, a $16bn mid-cap painting business, which Patchett described as a “surprisingly attractive industry” for the firm.

Technically listed as an industrials business, he noted that paint has more going for it than traditional industrials thanks to being capital light, while the brand power that exists in the industry gives businesses a quality characteristic.

“Through subsidiary Nipsea, it provides us with exciting exposure to China, where Nippon Paint it is the number one provider of consumer paint,” said Drury.

“Although this market – and those involved – have been impacted by the property market slowdown, there remain several exciting long-term structural tailwinds for growth (per capita usage is still a third that of developed markets; wall space in meters-squared is equivalent to the US, India and Japan combined).”

Net zero, geopolitics and populism combined with high debt could lead to sudden spikes in inflation, according to Trevor Greetham.

Inflation may be on a downward trajectory, but there are plenty of potential shocks, Royal London Asset Management head of multi asset Trevor Greetham has warned.

Although resurging inflation is not his base case scenario, Greetham highlighted the drive towards net zero, geopolitics and populism as potential sources of inflationary shocks.

“Our economists are expecting inflation to fall further, but when you make economic forecasts, you do not include shocks, and there are lots of potential shocks out there at the moment,” he said. This makes it “quite plausible” that inflation could rise again.

In particular, he noted oil prices will have a big impact on whether the rate of price growth spiked higher, or remains manageable.

A consequence of the net-zero target is lower investment in fossil fuel capacity. While Greetham believes it makes “absolute sense” if economies around the world are planning to use much less fossil fuel in the coming decades, he warned that it also means a much tighter supply versus demand today.

“As we saw with natural gas prices last winter, if you interrupt supply, you get an immediate price move,” he said.

On geopolitics, further escalations in the ongoing wars in Ukraine and in the Middle East could create another inflationary shock.

As for populism, Greetham worries that it is combined with high levels of government debt.

“A lot of governments think the right thing to do now is to use fiscal policy, either because of rearmament or for populist reasons,” he said.

“If you look at what's happening in France, the far left and the far right disagree about almost everything, but one thing they agree on is that more money needs to be spent. High debt levels mean that there's a temptation to let inflation overshoot.”

Due to those potential, yet unpredictable inflationary shocks, Greetham believes investors will need inflation hedges such as commodities in their portfolios and to be more responsive to risks.

“You will also have to be willing to hold much less in fixed income when interest rates appear to be too low relative to the inflation outlook,” he added.

“If you only have stocks and bonds, you just need to look at what happened in 2022: they both lost money while commodities were up 30%.”

On average, Royal London has a 5% allocation to commodities in its multi-asset funds.

“We keep commodities in there as a hedge against inflation and we're quite ready to dial up if we see signs of an inflationary shock coming through,” Greetham said.

More generally, he explained that environments with sudden inflation spikes and surging interest rates tend to point to shorter business cycles and, therefore, a more volatile macro environment.

He added: “When we look back at the current environment in five or 10 years, we'll probably have been through several inflation shocks.

“It's not a new thing. If you think about the UK, we've had three big inflation shocks since 2008: the GFC when sterling collapsed and inflation surged, Brexit which led to a 15% devaluation of the pound at one point and then Covid.

“If you look at the real return of cash in the UK in the 1970s, you lost about 29% of your purchasing power by keeping cash on deposit over that decade. Since 2008, you've lost 39%. It’s been worse than the 1970s already.”

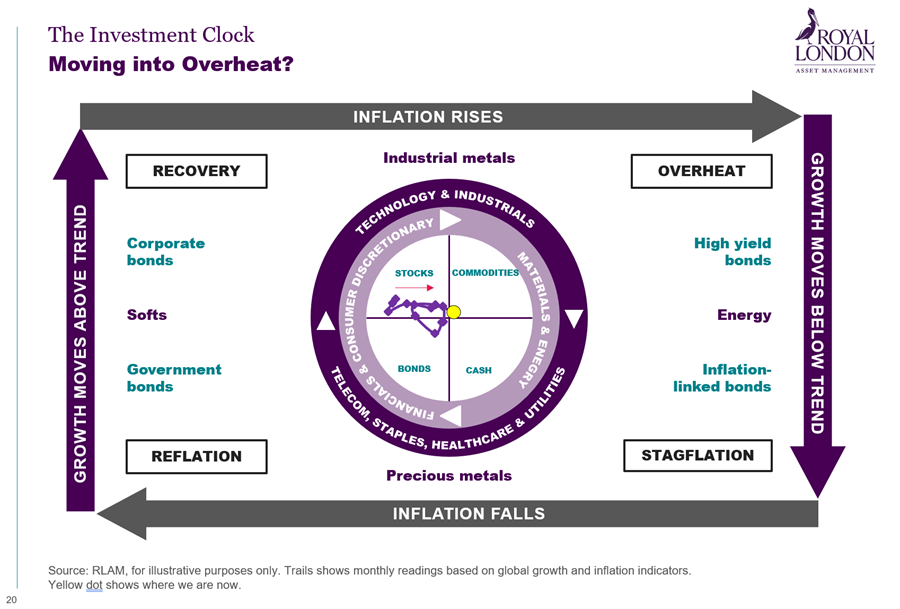

Although Greetham is mindful of inflationary shocks, he explained that economic indicators show low signals of either growth or inflation at this point in time. His assessment is that we currently are slightly in the overheat phase of the business cycle, but he stressed that it is not a high conviction call.

“At the moment, the growth indicators are okay, but if they were absolutely brilliant, that yellow dot would be higher up on our ‘investment clock’,” he said.

“Inflation indicators are also pretty balanced. If anything, they're pointing upwards, but if we had a stronger conviction, it would clearly be on the right-hand side. At the moment it's quite marginal.”

At this point in time, he is positioned for “okay growth” and inflation drifting lower and is, as such, overweight US stocks with a particular skew towards technology.

He concluded: “We are not in a bad situation. Economies are growing, there are signs of recovery in Europe and in the UK, things are not collapsing in America and inflation is alright.

“We’re in an environment in which central banks might squeak in a rate cut or two, but it's not weak enough for them to cut rates a great deal. I don't see the sharp downturn in growth that they would need to deliver a large series of interest rate cuts.

“I think there's a bit of a course correction going on here by central banks as they feel they can ease interest rates a little bit at the margin, but they don't need to do much more than that.”

There’s not enough knowledge about pension fees among investors.

Britons are unaware of the fees they are paying for their pension, new research from digital wealth manager Moneyfarm has revealed.

One in two pension savers of the 2,000 surveyed are not aware that they are paying annual fees on their pension schemes and, of the half that are, a further 50% don’t know how much they are paying. Only 32% have a rough idea of their costs and no more than 18% knew the exact amount. This financial blind spot can be a costly one.

Average annual charges on pension schemes are 2.5%, which is “way over what would be considered a reasonable amount”, according to Carina Chambers, pensions technical expert at Moneyfarm.

This too isn’t in line with investor perceptions, as 53% of the nation think their fees are competitive and only 23% have ever thought to shop around and switch providers to benefit from lower fees for the same service.

Costs deducted throughout the life of an investment “play an enormous part” in the final retirement pot. Chambers considers around 1% to be “a reasonable amount”.

“A seemingly small amount in fees can lead to significant shortfalls over the long term. The difference between 2.5% and 1% doesn’t seem much, but when it comes to pensions, we are talking about a large amount of money which is invested over a long period of time. That apparently small percentage difference therefore compounds, so the losses we are talking about can be very significant,” she said.

In fact, a 40-year-old’s pension pot worth £40,000 will be worth £78,000 by the retirement age of 67, assuming a 5% annual growth, no extra payments into the pension and a 2.5% management charge.

The same pot, but with 1% annual charges, accrues to a final £115,000.

“That small 1.5% difference in fees could mean an extra £37,000 in your pension – a significant 48% difference,” Chambers stressed.

Typically, pensions come with three main associated costs: fund fees; platform charges; and management fees.

“Frustratingly, these charges are often hidden in the small print or in footnotes of the contract, so you may be paying fees that you are unaware of which could be reducing the size of your pension pot,” she said.

“Costs can be very hidden. It may be easier to think ‘why bother finding out’, but you really shouldn’t put your head in the sand.”

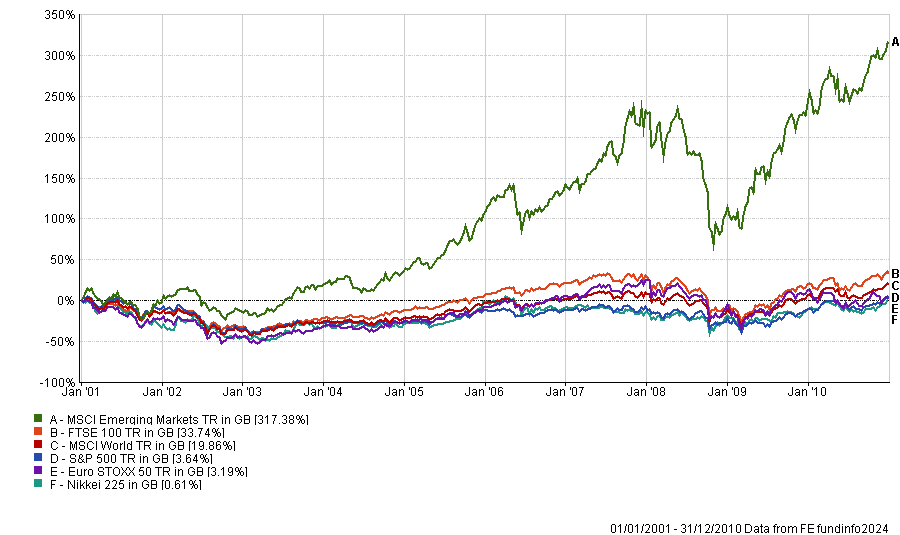

Global equity managers explain why the rest of the world is unlikely to catch up with US equities any time soon.

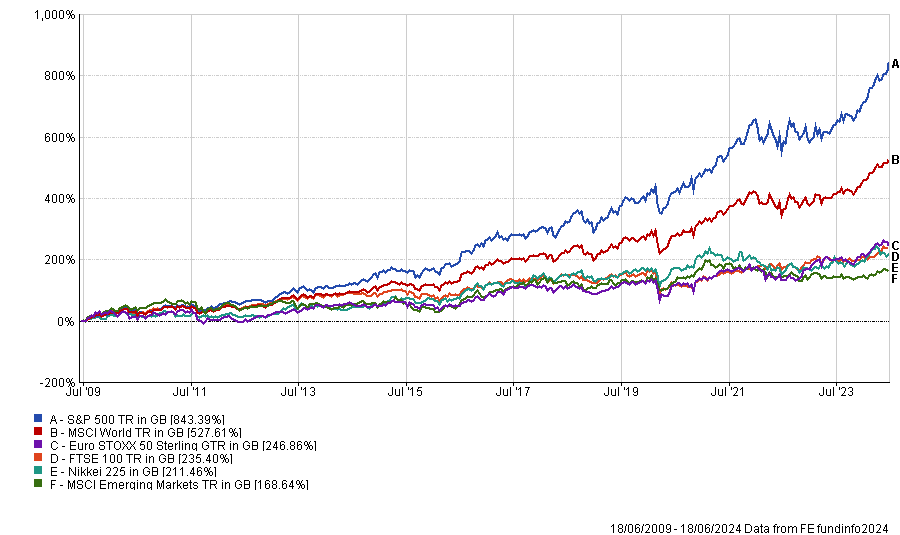

In his annual letter to shareholders in 2021, Berkshire Hathaway’s Warren Buffett urged investors to “never bet against America”.

History is on the side of the Sage of Omaha and US dominance has become particularly overwhelming since the global financial crisis.

Over the past 15 years, the S&P 500 has exceeded the Euro STOXX 50, FTSE 100, Nikkei 225, and MSCI Emerging Markets indices by roughly 600 percentage points, as the chart below shows.

Performance of indices over 15yrs

Source: FE Analytics

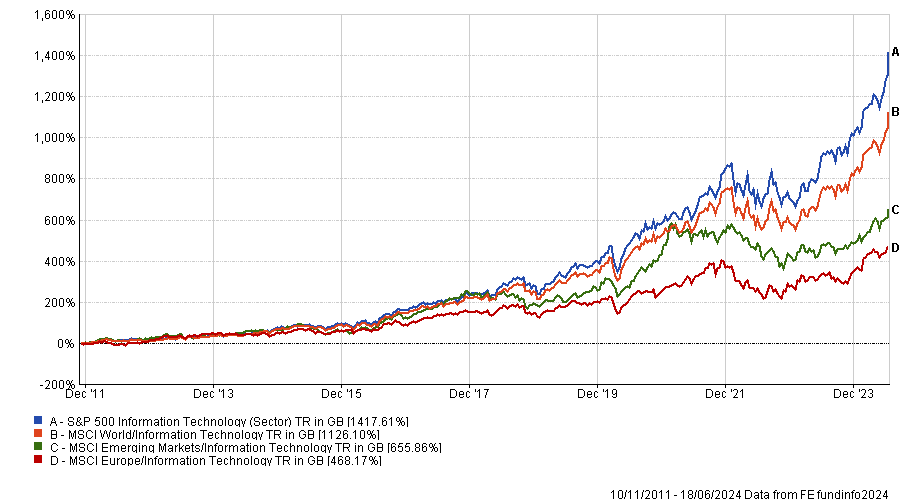

US exceptionalism has been underpinned by the technology sector, which is almost entirely dominated by American companies.

Ayesha Akbar, portfolio manager at Fidelity International, said: “The US is home to the majority of the largest and fastest growing tech companies in the world and this has helped propel US equity markets.

“Tech has fantastic margins and earnings growth, so even though the information technology sector has often looked expensive on valuations measures, earnings growth has always been there to deliver returns.”

Most non-US tech companies do not boast the same scale and significance as the Silicon Valley giants.

Gerrit Smit, manager of Stonehage Fleming Global Best Ideas Equity, noted that Europe only has one major technology company: ASML.

He said: “In America, you get the best of the new technology. We invest for future performance and it seems logical that it is going to come from technology. However, apart from China, there's no other region that really competes with America on that front.”

Performance of indices over 15yrs

Source: FE Analytics

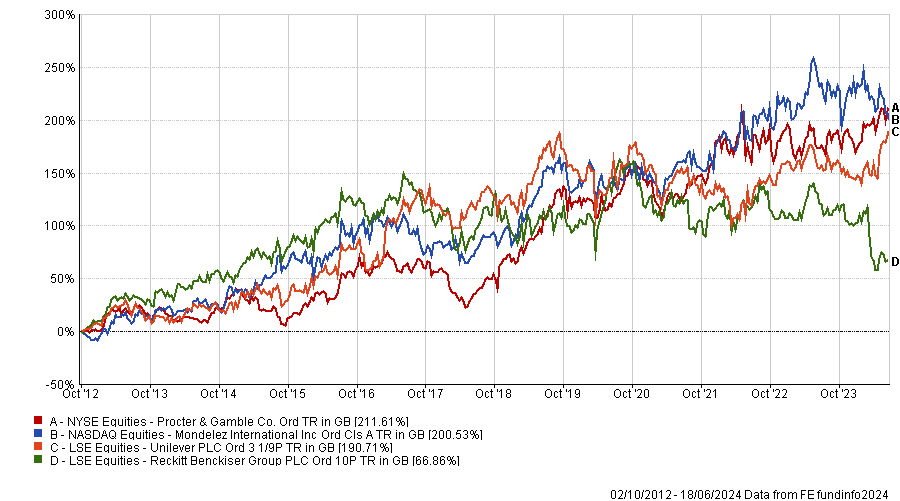

US equities have outperformed their global peers in non-technology sectors as well.

Matthew Page, manager of Guinness Global Equity Income, compared Mondelez and Procter & Gamble — two US consumer staples companies — with their UK equivalents, Reckitt Benckiser and Unilever. Over the past 15 years, the US duo has outperformed.

“I'm not entirely certain to what extent this is due to them being US-listed businesses or them having better management teams and benefiting from a more favourable market environment,” Page said.

“There are two things that tend to distinguish those US businesses relative to the European ones: growth and margins. American companies tend to deliver more top line and bottom line growth and they manage to do that with relatively high margins.”

Performance of stocks over 15yrs

Source: FE Analytics

Can the rest of the world catch up with the US?

The prolonged outperformance of US equities has opened up a valuation gap with the rest of the world. As a result, one could argue that American exceptionalism may stall, prompting investors to move to cheaper markets.

This would not be unprecedented. For instance, the S&P 500 did poorly in the 2000s, severely underperformed the MSCI Emerging Markets index and even lagged UK equities.

Performance of stocks between 1 Jan 2001 and 31 Dec 2010

Source: FE Analytics

Smit disagrees with the view that US equities are overpriced.

“We expect earnings growth for the S&P 500 to be close to 10% per annum over the next three years. If you divide that growth into the P/E ratio, you get a PEG ratio of 2.4. Against that, the PEG ratio for the MSCI World Index is 2.7. So, from a valuation perspective, despite the higher P/E multiples, I can also make a case for investing in America rather than in other regions,” he explained.

Page added that higher valuations for American companies are justified because they generate more profits per dollar invested. “Whether American companies are overvalued has been a constant question from investors over the past 15 years, but if you took the view that they were, you have missed out on some exceptional performance,” he said.

There are also macroeconomic factors that should benefit corporate America, such as better demographics.

Chris Iggo, chief investment officer for core investments at AXA Investment Managers, said: “There has been a surge in the US population in recent years. Between 2024 and 2054, the population is expected to rise from 342 million to 383 million. This is important because net immigration tends to mean a healthy growth rate in the working age population.”

Moreover, as the largest oil and gas producer in the world, the US is self-sufficient in terms of natural resources. Additionally, the US dollar is strong and close to a 20-year high against other major currencies.

The willingness to provide significant stimulus, as has been the case under the Biden administration, is another tailwind for US equities.

What could derail American exceptionalism?

Although valuations could be a concern in the short term, Akbar does not believe it will be enough to dethrone US equities.

The upcoming elections are causing some concerns, although Smith highlighted that both Republicans and Democrats are business-friendly.

Iggo said: “Any social unrest like the disorderly transfer of power seen in the wake of the 2020 presidential election could be harmful to economic growth.

“The geopolitical situation is also uncertain and the trade war with China could easily worsen.”

Iggo also raised concerns about persistent inflation in the US, which may prevent the Federal Reserve from cutting interest rates as quickly as anticipated, along with worries about the US federal government borrowing and the increasing cost of servicing debt.

Manchester & London has 32% in Nvidia and 25% in Microsoft and is trading at a 10% discount.

Nvidia became the world’s most valuable company last week with a $3.34trn market capitalisation, surging past Microsoft ($3.32trn) and Apple ($3.29trn). Watching Nvidia’s share price almost double so far this year has been either a rewarding or a painful experience for investors and fund managers, depending on whether or not they own shares in the chipmaker.

Victoria Clapham, an investment manager at private client boutique Manorbridge Investment Management, said several of her clients have been asking about whether they should increase their allocations to US mega-cap tech given the sector’s exponential performance.

One particular client inquired about investing in Nvidia recently. Manorbridge uses a combination of stocks, funds and trusts but in this instance, Clapham chose an investment trust to gain exposure to Nvidia at a discount – rather than betting the farm on Nvidia’s top-performing but potentially volatile shares.

“If you’re going to buy tech, buy it at a discount [so] you’ve got a bit of cushioning there,” she said. Clapham is concerned about the high valuations of US mega-cap tech stocks but admitted it is a “quandary” because “it could just keep going up”.

Clapham chose Manchester & London, which has 32.3% in Nvidia and 24.9% in Microsoft (as of 28 May 2024) and is trading at a 10% discount. The trust is fairly concentrated in just two stocks so “you’ve got to know what you’re buying”, she pointed out.

The trust is managed by Mark Sheppard and Richard Morgan at M&L Capital Management. Given its concentration, performance is likely to vary markedly from broader technology indices, they said in the trust’s annual report.

“Should either Nvidia or Microsoft have materially adverse events, or the monetisation of artificial intelligence (/AI) by the sector in general be slower than expected, then the fund will suffer material losses. Humans have a tendency to want everything now,” they wrote.

“The consensus solution to concentration risk is diversification but so often when one does diversify, one has to diversify into lower quality holdings.”

Recent performance has been exponential. The trust, which has a market capitalisation of £318m, delivered a total return of 82.5% for the 12 months to 19 June 2024 in sterling terms. It was the best performer in the IT Global sector by a wide margin, ahead of Scottish Mortgage in second place, up 31.3%.

Manchester & London topped its sector over three and five years as well, although the gap between itself and other trusts was smaller. It came second over 10 years after Scottish Mortgage.

Investors would have been better off buying shares in Nvidia directly, however. Its share price has climbed 216.9% in the 12 months to June 19 in dollar terms. Microsoft’s performance was measly by comparison, up 31.6%.

Over five years, Nvidia is up an eye-watering 3,551.7% in dollar terms. Manchester & London didn’t come close; it returned 86.1% in sterling (87.5% in dollar terms).

Beyond Nvidia and Microsoft, Manchester & London also has 7.8% in Advanced Micro Devices, 6.7% in ASML, 5.9% in Synopsys, 5.6% in Arista Networks, 5.5% in Synopsys, 4.6% in Cadence Design Systems and 4.0% in Alphabet.

Sheppard and Morgan are focussing on ‘hard technology’ (high intellectual property, mission critical, recurring, low churn) rather than ‘soft technology’ (social media and easily created apps, such as food delivery).

Another way to gain exposure to technology at a discount and access some diversification would be through a specialist technology trust.

The £1.5bn Allianz Technology trust and the £4bn Polar Capital Technology trust are trading at discounts of 8.9% and 8.8%, respectively. Nvidia is both trusts’ largest holding, with a 9.6% and 10.4% weighting, respectively.

They are more diversified than Manchester & London, but this means they do not benefit from Nvidia’s stellar growth to the same extent. They produced total returns of 52.6% and 52.2%, respectively, for the year to 19 June 2024.

Performance of trusts over 1yr

Source: FE Analytics

Trustnet recently compared the two tech trusts and asked experts to choose between them.

Shavar Halberstadt, equity research analyst at Winterflood, and Ryan Lightfoot-Aminoff, investment trust research analyst at Kepler Partners, both backed Allianz Technology.

Its manager Michael Seidenberg invests in more off-benchmark names, implying that he has a better chance of beating his benchmark, Lightfoot-Aminoff said.

However, Richard Williams, an analyst at Quoted Data, preferred Polar Capital Technology because it has taken a bigger bet on AI. It holds Advanced Micro Devices, for instance, which should benefit from the insatiable demand for chips and increasing AI infrastructure.

Other trusts trading at a discount that have more than 5% in Nvidia include Scottish Mortgage, Martin Currie Global Portfolio, Canadian General Investments and Baillie Gifford US Growth.

Four themes suggest we’re about to see a broadening of equity opportunities in the second half of this year.

Lofty tech stock valuations, rate cut delays and geopolitical shifts may have investors worried about what’s next for equities in 2024. But, while risks of an economic slowdown remain, the potential for unlocking new shareholder value is also strong. Despite the potential for slower growth, we see four sector trends which are particularly encouraging.

Healthcare bounces back from a bear market

After a multi-year bear market, many biotechnology stocks still trade below the value of cash on their balance sheets. Meanwhile, the broader healthcare sector’s total return lagged the S&P 500’s by more than 20 percentage points in 2023, suffering from a sharp slowdown in Covid-related product sales.

And yet, the healthcare sector is ripe with innovation. Last year, the Food and Drug Administration approved a record 73 novel medicines. These drugs are now beginning what will likely be a 10-year revenue cycle, including in new end markets with multi-billion-dollar sales potential. Recently approved GLP-1 drugs for diabetes and weight loss, for example, are already annualizing more than $30bn in revenue and are forecast to reach roughly $100bn in sales by the end of the decade.

AI set to spread and strengthen

As in 2023, artificial intelligence (AI) has been one of the biggest market narratives in 2024. This year, however, the trade has started to evolve. Only five of the Magnificent Seven mega-cap tech companies that rocketed into the stratosphere last year have continued to see gains in 2024. Meanwhile, other stocks are starting to catch what looks like an AI tailwind.

For example, since October 2023, utilities have rallied sharply. A recovery trade and the prospect of falling rates likely explain part of the gains, but another reason could be a growing appreciation for the energy demands that AI is creating.

The data centres that train and host generative AI programs are expected to account for an estimated 8% of electricity usage in the US by 2030, up from 3% in 2022. That, in turn, is forecast to drive sizable investment in energy infrastructure, boosting utilities’ long-term earnings growth potential.

We see similar stories beginning to play out in other areas of the economy, building a case that AI is still in the early chapters of its story. As such, we believe mega-cap tech companies that continue to invest and innovate in AI could see more revenue and free-cash-flow growth.

Valuation gaps present opportunities in China

The continued outperformance of US tech has exacerbated a global gap in equity valuations.

The spread has grown so much that any whiff of positive news can lead to big rallies for beaten-down markets. Hong Kong’s Hang Seng Index, for example, was among the worst-performing indices in 2023 (down -10.5%), as well as during the first quarter of 2024 (-2.5%). Then, in mid-April, the benchmark did an about-face, surging more than 20% in one month as news of government stimulus combined with rock-bottom valuations.

But China is also up against some acute challenges, including a distressed property market, lacklustre consumer demand, and mounting trade tensions that threaten to curb Chinese exports – a main driver of recent economic activity. So, while some Chinese corporations have exciting growth stories, an investment strategy based on valuation alone could face near-term volatility.

European markets make a case for themselves

Encouragingly, fundamentals are turning more positive in other markets. In areas where valuation and fundamentals unite, potential exists for stocks to rerate higher more consistently.

In Europe, for example, GDP grew faster than expected in the UK and the European Union in the first quarter of 2024. As such, European indices have traded largely in line with the US year to date.

There are reasons to believe the positive momentum can continue: roughly 18 months of inventory destocking in manufacturing is winding down and both the Bank of England and European Central Bank have signalled the potential for at least one rate cut in 2024.

Europe has also nurtured its own group of mega-cap leaders in sectors such as healthcare, semiconductors, and retail. And it has overseen a 62% rise in military spending from a decade ago, which is swelling the order books of European defence contractors.

These four overarching trends all point to a broadening of equity opportunities for the remainder of 2024. Investors should look for a combination of fundamentals and valuation, especially amid elevated interest rates and wider risks to economic growth.

Lucas Klein is head of EMEA and Asia Pacific equities at Janus Henderson Investors. The views expressed above should not be taken as investment advice.

A Labour government might be priced in but some UK stocks could have further to run under a new administration.

Lloyds, Taylor Wimpey and JD Wetherspoon are among the stocks that could benefit from a Labour victory at the looming general election, according to analysts at investment platform Hargreaves Lansdown.

The UK will go to the ballot box on Thursday 4 July, with the polls showing the Labour party likely to win by a considerable majority. While investors are not expecting this to spark a strong market reaction, there might be some key beneficiaries.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, said: “While the nation appears to have become obsessed by politics during the general election campaign, the impact they have on financial markets is likely to stay more minimal – especially Britain’s blue-chip index, given its international focus.

“The Labour party has been ahead in the polls for many months and has widened its lead. There could be a tailwind for certain sectors and stocks if the expected result turns up even though a win for Keir Starmer has largely been priced in.”

Below, we look at 10 stocks that Hargreaves Lansdown thinks might be among those that do well under a Labour government.

Housebuilders: Taylor Wimpey and Vistry

First up, Streeter pointed to Labour’s pledge to shake up the planning system and fast-track urban brownfield sites for development, in the hope of building 1.5 million new homes.

This would help housebuilders such as Taylor Wimpey, which have been hampered by slow approvals of projects and higher interest rates. However, rate cuts appear to be on the horizon while a promise to extend the mortgage guarantee scheme should bolster demand

A Labour administration’s expected emphasis on constructing more affordable housing would also be beneficial for Vistry, which partners with housing associations to provide affordable housing.

“Although these projects tend to be lower margin, if they can be approved in greater volumes it bodes well for its business model,” Streeter said. “Partnership revenues are typically more defensive than those from ordinary housebuilding operations. The need for more affordable private and social housing shows little sign of going away even if the economy doesn’t improve significantly.”

Construction: Balfour Beatty

Meanwhile, construction contractors such as Balfour Beatty stand to benefit from pledges to improve roads, schools, hospitals and other elements of national infrastructure. The public sector accounts for more than 95% of future orders in Balfour Beatty’s UK business and the impact of a government-led infrastructure boost would be significant.

But investors need to keep in mind that some of its projects have been delayed because of higher borrowing costs, mainly in the US, which could continue to hamper the wider business if interest rates remain higher for longer, according to Hargreaves Lansdown.

Banks: NatWest and Lloyds

The pledges of funding for infrastructure could also lead to a modest boost in GDP, Streeter argued, which may help UK-focused banks such as NatWest and Lloyds.

“NatWest has been showing signs of promise with loan default levels remaining low and with the return of real wage growth, plus an improving housing market, borrowers look set to remain resilient,” she added. “If the economy does continue to recover as expected, this trend should help put NatWest in a more resilient position, especially with easing conditions in the mortgage market appearing.”

She described Lloyds as “another piece of the unloved banking sector”, but said this bank – which is often seen as a bellwether for the UK economy – would also benefit from the improved consumer confidence that would follow a change in government.

Bricks & mortar store chains: Associated British Foods and J Sainsbury

Labour’s plan to overhaul the business rates system would support high street operators by levelling the field between bricks & mortar chains and online giants such as Amazon.

Chains with large footprints in town and city centres such as Primark owner Associated British Foods (which has not gone down the online-only sales route) and supermarket giant Sainsbury’s (where the pandemic’s surge in digital sales has reversed) could benefit from this change.

“If a Labour win is accompanied by a confidence lift, caused by optimism brought by the winds of change, it could also help consumer sentiment and provide a tailwind,” Streeter said.

Health: Primary Health Properties

Another stock to watch in a Labour victory is Primary Health Properties (PHP), which is a real estate investment trust that provides purpose-built doctor's surgeries. It would benefit from the stable growth environment created by pledges to add another 2 million appointments to the healthcare system and recruit another 8,500 staff, specifically to work in mental health.

“PHP has successfully navigated the era of higher interest rates even though it’s had an impact on the value of the portfolio,” Streeter said. “The company has focused on squeezing more from existing locations and, with more demand expected at bricks & mortar properties amid a lack of new supply, this has given PHP more bargaining power in terms of rent increases. With investment in primary care facilities also likely to increase, PHP is well placed to benefit from further opportunities.”

Pub companies: JD Wetherspoon and Mitchells & Butlers

Finally, Hargreaves Lansdown highlighted JD Wetherspoon and Mitchells & Butlers as hospitality stocks that would benefit from Labour’s promised business rates reforms, while the proposed establishment of Great British Energy could also help keep energy costs down.

“JD Wetherspoon’s Tim Martin has long been a vocal campaigner for tax parity between supermarkets and pubs. Either way the company is better placed than most in the sector to deal with changing market conditions and should continue to build market share,” Streeter finished.

“Mitchells & Butlers, whose brands include the likes of Harvester and All Bar One, is another name that’s impressed of late with market-beating sales growth.”

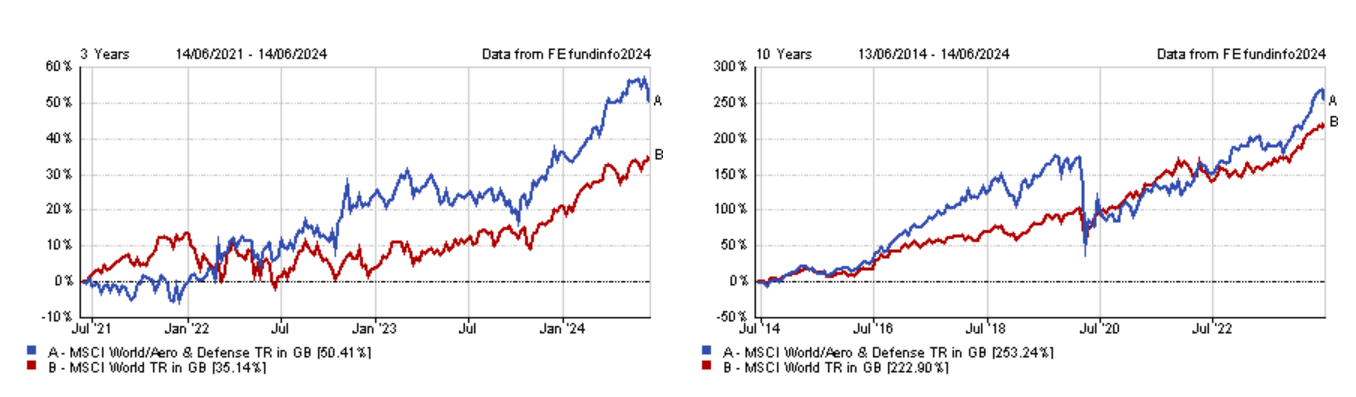

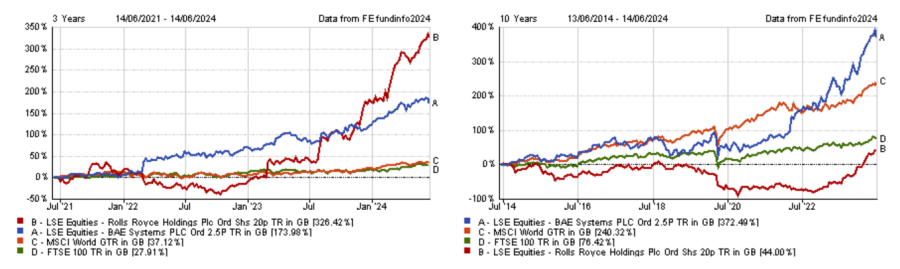

The Future of Defence UCITS ETF provides exposure to a sector “virtually guaranteed to attract increased spending”, experts believe.

The defence sector has proven to be a rewarding investment, which implicitly suggests that the ‘peace dividend’ era that followed the end of the Cold war is now over.

This has translated into outperformance for the MSCI World Aerospace and Defence sector compared to the broader market over the past three years, as well as over the past decade.

However, due to ethical and reputational considerations, it is a sector that fund managers are not always keen to delve into. Yet, with no signs that geopolitical tensions will abate in the foreseeable future, the defence sector may well continue to thrive.

Performance of indices over 3yrs and 10yrs

Source: FE Analytics

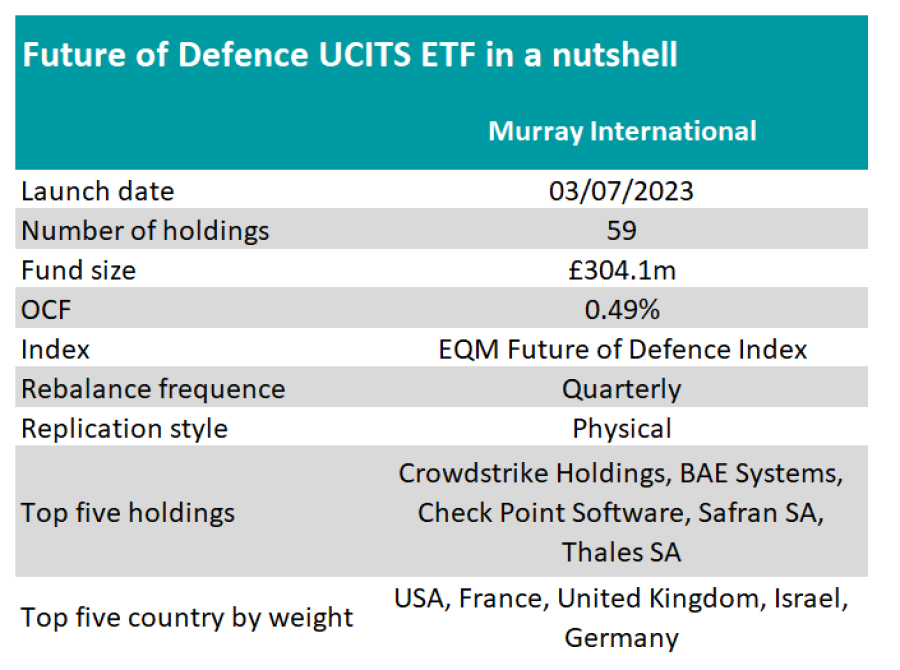

Therefore, HANetf launched the Future of Defence UCITS ETF in July 2023 for investors keen on gaining exposure to the sector but not comfortable with the idea of cherry-picking their own defence stocks. Despite the recent outperformance, experts believe this thematic ETF still has the potential to be rewarding.