Brown Advisory is taking ‘skin in the game’ to the next level.

There is a big debate in the investment management industry on whether fund managers should have significant amounts of their own money invested in their funds.

On the one hand, putting their own cash in aligns interests with shareholders, which in theory should keep them from making poor decisions. On the other, some argue their salary and bonuses are already linked to their portfolio’s success, so there is no need.

Mick Dillon and Bertie Thomson seemingly take the former view, piling almost all of their own money into the Brown Advisory Global Leaders fund, which they co-manage together.

Dillon said: “Bertie and I have only two investments. We are partners and shareholders at Brown Advisory and we invest in Brown Advisory Global Leaders and that’s it. We’re all in: my wife's money's in, my kids money's, everything is invested. I'm a big believer in people who eat their own cooking and put their money where their mouth is.”

Of course, this comes with its own concerns, such as whether the fund is risky and if it is suitable as a one stop-shop. Dillon had an easy response, however: “Clearly, I don't think it's that risky or I wouldn't have everything in it.”

His confidence comes from his companies’ fundamentals, with an average return on capital more than twice that of the broader market. “They typically grow faster than their industries because they are taking market share,” he said.

Although valuations are “maybe 15-20% more expensive than the benchmark on a one-year view”, over the longer term, "you're going to compound something that's twice as good as the benchmark for return on capital and is growing slightly faster, and you only paid 15% more".

Fortunately for the managers, Brown Advisory Global Leaders has delivered top-quartile returns over three and five years and pulled ahead of both its sector and benchmark since inception in November 2017, as the chart below shows.

Performance of fund vs sector and benchmark since inception

Source: FE Analytics

Below, Dillon tells Trustnet about his rules for selling and how he works with behavioural coaches to make better decisions.

What is a global leader?

For every investment we ask: how does that company help its customers solve a problem or achieve their goals? Frankly, how do they make their customers’ lives better?

When you get a business whose customers are happy, who come back again and again because the business is solving a problem and creating value for them, that company will have a long relationship with its customers. Ultimately, that’s what creates a ton of value for shareholders.

We have a team of investigative analysts who talk to customers to understand why they want to come back. Our favourite piece of feedback is when a customer says, ‘it’s not cheap, but it represents good value’. That tells you it’s not about being the cheapest on the market, it’s about solving customers’ broader problems.

What do you look for in a stock?

We look for a 20% or higher return on capital, which means these companies are efficient at turning revenues into cash flow. Then lastly, it has to be cheap. We want double-digit returns in the strategy on an absolute basis. With every investment, we need to believe we can make 10% a year for five years, so over 50% compounding.

What’s has been your best investment recently?

General Electric (GE) is already up more than 70% since we bought it in April/May last year. It has a 70% global market share in narrow-body aircraft engines. Its engines are more fuel efficient than anyone else’s, which saves money for airlines and is also great for the environment. Its after-market business, which sells parts to maintain planes, is incredibly valuable for customers and profitable for GE.

And your worst?

Not investing in Nvidia. In October 2022 we did a full investment review of Nvidia. At the time, it was within 5-10% of what we thought was a five-year, double-digit annual internal rate of return, so easily a 50% upside.

But we didn’t invest because we wanted to buy it 5-10% cheaper and we fundamentally mis-calibrated what artificial intelligence (AI) was going to do for that business.

How do you work with behavioural coaches?

We sit down with a behavioural coach once a quarter who uses data and analysis to help us avoid classic behavioural mistakes. We've got a whole bunch of processes now to use in different scenarios. I think of them as game plans.

One of our rules is, if an investment falls 20%, we either have to buy more or get out. About 70% of the time it works, so it's not perfect, but the odds are in our favour. That changes the psychology in the room from a negative event where we've lost money, to a positive event where I can tell you with 70% certainty that we'll make a good decision today.

In February last year, Google did a disastrous product demonstration and was considered an AI loser. We had to do a drawdown review on it; either buy more or get out. We bought more.

At the drawdown reviews we ask, will I care about this issue in five years’ time? I don't think I'm going to care about Google’s bad product demo.

We think it’s highly unlikely that anyone will disrupt Google’s search or cloud businesses. The transformer technology that enables generative AI – the ‘T’ in ChatGPT – was invented at Google.

How has working with coaches impacted your sell discipline?

If we're selling for a broken thesis, more often than not, we're right and the stock continues underperforming, so our rule is to get out within a week. That came from working with the coach.

When we sell on valuation, we always sell too early, but that's okay because we're going to take that capital and put it somewhere else.

What do you enjoy doing outside of investing?

I grew up on a farm in rural Australia so I like anything outdoors to switch off. I enjoy cycling, surfing, hiking, even gardening.

People are looking towards the stock market again, but could be repeating their mistakes.

Markets have gone gangbusters over the past few years and investors have finally decided to take the plunge and get back into stocks.

This is according to the latest Schroders UK Financial Adviser Pulse Survey, which showed 49% of advisers reported that their clients, who have been holding cash over the past few years, are now more likely to consider returning to investment markets or have already invested.

It is understandable why investors waited for the market to calm down. In an era of rising rates, many chose to pull their money out of stock market investments and channel it into cash savings accounts and money market funds, which offered decent returns for the first time in more than a decade.

Yet perhaps the question should be why now? On the face of it, it makes logical sense. Markets have held up surprisingly well over the past two years, despite inflation and interest rates rising sharply. Since January 2022, for example, the S&P 500 is up 24.3%, despite losing 8.3% in 2022.

In theory, with interest rates peaking – and likely to come down in the coming months across the world – this should benefit big companies such as the Magnificent Seven tech names, which should have been hit hard by rising rates.

Higher rates, after all, increase the discount rate. Or put more simply, why pay up for a growth stock with high risk in the hopes it can deliver future returns, when you can get more than 5% in a bank account today?

But there is a chance that investors have left it too late. For example, despite being hammered in 2022, the S&P 500 Information Technology sector has rocketed and is now 54.1% higher than it was at the start of 2022. Many could have therefore missed the boat.

Yes interest rates are expected to fall, but the market has, in my view, become too myopic on this one data point.

Overlooked factors, such as wars breaking out around the world, elections in hundreds of countries and the perceived end of globalisation through trade tensions – particularly between China and the US – make the situation less straightforward than simply: ‘interest rates will fall so stocks should do well’.

For an example of this, we do not have to look too far back in history. The Schroders report noted 41% of advisers reported that their clients are now bullish compared with only 17% in November 2023, while just 10% are bearish.

This is the strongest balance of sentiment since May 2021 when market optimism surged as economies started to recover from the initial impact of the pandemic and first lockdown.

Here investors were singularly focused on the Covid recovery narrative and eschewed fundamental investment principals. They focused on the feel-good story. Yet while those that invested in May 2021 enjoyed some upside early on, they would have then been hit by the falls in 2022.

As mentioned, those that held on for the long-term have been rewarded in the years since, but it is human nature to sell when things are falling. Which is something we can infer from the data, with many clients moving to cash in 2022 as markets were falling.

There are good reasons to invest today but investors looking to get back into markets on the hopes of interest rates falling should remember that it is often something unexpected that derails markets.

Therefore, it is crucial that any money added over the coming months is with the knowledge it will be tucked away for years, and won’t be pulled out at the first signs of trouble.

Rob Morgan, chief investment analyst at Charles Stanley, thinks there are bargains to be had amongst UK equities, mining companies and Japanese growth small-caps.

Investors have benefited from several rallies since the beginning of the year, with a range of indices reaching all-time highs, including the S&P 500, the Nikkei 225 and even the FTSE 100. This has left some investors feeling uneasy about lofty valuations.

For investors on the lookout for more attractively-priced opportunities, Rob Morgan, chief investment analyst at Charles Stanley, pointed to three underappreciated sectors.

First up is the UK, which despite the recent rally, remains cheap compared to its international peers and its own historical valuations.

Although Morgan finds UK equities attractive across the board, small- and mid-cap (smid) stocks are even cheaper than FTSE 100 blue-chips and should benefit from an improving economic backdrop, as well as renewed interest from private equity buyers, he said.

Moreover, the liquidity profile of UK equities, especially in the smid-cap space, has significantly diminished, which means “it won’t take much for them to surge”, according to Morgan.

For investors hoping to benefit from a re-rating of UK cheap stocks, he suggested Fidelity Special Values and Man GLG Undervalued Assets.

“Fidelity Special Values focuses on finding underappreciated bargains in an already cheap market,” he said.

“Man GLG Undervalued Assets also adopts a value-focussed approach while aiming to ensure good quality.”

Performance of funds over 10yrs vs benchmark

Source: FE Analytics

Although Morgan has a preference for UK smid-caps, he also expects the FTSE 100 to perform well. Given its large weightings in banks, oil companies and commodities, persistent inflation should be a tailwind for the blue-chip index.

Mining is another underappreciated area that Morgan highlighted.

Although mining companies have faced issues such as poor capital discipline, failure to control costs and overleverage in the past, they are now benefiting from the transition to a low-carbon economy.

Morgan said: “It will require a lot of raw materials, especially metals and we’re now seeing a scramble for raw materials. In spite of this, mining companies are under-owned as their growth potential is underestimated.”

Miners tend to pay dividends, although they can be lumpy. Morgan also warned that mining is a highly volatile sector and that investors should get in with a five- to 10-year view.

For investors capable of stomaching this volatility, Morgan recommended WS Amati Strategic Metals.

Performance of fund over 10yrs vs benchmark and sector

Source: FE Analytics

“The fund takes a highly active approach to investing in the mining sector, aiming to actively manage an optimal combination of precious, specialty and base metals at any given time,” he explained.

“It holds a concentrated portfolio of 35 to 45 companies, including higher risk smaller stocks, so the individual selection by its managers will have a significant bearing on returns. In particular, it targets specialty metals companies which will play a future role in the global energy transition such as battery metals like lithium which is vital in electric car batteries.

“It’s definitely not for the faint hearted but could be an interesting satellite holding in a portfolio for the long term.”

Finally, Morgan also finds Japanese small-cap growth stocks compelling, as they remain attractively valued compared to the rest of the market.

Japanese large-cap exporters have made significant strides in a short amount of time as corporate reforms narrative has played out, with the weak yen providing an additional tailwind. Therefore, they are not as cheap as they used to be.

However, Japanese companies focusing on the domestic market haven’t benefited to a significant degree from those tailwinds, especially in the small-cap growth space where valuations have derated as global interest rates rose and the yen fell.

As a result, they are now far cheaper and widely overlooked, but could benefit from global interest rate cuts as well as their own organic growth over time.

To gain exposure to this space, Morgan highlighted Baillie Gifford’s Shin Nippon trust, which has struggled since late 2021.

Performance of investment trust over 10yrs vs benchmark and sector

Source: FE Analytics

“Shin Nippon’s collection of small, more growth-orientated companies have been of little interest to their traditional domestic buyers who have favoured dollar-earning exporters or simply investing overseas.

“However, following a brutal derating, there appears to be value on offer with growth companies on undemanding valuations. It might be a slow burn, but as sentiment improves and, ideally, the yen stabilises, it could be a profitable area to focus on,” Morgan explained.

“This trust is a higher risk option in an already-specialist area as it has gearing of around 20%, plus the discount to NAV of the shares fluctuates. At the moment it is around 15%, but recently it was as much as 20% having traded at a very small premium at the start of 2022.”

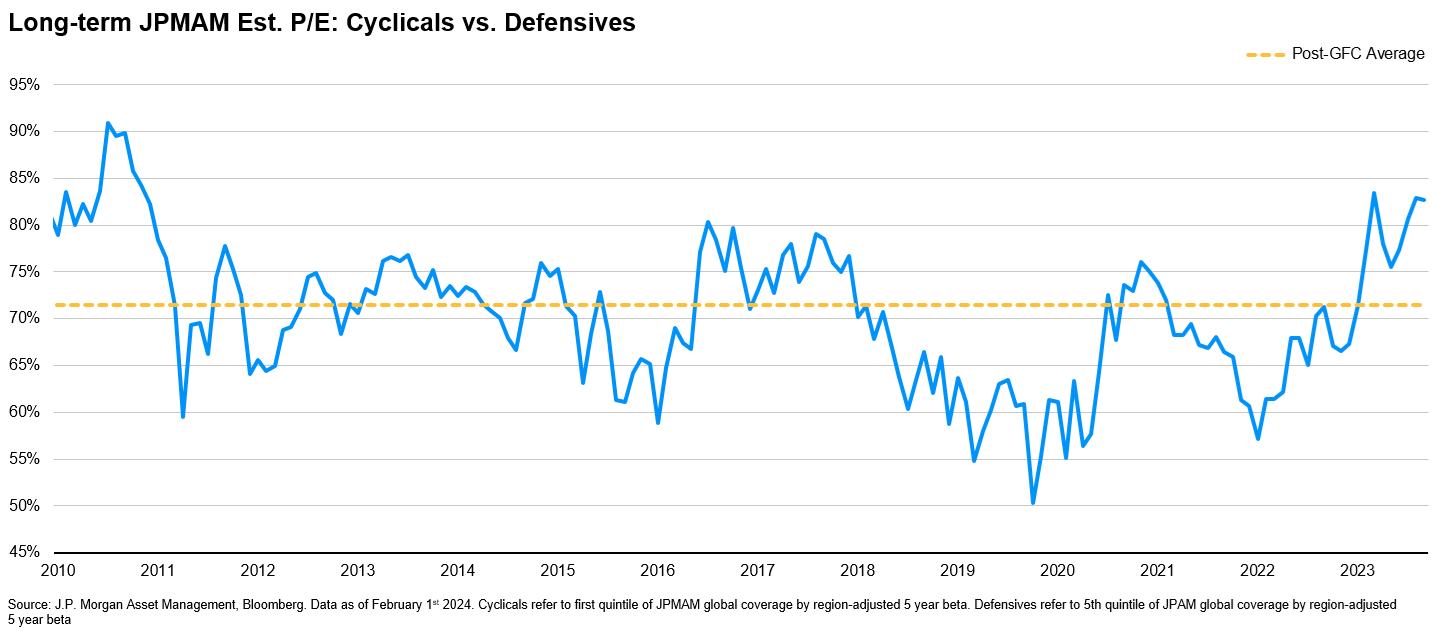

Portfolio manager Sam Witherow thinks utilities and consumer staples offer the best value currently due to market uncertainty.

The disparity between the valuations of the cheapest and most expensive stocks is historically wide globally but especially so in the US.

Wide spreads are indicative of uncertainty, according to Sam Witherow, a portfolio manager in JPMorgan Asset Management's international equity group. The gap between cheap and expensive stocks has been wide since the pandemic but the pockets of cheapness have shifted, reflecting an evolution in the sources of uncertainty.

“The baton of controversy has been passed from one group of stocks to another,” Witherow said. “Rolling controversy has played through markets.”

At the start of the Covid-19 pandemic, valuations of the “work from home losers” such as restaurants and airlines, were “in the doldrums”, he explained. Then the baton passed to stocks that were “crimped by huge rises in energy prices”. Next, as interest rates rose, companies hit by the higher cost of borrowing were discounted.

Today, “historical defensives” are cheap, such as utilities and consumer staples. “They don’t have the jazzy artificial intelligence (AI) story,” he pointed out, describing them as “boring stocks”.

In the past, income investors flocked to these sectors for their dividends but now, with bonds and cash offering decent yields, their relative attractiveness has diminished.

As a result, consumer staples are “getting more and more attractive” given their cheap valuations. Coca-Cola is one of the £730m JPM Global Equity Income fund’s top 10- holdings.

Boring defensive stocks are attractively valued compared to cyclicals

“The market is getting its head around this transfer and tricky hand-off between price-led growth to volumes-led growth,” Witherow continued. In other words, companies that hiked up prices in the past couple of inflationary years are starting to lose market share as consumers find cheaper alternatives elsewhere, so they are having to become less aggressive with price hikes and promotions.

“There’s always a pocket of controversy somewhere that we’ll exploit,” he added. “Now the opportunity is in boring stocks.”

Utilities are the JPM Global Equity Income fund’s biggest active overweight, with a 7% allocation, representing an overweight relative to the MSCI AC World benchmark of four percentage points.

The fund owns four utility companies in the US, where electrification has been “turbocharged by data centre demand”. These companies are paying dividends of 4% and are trading on 15-16x earnings, which is a post-financial-crisis low point. “A 4% yield compounding at 7% is a really nice total return from a regulated asset,” he explained.

He also holds a couple of utilities in Europe, where the grid needs to be reorganised to be fit for purpose and to incorporate renewable energy.

Exploiting these revolving pockets of controversy has paid off for the JPM Global Equity Income fund, which is the third-best performer in the IA Global Equity Income sector over 10 years, fourth over five years and seventh over three years to 11 June 2024.

Performance of fund vs benchmark and sector over 10yrs

Source: FE Analytics

That being said, sector allocations are tilts, not large bets. Witherow and the fund’s co-managers Michael Rossi and Helge Skibeli (an FE fundinfo Alpha Manager) endeavour to keep sector and regional exposures broadly similar to benchmark, believing that their expertise lies in stock section, not macro calls.

The fund aims to deliver a yield that is 20-50% higher than the broader market, plus an income that is compounding faster and, finally, fewer dividend cuts than the broader market.

Witherow expects the portfolio to deliver 8% dividend growth per annum for the next five years, which is about 50 basis points higher than the MSCI AC World index benchmark.

JPM Global Equity Income is slightly underweight the US, where dividends in general are lower than the UK and Europe, but its underweight is much smaller than most global equity income funds, Witherow said.

He thinks the Magnificent Seven, which dominate most global benchmarks, warrant their valuation premiums because of their superior earnings growth. Now that several of them have started to pay dividends, they also fall within his remit.

Meta Platforms, Alphabet and Salesforce all initiated dividends this year and Witherow bought shares in Meta the day it announced its dividend. It is currently the fund’s fifth-largest holding.

Microsoft is the global equity income strategy’s largest holding and although it pays a modest yield, it has strong potential for dividend growth, he noted.

Witherow is concerned, however, that consensus expectations for corporate profitability are too lofty and too complacent. Margins have come down since 2022 but are not far off their all-time highs. Companies have multiple challenges to deal with including slowing inflation and slowing real growth but sticky wage inflation, he said, and these challenges are not fully priced in.

Ahead of the kick-off for the football Euros, Shard Capital has proposed a team of US stocks which, with allowance for a few subs and formation changes, could go all the way to qualify for the World Cup.

Football squads and equity portfolios both need attackers and defenders – high growth, high risk forwards who should score goals, combined with companies or players that hopefully offer some stability and prevent you conceding too many losses at the other end.

You might feel that the entire transfer market is quite inflated at the moment, so I would remind investors at all times to keep within the ‘Football Financial Fair Play’ regulations, which stipulate that you do not spend more than you earn and threaten your long-term survival.

The Goal Keeper: Solid and strong, nothing getting past this one

Chubb: Outstanding value at approximately half the market multiple, this insurance company offers stability, longevity and now has the backing of Warren Buffett and Berkshire Hathaway. The change in the world’s climate has arguably changed the dynamics for property/casualty insurance forever and whilst we will all pay more in premiums, companies such as Chubb should continue to benefit.

Defence: Playing four at the back

Consumer staples make good defenders, while fullbacks in the energy and retail sectors can get up the pitch when the economy is flowing forward.

Hershey: Shares in the 130-year-old iconic chocolate company have fallen 24% over the past year due to the impact of cocoa prices skyrocketing to an all-time high in April 2024. But from this point, I would bet that the commodity price goes down and as it does, Hershey’s earnings and stock will recover.

Kenvue: This company is a spin-out from healthcare giant Johnson & Johnson and now owns several consumer brands we all know and love, such as Listerine and Neutrogena. The shares have fallen in their first few months of trading ahead of the sale of J&J's remaining 9% holding but with this transaction now completed, from here we have good value for steady, predictable GDP-level growth.

Cheniere Energy: A leading player in liquified natural gas exports from the US, whose business and share price benefitted hugely from the disruption to energy prices in 2022 as a result of Russia’s invasion of Ukraine. Now, we have come full circle with a politically motivated pause on development announced by US president Joe Biden in January 2024 which has hurt the stock. Trading at under 8x last year’s earnings, any reversion to the mean or an election victory for Donald Trump should see it perform well over the next year or so.

Walmart: Whilst Amazon gets all the attention, the world’s largest retailer is quietly improving all the time, turning its stores into fulfilment centres so that its online business is outgrowing its major competitor – by 21% in the most recent report. A sleeping beneficiary of the deployment of artificial intelligence (AI) over time, this should be a core holding and is my team captain.

Midfielders: They can defend on valuation and join the attack with growth

Knife River: Smaller companies such as Knife River have dramatically lagged their larger brethren during this period of higher interest rates and tech obsession. Knife River is a construction materials and aggregates company, which is likely to see an uptick in its business as all this well-publicised reshoring and grid transformation money gets put to work. You do need to actually build all these data centres and the power plants to run them, before you can enjoy all this AI stuff!

Amgen: This biopharma giant is on a mere 15x price-to-earnings ratio, based on the growth expected from the existing portfolio. But it also has a product for the GLP-1 obesity and diabetes market in trial currently. Based on early results, Amgen has a reasonable shot of disrupting the two leaders (Eli Lilly and Novo Nordisk) with a product that works just as well but will be much cheaper and easier for patients to take, as it only needs a monthly injection rather than the current weekly treatment required by alternatives.

Covenant Logistics: A small niche player in transport, partly a play on a recovery in the truckload cycle, this company also operates in two specialty and less-commoditised businesses: it takes live chickens and pigs to market and transports weapons and systems for the military. You can imagine the specialist equipment required for the former and security clearance for the latter to see that this business is therefore more predictable and profitable.

Attackers: High risk, they are on the pitch to score goals

Seagate: The world leader in the commodity business of hard disk drives. Is that exciting? Yes, when there is a new product cycle starting and the market has yet to fully appreciate it. It is called heat assisted magnetic recording (HAMR) and I believe Seagate has a lead over their competition. If correct, it should gain share with its customers, who are all the giant cloud companies, as they start to deploy this new storage disk from next year.

Qualcomm: My own Harry Kane. Qualcomm has moved a lot this year already, despite losing business to China’s Huawei. Momentum should stay with Qualcomm, if you believe that an AI-related upgrade is coming to mobile phones. Its chips go into both Android and Apple, but while the iPhone maker would like to get rid of them it clearly cannot (because Qualcomm’s technology is superior to anything Apple has in-house) and now, for the first time, its Snapdragon semiconductor is going into the latest PCs announced by Microsoft.

Knight Swift Transportation: Overcapacity of trailers, under-supply of drivers and over-inventory at retail stores has led to a collapse in the earnings of the leading truckload carrier in the US. It has reached the point where pricing is at or below breakeven for many routes, so companies are just starting to say no to business. It is called a cycle and the time to buy is when it looks horrible but before the turn. I expect earnings to trough within six months and then triple off the bottom over the following year to 18 months. An interest rate cut will goose the stock, but usually by then you will be too late to buy.

Julian Wheeler, is a partner and US equity specialist at Shard Capital. The views expressed above should not be taken as investment advice.

The manager of Finsbury Growth & Income Trust reveals why he's intending to increase his stakes in Burberry, Sage, and Experian.

FE fundinfo Alpha Manager Nick Train has revealed his plan to increase his holdings in Burberry, Sage, and Experian.

In Finsbury Growth & Income Trust’s latest factsheet, Train stated these three FTSE 100 businesses are executing on their stated strategy, “albeit to greater or lesser success” in the short term.

“For each we believe successful implementation of the stated strategy should lead to higher future earnings and a higher [price-to-earnings] P/E rating for those earnings,” he said. “Accordingly, we intend to add to each when we judge appropriate.”

Burberry’s shares are down 27.2% since the beginning of the year. The luxury fashion house reported a 4% decline in revenue in the past year, bringing it to just under £3bn.

Although Train expects further revenue declines this year due to ongoing challenging market conditions, he highlighted that the company is now attractively valued.

Performance of share YTD vs index

Source: FE Analytics

He said: “We note that at today’s market capitalisation of £3.6bn, Burberry is valued on c1.25x historic revenues. This seems low for a business that has generated operating margins of over 16% per annum on average for the past decade and will definitely be too low if the current, relatively newly installed, CEO, CFO and head of design can restore excitement to the brand and grow revenues again.”

Sage also disappointed investors as the software company's growth expectations were slightly revised downward. However, this has not dampened Train's optimism about the company's prospects.

“As long-term holders we must avoid being backward looking, but have to note that the new medium-term forecasts for Sage, of its revenues growing at high single or low-double digits, would have appeared incredible five years ago, when the company was struggling to grow at all,” he said.

Performance of share YTD vs index

Source: FE Analytics

Moreover, Train explained that Sage should benefit from two “big opportunities”. One of these is the growth of its Intacct subsidiary in the US and other geographies, while the other is to capitalise on new artificial intelligence (AI) enhanced services to deliver substantial efficiency gains.

“There are few listed UK companies with a global strategic opportunity comparable to this and Sage’s current market capitalisation of c£10bn could be much higher, we expect, if it can execute on that opportunity,” Train said.

Earlier this year, Train shared a list of six FTSE 100 companies that he believes will benefit from the advancement of artificial intelligence. That list already included Sage.

Another company in this list was Experian, which Train is intending to top up as well. Unlike the two previous holdings, Experian has performed well recently, with its latest results prompting analyst upgrades for the company’s medium-term revenue growth and higher profit margins, which Train assesses as credible.

Performance of share YTD vs index

Source: FE Analytics

He said: “The lessons we have learned from watching successful digital and software businesses over the past decade is that growth rates and profitability can scale as such companies’ services become increasingly valuable to a growing customer base. Experian is one of a relatively small set of UK-listed companies that offer participation in such effects.

“Those lessons also suggest that the ostensibly “high” prospective P/E that Experian trades on, of c28x, is, in fact, not high at all and the shares offer good value.”

Finsbury Growth & Income achieved a total return of 1.6% in May, while its year-to-date performance stands at 0.1%, according to FE Analytics.

Performance of investment trust in May and YTD vs sector and benchmark

Source: FE Analytics

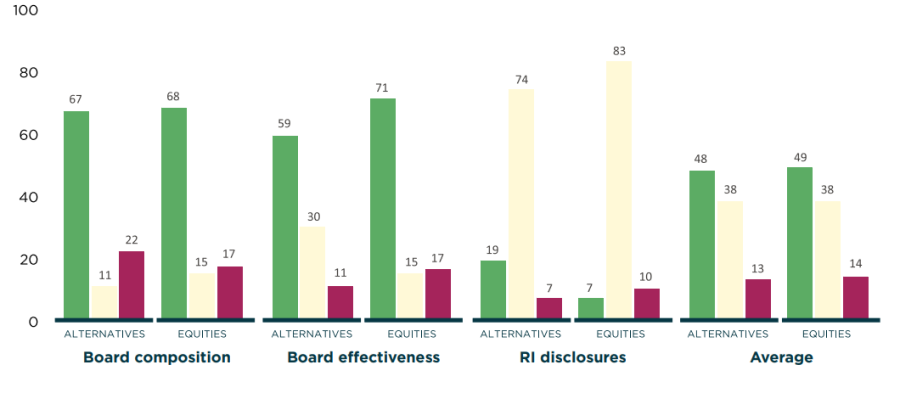

Quilter Cheviot’s engagement programme focusses on alternative investment trusts.

Less than half (48%) of alternative trust boards are well set-up and effective, according to wealth asset manager Quilter Cheviot.

Board composition and effectiveness are two of the three main factors used to assess alternative investment trusts within Quilter Chievot’s engagement programme.

The wealth management business gave a green, amber or red score to each investment trust in the private equity, infrastructure, multi-asset, macro and music royalties sectors, with less than one in two achieving a green light for both categories.

Board composition, which measures the degree of independence, diversity and skillset within the board, had both the highest percentage of green ratings (67%) and the largest proportion of red ratings, with nearly a quarter (22%) of trusts showing a lack of independence, manager representatives, poor oversight or little diversity.

The second factor is board effectiveness, or the ability and willingness to challenge the investment adviser and be open to shareholder feedback. Here, fewer than three in five (59%) trusts received a green rating.

This is an area in particular need for improvement, according to Quilter Cheviot’s head of investment fund research Nick Wood, with communication around gearing, discount management and performance fees atop the issues.

“We want to see trusts communicate clearly and effectively with us, especially around issues pertaining specifically to their structures,” he said.

“It isn’t the case that alternatives are opaque on these sorts of themes, but shareholder communication needs to improve to ensure investors understand exactly what it is they are buying in to and how they expect it to perform.”

The third factor was responsible investment disclosures, especially real-life examples of how the trust approaches stewardship and the integration of environmental, social and governance (ESG) factors within its investment process.

In this category, alternative trusts were found to be ahead of the wider market, with just 7% being given a red grade. However, only 19% of boards scored a green rating and the overwhelming majority (74%) were crossing the line on amber.

This is a result of the disconnect between responsible investment processes and the disclosure of such activities, said head of responsible investment at Quilter Cheviot, Gemma Woodward, who however noted that the direction of travel in this space is good.

“There is room for improvement when it comes to the corporate governance practices of alternative investment trusts. Investor expectations change over time with a fast pace of change, some can be left behind,” she said.

“Nevertheless, we have already seen some very positive improvements from some boards and we look forward to working closely with the 27 we have engaged with here to help them improve where possible.”

With all the three categories combined, only four investment trusts qualified for a triple-green rating.

The report on alternatives follows a first part that was carried out on the broader equity trust sector in September 2023.

The comparison of the two is illustrated with the chart below, which highlights some discrepancies in the factors assessed but a similar performance on average.

Comparison of alternatives versus equity trusts

Source: Quilter Cheviot

This Vontobel quality-growth manager highlights four stocks with powerful moats.

If you travel to some parts of the US, you’ll see massive construction projects going on in many cities such as Columbus, Ohio and Phoenix, Arizona. From a distance, they look like football stadiums but actually, they’re six times as big as that.

What you’re looking at are new chip plants being built with government support as part of the nearshoring trend set off to revolutionise supply chains and decrease dependence from China. Intel is currently building in Columbus and TSMC in Arizona, as Markus Hansen, portfolio manager at Vontobel’s quality growth boutique, explained.

Hansen is investing in a number of stocks that should benefit from the nearshoring trend and, in his opinion, will do well come rain or shine as they are losing the element of cyclicality they used to have. Below, he highlighted four stocks that fit this trend.

Vulcan Materials: With its cyclical side disappearing, the core quality business grows

We begin in the US, where Vulcan Materials makes crushed stone, or in technical terms, aggregate. Aggregate goes into two major things: roads and construction projects.

As such, the company is benefiting both from the nearshoring trend and from the “massive infrastructure programme” taking place in the United States.

Performance of stock over the past year

Source: Google Finance

“Instead of outsourcing chips production to Asia or manufacturing in cheap countries, the Inflation Reduction Act has encouraged American technology firms to bring those back to the US, which is why you see Intel and TSMC building these huge sites,” the manager said.

“But roads and infrastructure are also key – not just from and to the new plants but beyond. Infrastructure used to be pretty bad in the whole country and that's changing. This whole bulk of spending is going to be a 10 year process, which Vulcan will benefit from.”

Traditional roadbuilding has become a much more significant part of the business because roads have to be maintained every year, which is “a nice sustainable growth business over time”.

“The stock is going from what people used to perceive as a cyclical business to more of an actually predictable growth-type businesses,” Hansen said.

“The construction side is a cyclical business, but the company is reducing its exposure there. With the cyclical part disappearing, the core quality business grows.”

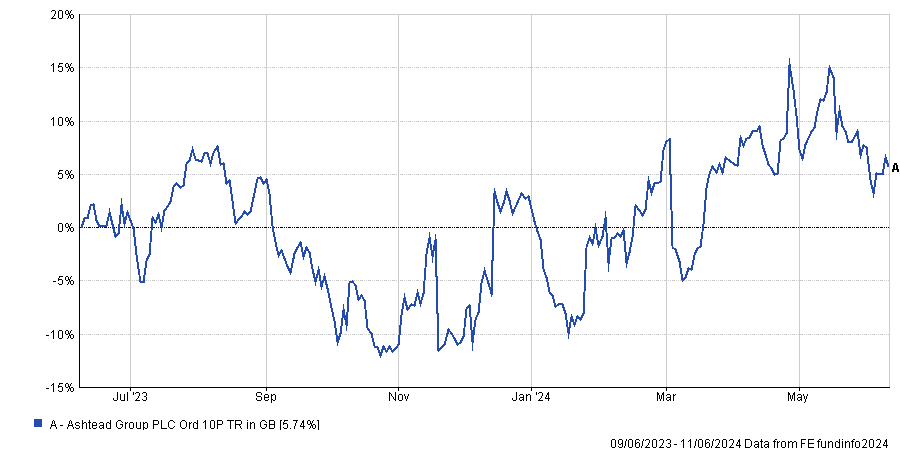

Ashtead: Its new app is changing a fragmented industry

Listed in the UK, Ashtead is an example of an industrial company whose business is mostly in the US – under the name Sunbelt – and will also benefit from the construction bonanza. It makes rental equipment for construction, maintenance and services.

Performance of stock over the past year

Source: FE Analytics

Generally, builders don't own their equipment but rent it, and that used to be a very fragmented industry. Sunbelt bought up these renters over time and created a franchise network. Today, they operate through an app, removing the need for subcontractors.

“Sunbelt has about a 15% market share and is looking to get that to north of 20%, because there’s still a big pie, which is still very fragmented to bring in,” Hansen said.

This part of the business has some cyclical elements to it, but the manager is excited about the developing services and maintenance side.

“The beauty of that is that, if the economy collapses tomorrow, offices will be empty but landlords are still required by law to maintain things like air conditioning, lighting, electrical and fire systems,” he said.

“So as that becomes a bigger portion of the business, we get more predictability in the earnings stream.”

Vinci: Its construction business is a fantastic cash cow

For an example of a European business, Hansel picked French concessions and construction company Vinci, which operates a toll road and an airport business, but the manager was more enthusiastic about its road construction activity, which he defined “a fantastic cash cow”.

Performance of stock over the past year

Source: Google Finance

“Once you build a road, you constantly have to maintain it, and generally, once a municipality has signed with a company, you have that contract for the rest of eternity,” he said.

ASML: Its order book is going to look pretty formidable

Remaining in Europe, for a much more recognisable name, the manager highlighted ASML, the leading manufacturer of machines that make silicon wafers.

As the only company that has the extreme ultraviolet lithography (EUV) technology, it was already the top player in the sector. But, according to Hansen, now it's an even better beneficiary.

Performance of stock over the past year

Source: Google Finance

Every chip manufacturer in the West has been told they cannot use Chinese technology in their chip plants, so now there's only one provider – ASML.

“The order book is going to look pretty formidable and it has very strong pricing power,” the manager said. “The stock has done well, so it's not that the market doesn't see this, but the predictability of the order book has improved dramatically and therefore it can carry a higher rating for longer now, because it’s just sitting in a great spot.”

The US Federal Reserve opted to hold interests steady yesterday.

Fund managers are divided on how many times they expect the US Federal Reserve to cut rates this year, following its decision yesterday to keep rates on hold.

Pictet Wealth Management expects two cuts in September and December while Nomura Asset Management thinks it is too early to rule out a summer cut and has put derivatives in place to profit from surprise cuts in July and September. Nikko Asset Management expects one cut this year, but Fidelity International is bracing itself for no cuts at all. This is all a far cry for the six cuts the market had priced in back in January.

Salman Ahmed, global head of macro and strategic asset allocation at Fidelity, said: “Our base case is zero cuts this year but if progress on inflation continues over the summer months or labour markets start to show some signs of stress, we do see the likelihood of one cut this year rising.

“That said, the US economy remains resilient and yesterday’s release was affected by vehicle insurance and airfare components, which means the bar for cutting to start remains high.”

The lack of consensus among asset managers and economists reflects divisions amongst the Federal Open Market Committee (FOMC) itself.

Eight officials have pencilled in two cuts this year, seven members expect one cut and four predicted none, although no-one is gunning for a hike. Chair Jay Powell has said one or two cuts are both plausible outcomes.

Xiao Cui, senior economist at Pictet Wealth Management, said the Fed has become extremely data dependent and that interest rate decisions will be driven by inflation and employment data. “The labour market is gradually balancing so the burden of proof lies on the inflation side,” she said.

Ahmed agreed: “We have seen the Fed completely abandon any kind of reliance on forecasting to set policy, so we continue to foresee the current data dependency in policy and markets to remain in place.”

What does this mean for bond markets?

Inflation remains stubbornly above target on both sides of the Atlantic, said Richard “Dickie” Hodges, manager of the $2.3bn Nomura Global Dynamic Bond fund, which “implies great caution on the part of central banks in moving to cut rates”.

“For now, as the market continues to guess when cuts will finally be delivered, bond yields will likely trade within a range (as they have for months now),” he said.

Hodges has invested in emerging market bonds, additional tier ones (AT1s) and convertible bonds, which will all “perform well when cuts are finally delivered” and “deliver positive yields in the meantime”.

Nomura also has call options in place on five-year US Treasuries. “The expiries are after the July and September Fed meetings, allowing us to capture some of the upside that would result from a (surprise) cut at that meeting. A form of insurance in case we are wrong,” Hodges explained.

The biggest risk facing bond markets is that the European Central Bank starts to walk back the two to three cuts that are priced in for this year, Hodges warned. “We therefore have credit hedges in place through credit default swap (CDS) index contracts, the notional size of which equates to 31% of the fund’s net asset value.”

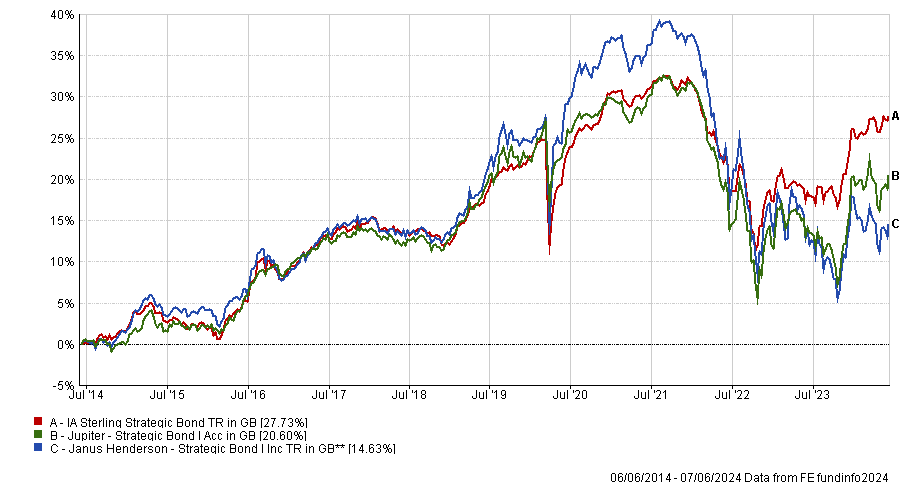

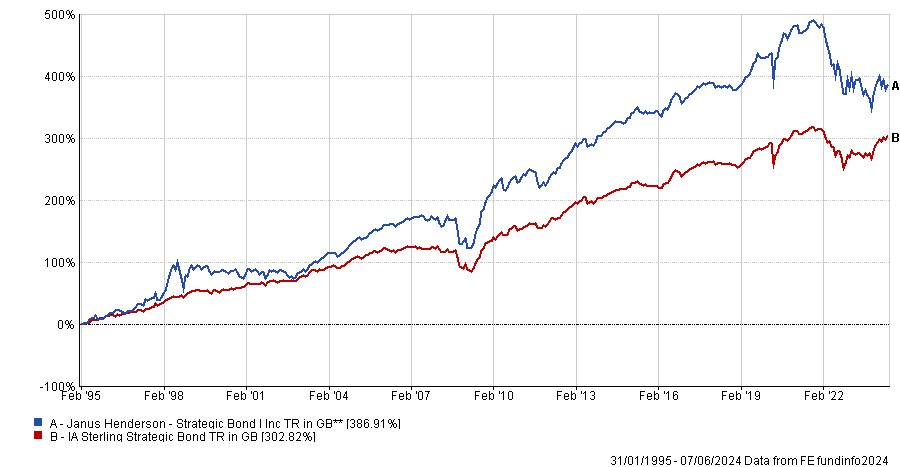

Experts compare the Janus Henderson Strategic Bond and Jupiter Strategic Bond funds and share their preferences.

Janus Henderson Strategic Bond and Jupiter Strategic Bond are the largest funds in the IA Sterling Strategic Bond sector, suggesting significant demand from investors.

Both funds are managed by experienced and respected teams. For instance, FE fundinfo Alpha Manager Ariel Bezalel has been at the helm of the Jupiter fund since 2008. Meanwhile, Janus Henderson Strategic Bond has been managed by John Pattullo since 1999 and Jenna Barnard since 2006, although Pattullo will retire in March 2025.

Paul Angell, head of investment research at AJ Bell, said the funds approach duration in a similar way.

“Both funds are genuinely dynamic in their duration positioning, which is surprisingly rare when compared to most funds in the IA Sterling Strategic Bond sector.

“An appetite for duration risk was particularly evident during the years of low interest rates through the tail-end of the 2010s, when the managers of both funds were willing to buck wider consensus and take sizeable duration positions as part of a 'lower for longer' interest rate trade,” he explained.

“The funds have been similarly positioned in their duration positioning in recent years with both now operating near a maximum long, given their managers' concerns with economic growth and expectations around falling inflation.”

Trustnet asked experts about the differences between the funds, their personal preferences, and whether they would suggest any other strategic bond funds besides those two.

How do they differ?

Eduardo Sánchez, associate research director of fixed income, alternatives and multi-asset at Square Mile Investment Consulting and Research, highlighted Jupiter’s barbell approach, combining high-quality credits with highyield bonds.

In comparison, Janus Henderson Strategic Bond has reduced its position in high-yield credits. While this is a sign of prudence, it has caused the fund to underperform compared to Jupiter.

Performance of funds over 3yrs

Source: FE Analytics

Angell said: “Janus Henderson typically invests in what it sees as lower beta, defensive credits in sectors such as telecoms, software and healthcare, whereas the Jupiter team typically has a broader and more active approach to allocating across sectors, depending on where the managers see the best opportunities through time.”

In addition, Jupiter Strategic Bond allocates to emerging market debt, while the Janus Henderson fund avoids this part of the market.

Janus Henderson Strategic Bond has two-thirds of its portfolio invested in AAA to A-rated bonds, which is more than twice the allocation of the Jupiter fund.

Which fund do experts prefer?

While considering both funds to be “solid” options, Sánchez prefers Janus Henderson Strategic Bond. He highlighted the experience of the portfolio managers and their top-down macro expertise.

Yet, he also warned that they can “get stuck to their views”.

“When these go against market moves, the strategy can experience sustained periods of underperformance given their willingness and patience to allow their thesis to play out,” Sánchez said.

Performance of fund since launch vs sector

Source: FE Analytics

Jason Hollands, managing director at Bestinvest, also opted for the Janus Henderson fund. He emphasised the depth of resources available to the managers, including the ability to leverage a team of 20 credit analysts based in London and Denver.

He added: “The key Janus Henderson strengths in my view are the flexible approach and strong risk management mindset, which has helped the fund perform well across different market conditions.”

Yet, Sam Benstead, fixed income lead at interactive investor, favours Jupiter Strategic Bond, stressing the strong absolute and risk-adjusted returns since inception.

Performance of fund since launch vs sector

Source: FE Analytics

He said: “Bezalel has been happy to own fewer UK government bonds to achieve this, and currently has debt from the US, Brazil, New Zealand and Australia in his top 10. Around a quarter of his fund is in sterling-denominated bonds compared with 37% for Janus Henderson.

“Both funds have a similar duration and amount invested in government bonds, but Jupiter has a higher yield because it owns more lower-rated bonds. Janus Henderson has 90% in investment-grade bonds and Jupiter has only around 40%.

“Investors looking for higher yields are better served by Jupiter, but the downside is that the bonds could perform worse if there is a recession and doubts over the credit worthiness of companies.”

Are there better alternatives?

While Janus Henderson Strategic Bond and Jupiter Strategic Bond are the largest funds in the IA Sterling Strategic Bond sector, it is worth noting that they have both lagged behind their peer group over the past 10 years.

As a result, investors may prefer to bet on a strategic bond fund with a lower profile but a more appealing recent track record.

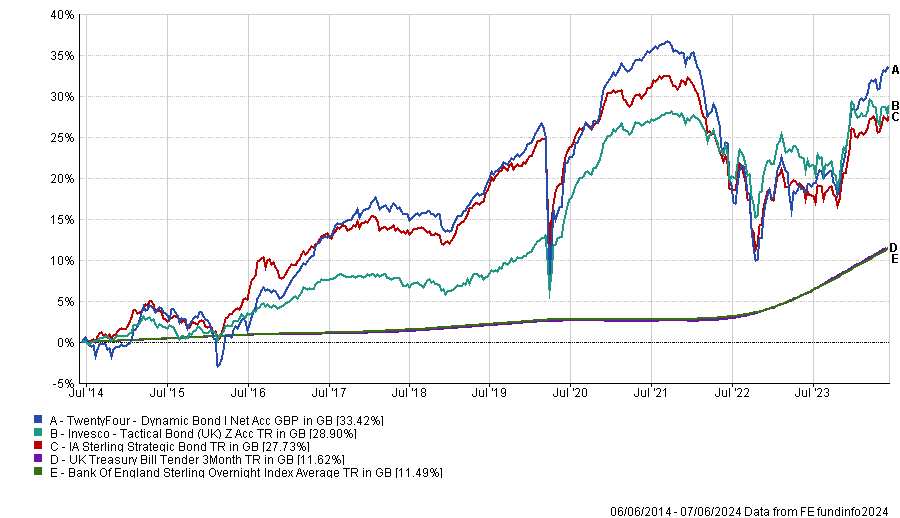

Both Hollands and Angell pointed to TwentyFour Dynamic Bond and Invesco Tactical Bond, which are both best ideas funds with flexible mandates.

Performance of funds over 10yrs vs sector and benchmarks

Source: FE Analytics

Angell said: “The managers of the TwentyFour fund have made the most of its dynamic asset allocation, as well as its holdings in high-yielding collateralized loan obligations, whilst the Invesco fund positioned well into the rising interest rate environment.”

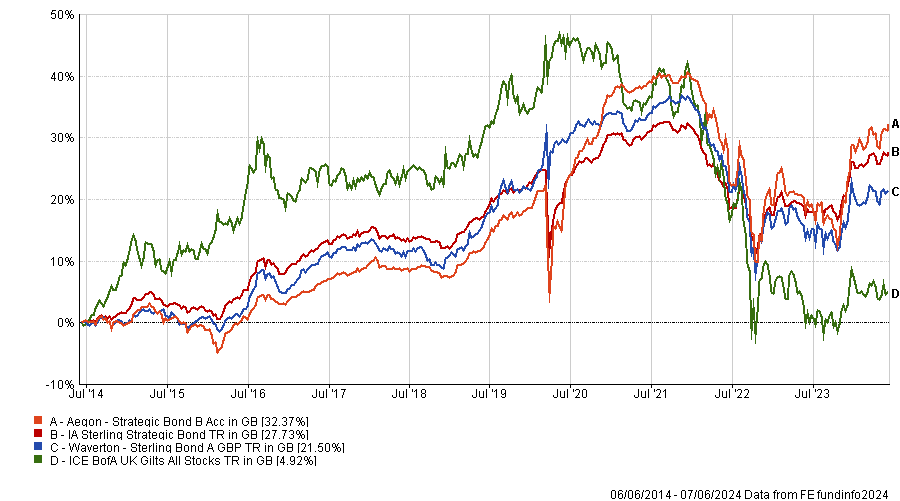

As for Sánchez, Waverton Sterling Bond and Aegon Strategic Bond are his preferred choices alongside Janus Henderson Strategic Bond.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

The Waverton fund, managed by James Carter and Jeff Keen, aims to offer investors a blend of income and capital growth with low correlation to equities and high-yield debt.

Sánchez said: “We believe this to be an attractive feature making the fund a core fixed income offering, providing diversification benefits in risk off periods.

“However, the fund is also flexible enough to manage credit exposure actively, including high yield credit and emerging markets debt, to deliver income.

“In addition, we like the managers’ high conviction approach which emphasises a high-quality portfolio, with a minimum 80% exposure to investment grade rated bonds and a self-imposed minimum interest rate risk exposure of at least five years.”

The Aegon Strategic Bond fund is an active, unconstrained strategic bond strategy consisting of a dynamic blend of global fixed income instruments, constructed to maximise risk-adjusted total returns through the market cycle. It is co-managed by Colin Finlayson and Alexander Pelteshki.

Sánchez added: “The process relies on six areas of alpha generation: asset allocation, credit risk, duration, yield curve, stock selection and sector selection. The managers blend top-down views with bottom-up security selection, with alpha coming from the different factors in different ways depending on the market environment, seeking to exploit long term and short-term market opportunities and inefficiencies.

“This combines to make the fund a compelling option for investors seeking a blend of income and capital growth through a dynamically managed portfolio of fixed income assets.”

Chinese equities have lost more than a third of their value during the past three years but funds managed by Matthews Asia, Federated Hermes and Fidelity have been overweight China for much of that time.

The Chinese equity market has been on a downward trajectory since early 2021 and despite short rallies in late 2022 and early 2023, and again this year, overall, the country has been mired in a savage three-year bear market. Consequently, the relative performance of Asian and emerging market equity funds has hinged upon their exposure to China.

Some funds such as Jupiter Asian Income have pulled out of China altogether while other managers have been ramping up their allocations as the stock market has gotten cheaper and cheaper. Managers at Matthews Asia, Federated Hermes and Fidelity International fall into the latter camp.

China vs Asian and global equities over 3yrs

Source: FE Analytics

Matthews Asia has been overweight China for three years in its Emerging Markets Sustainable Future and Emerging Markets Small Companies strategies. Portfolio manager Vivek Tanneeru said that after the sell-off in 2021, some Chinese companies became available at “very attractive multiples”, which is why he went overweight through stock selection.

The $3bn Federated Hermes Asia ex-Japan fund has stuck with China for even longer. Deputy manager Sandy Pei said the strategy has been overweight China and Hong Kong for as long as she can remember – apart from a brief period at the end of 2020 and in the first quarter of 2021 when the fund was underweight. The current allocation of 17% is close to the fund’s 20% cap on single country exposure.

The small-cap focused Fidelity Asian Values trust has an even higher allocation, with 31% in China and an additional 9% in Hong Kong-listed stocks as of 30 April 2024, the most it has ever allocated to those markets.

All three managers are overweight due to stock-specific opportunities. Pei said that “after a three-year bear market, everything is cheap in China”. Valuations are attractive across the board, encompassing both high quality and low quality stocks.

“We’re willing to pay £100,000 for a Ferrari but we’re equally happy to pay £5,000 for a Ford, so long as we’re getting a bargain,” she explained. “In China today there are lots of £100,000 Ferraris and £5,000 Fords.”

For instance, Tencent is the highest quality company in China and is trading on a valuation of 14-15x earnings, she said, as well as paying dividends and buying back its shares.

Pei also pointed to solid fundamentals. Last year Chinese companies achieved earnings per share growth of 15% yet the stock market de-rated due to negative sentiment. This year, she expects earnings to continue growing and hopes the stock market will not suffer any further de-rating. Many companies have strong balance sheets and cash flows, she said, and dividend yields provide downside protection.

Pei acknowledged that trade sanctions are an issue for some companies but said the market is broad, diversified and cheap, so fund managers can cherry pick companies with good risk/reward characteristics in areas where they wish to take on exposure.

Tanneeru agreed. He is “staying out of areas where there is obvious friction between the US and China”, but “embracing opportunities that come about because of these trade frictions”, such as China’s efforts to develop a localised supply chain.

He thinks that small and mid-sized companies focusing on mainstream technologies such as semiconductors will not be a focus for sanctions (which he expects to target large companies with cutting-edge technologies) and will have ample opportunities to grow their revenues.

Tanneeru views sustainability as an alpha generator in Asia and said China is at the front and centre of addressing climate change. The country has an 80-90% market share in the solar power supply chain and half of the world’s wind power capacity.

In electric vehicles, Chinese companies have taken over from Tesla to dominate the market, he said, and the world’s largest battery company resides in the country. China also has a colossal network of high speed trains which have been reducing emissions.

Asia is a world-leader in innovation and intellectual property, he continued, accounting for about two-thirds of global patent filings for the past few years. And in healthcare, “Chinese companies are among the world leaders in cutting-edge innovative cancer therapies”.

He also believes there is “discovery alpha” in finding Asian small and medium-sized companies, given 47% of the stocks in his target universe are not covered by sell-side research.

Tanneeru, who manages Matthews Asia’s Emerging Markets Sustainable Future, Emerging Markets Small Companies, Emerging Markets Discovery, Asia Small Companies and Asia Sustainable Future strategies, said his funds outperformed in 2020, 2021 and 2022 through diversified exposure to companies in different industries and factors.

The past year or so has been more of a struggle, when some stock selection decisions underperformed and China suffered a particularly sharp sell-off at the end of last year. “China accounted for well over 100% of the underperformance drag,” he said, given that performance was positive in other countries.

Going forward, China offers attractive growth compounding opportunities and attractive valuations, Tanneeru said, although he expects China’s recovery to be gradual.

Investors need to consider looking beyond public markets to help build diversified and therefore resilient portfolios.

The traditional investment portfolio, epitomised by the 60:40 split between stocks and bonds, has long been considered a safe and reliable strategy for balancing growth and risk. Either times were good and stock prices went up, or the economy faced troubles and investors flocked to the safety of bonds, pushing up their prices.

However, as 2022 showed, stocks and bonds tend to move together in periods of high inflation, significantly reducing bonds’ ability to diversify your portfolio when faced with an inflation shock. And it’s likely we will see more inflation shocks over the next 10 to 15 years, driven by three key factors.

First, the era of globalisation that defined the past several decades appears to be fading. Rising trade barriers, tariffs, and protectionist policies are increasingly hindering the free flow of goods and services. At the same time, rhetoric around immigration has grown more heated and restrictive in many countries.

Second, labour shortages will become more pronounced as demographic shifts and changing workforce dynamics take hold. An aging population in many developed countries, coupled with a decline in birth rates, is reducing the labour pool.

Moreover, the lingering effects of the Covid-19 pandemic have accelerated shifts in employment preferences, further exacerbating labour scarcity.

Third, climate change is increasingly disrupting supply chains, reducing agricultural yields, and increasing the costs of raw materials.

This means investors will need to consider looking beyond public markets to help build diversified and therefore resilient portfolios. Here’s where alternatives come in.

Alternative investments are a broad category encompassing private equity and private credit, as well as hedge funds and ‘real assets’. Real assets which include real estate, infrastructure, transport, and timber, have historically demonstrated low correlations with traditional asset classes, offering investors broader diversification opportunities.

Real estate and infrastructure tend to be leased to occupiers or operators on long-term leases, with clauses that allow rental increases at certain time periods, either by a fixed amount, or in line with a price level.

These built-in escalation clauses allow cash flows to grow over time. This last quality is especially attractive in a world of more frequent bouts of unexpected inflation – inflation that would otherwise eat into investment returns.

The equity market is changing

In addition to the challenges posed by a changing macroeconomic environment, the investment landscape is also changing, with companies choosing to stay private for longer.

In 1999, the median age of a company at IPO was four years; by 2020 this had risen to 12 years. As a result, the number of publicly listed companies has been steadily declining.

Between 1997 and 2022, the number of US listed companies fell by more than 30%; in the UK it fell by almost 60%. If you only focus on traditional public markets, public equity now provides exposure to a dwindling proportion of the total equity universe.

The flipside to a dwindling public equity universe is a rapidly expanding private equity universe. In fact, private equity now comprises 85% of the total investable equity universe and provides investors with access to some of the fastest-growing companies that are simply not available through public markets.

By investing in private markets, investors can participate in the value creation process and potentially capture outsized returns.

Gaining access

Alternatives have traditionally been the preserve of institutional and high-net-worth investors alone, but regulation is playing a key role in changing that. The introduction of frameworks such as the European Long-Term Investment Fund (ELTIF) and the UK Long-Term Asset Fund (LTAF) aim to provide retail investors with access to long-term, illiquid assets while ensuring appropriate investor protections.

As these regulations evolve, they may further democratise access to alternative investments and expand the opportunities available to investors.

Of course, investors must approach these assets with a clear understanding of their unique risks and considerations, such as illiquidity and the importance of manager selection.

But given the combination of broader diversification, protection against inflation, and access to a wider opportunity set, these investments are no longer just alternative. They’re essential.

Aaron Hussein is a global markets strategist at JP Morgan Asset Management. The views expressed above should not be taken as investment advice.

Contrarian investors share their secrets.

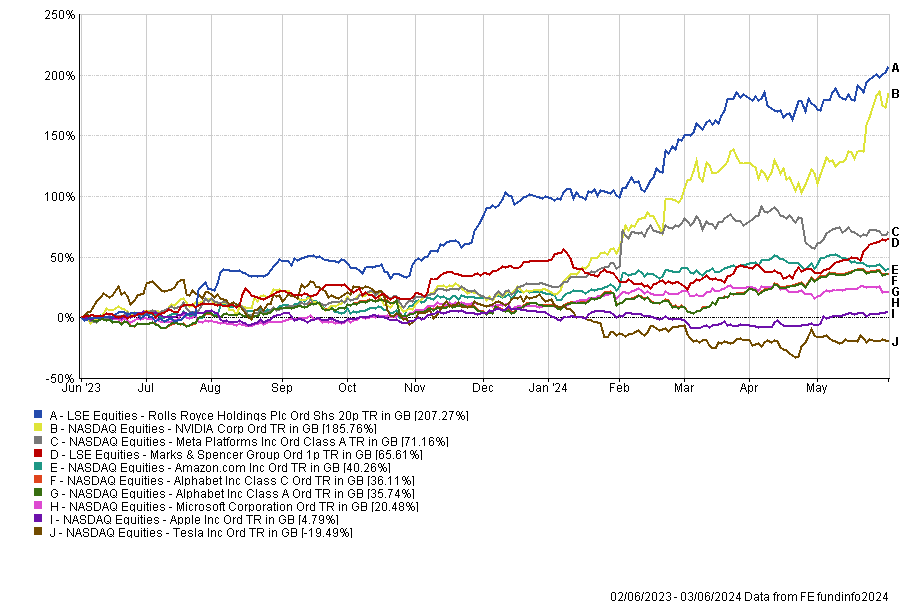

It is arguably more challenging for retail investors to spot mispriced opportunities. Unlike the most promising growth stocks, underappreciated companies rarely make the headlines, and when they do, it’s often for negative reasons.

Yet, they can be a cost-efficient way to make profits. For instance, buying shares in the then-unloved and therefore cheap Rolls Royce one year ago would have delivered better returns in sterling terms than investing in any of the expensive and well-known Magnificent Seven, including Nvidia.

Likewise, Marks & Spencer’s recovery has delivered returns exceeding those of most US artificial intelligence beneficiaries, and at a cheaper price.

Performance of stocks over 1yr (in sterling)

Source: FE Analytics

So how do professional contrarian investors identify these turnaround stories?

According to FE fundinfo Alpha Manager Alec Cutler, who runs Orbis Global Balanced and Orbis Global Cautious, there are plenty of signs in publicly available information that can suggest an opportunity.

These signs could include fearful headlines or headlines suggesting hope after a long period of dread, broker commentary that misunderstands the business, or commentary starting to connect the dots after a long period of not getting it, a falling share price, or a share price that stops declining even when the company reports tough conditions.

He said: “As a contrarian, you never really know what the catalyst is going to be. You try and find things that are cheap, where you can see a contrarian case. But you never really know what the thing will be that shifts the market’s view.”

An example Cutler gave is electricity infrastructure stocks. While he did not know what the catalyst would be at the time of purchase, they benefited from the artificial intelligence rally, as this technology requires a lot of electricity.

“You can pay up for Nvidia, or you can buy an electric utility of all things. It’s pretty cool to see that,” he said.

However, Dmitry Solomakhin, portfolio manager of Fidelity FAST Global, warned that contrarian investing is a time-consuming process with no “hard and fast rules”.

He structures his approach in three steps. The first is to find a business that is fundamentally of good quality but may have been mismanaged or gone through operational or financial issues. Then it is important to ensure the company acknowledges these issues and is willing to address them. Finally, the management and the board need to be capable of executing the necessary changes.

Rolls Royce, which remains his largest holding today, “was lacking cost and financial discipline, but it is now being fixed”, Solomakhin said. “There have been very significant improvements in cash flows and financial returns and it now in an even stronger competitive position today.”

Due to the nature of contrarian investing, Tom Matthews, co-manager of the JOHCM UK Dynamic fund, emphasised that this investment style requires both discipline and patience.

Discipline is needed when selecting which assets have the potential to be turned around. Moreover, investors must ensure they are paying the right price for the expected future cashflows, with an “acceptable margin of safety on top”.

As for patience, he believes investors should hold back until a new management team reveals a strategy focused on unlocking value and the benefits of the turnaround start to accrue to shareholders.

Matthews added: “At UK Dynamic, our holding period for stocks is often well over five years. Good things do come to those who wait!”

What financial ratios can investors use?

One of the first things James Henderson, portfolio manager of Henderson Opportunities and Lowland Investment Company, considers when looking for a mispriced opportunity is a company’s sales volumes.

“Firstly, it’s a good indicator of size – where market cap tends to fluctuate, sales volume provides us with a solid number to start from. It is particularly important for us because it gives us an indication of existing demand,” he explained.

“When a company is in trouble, it might not be making a proper margin on its sales, or it might even be making a loss, but the sales number tells us what scope there is for improvement of those margins once other issues have been addressed. This helps focus a company on the changes they need to make to return to proper profit margins.”

The main metric Henderson uses is the enterprise value-to-sales ratio, which indicates how much it would cost to buy a company in the context of its sales.

Debt is another factor that Henderson considers.

He said: “Often in these cases, debt is too high so we need to understand how it is going to be paid down. We then need to assess whether a company is going to invest in its own products to improve their offering sustainably. So, we look at the debt position when we make the initial investment, and we have to see a path from there to bring it down.”

To identify contrarian opportunities, Solomakhin relies on free cash flow, which is a measure of profitability representing the remaining cash after capital expenditures have been subtracted.

He said: “I look at the normalised free cash flow the business should be able to generate three to five years out if the turnaround is successful. If it offers over 15% free cash flow yield to enterprise value on these normalised numbers, it is quite attractive.”

Beware of value traps

Contrarian investing is not without risk as turnaround stories might never materialise.

Mark Landecker, portfolio manager of Nedgroup Contrarian Value Equity, explained: “Value traps occur when a company’s cashflows fail to inflect. There are two clear cases when this can occur.

“First, a company’s end-markets are too structurally challenged and its revenues and cashflows collapse faster than it is able to re-allocate capital to new, higher returning parts of the business.

“Second, a company’s starting debt position or transformational capital investment requirements are too high, meaning that cashflows never reach inflection point.

“Any combination of these can lead to the equity value of a company being significantly diluted as investors are required to inject further capital.”

Solomakhin added that misses are part and parcel of investing in contrarian opportunities.

“Given that I only look at challenged businesses with turnaround potential, any mistake that I make will almost certainly be a value trap. If I am good, then my single stock ‘hit rate’ will be around 54-55%, which means in 45-46% of cases I will be involved in value traps,” he pointed out.

An example of a stock that did not live up to his expectation is Tripadvisor. He explained that the company used to have a strong competitive moat due to the large user base and a database of consumer reviews. However, it then tried to compete directly against its own customers, such as Booking.com or Expedia, and failed. Moreover, the company’s competitive moat has weakened over time.

Almost a third of financial advisers now use a bespoke model portfolio service, a survey by FE fundinfo found.

An increasing number of financial advisers are working with discretionary fund managers (DFMs) to build bespoke model portfolio solutions (MPS) – as opposed to using off-the-shelf funds for their clients.

Just under a third (31%) of financial advisers responding to a survey from FE fundinfo said they had implemented a custom MPS in partnership with a discretionary fund manager. Another 13% of respondents expect to start using bespoke solutions in the next one to three years.

There remains a cohort of advisers who are unconvinced about the benefits of bespoke solutions, however. A fifth of respondents said they would not use a custom MPS while an additional 36% said they were unsure.

Tax changes, meanwhile, have prompted almost a fifth (19%) of advisers to implement a customised MPS. The capital gains tax allowance has been gradually reduced over the past few years and stands at £3,000 for the 2024-25 tax year.

Other than investment performance, advisers said their priorities when choosing an MPS were: integration with platforms and research tools (cited by 70% of respondents); clear, transparent and client-friendly reporting documents (61%); contact with the investment team (58%); and choice of term lengths and risk profiles (57%). A fifth of financial advisers said they wanted to have input into their DFM’s investment strategy.

Advisers ranked asset allocation as the most important factor for selecting a customised MPS. They also prized fund analysis, portfolio and governance, reporting and communication, portfolio design and analysis, and operational excellence and trade validation.

Ed Margot, head of client investment strategy at FE Investments, said: “The rules of investing and financial advice haven’t changed – empathy and communication are still highly prized. An MPS that can get the message across, can support the financial adviser, and deliver positive outcomes across term length and risk level, is a valued strategic partner.”

There is growing scepticism among financial advisers’ clients about the validity of sustainable investing. This year, 33% of advisers said their clients were unconvinced by environmental, social and governance (ESG) investing, compared to just 11% in FE fundinfo’s 2022 survey. This considerable shift could reflect concerns about greenwashing and/or disappointing investment performance.

Meanwhile, advisers were optimistic about the Financial Conduct Authority’s Consumer Duty, which was introduced on 31 July 2023, with 45% of respondents saying it would have a positive impact on advice provided to clients.

As a result of Consumer Duty, advisers are putting more emphasis on evidencing that clients’ needs and outcomes have been met and are spending more time on suitability assessments and client communication.

Although most (82%) of respondents said Consumer Duty has not changed what they look for in a centralised investment proposition or MPS – for the 18% of advisers where it has been an influence, they are now focusing more on value for money and fees.

FE fundinfo’s survey was conducted between November 2023 and February 2024 and was completed by more than 160 financial advisers.

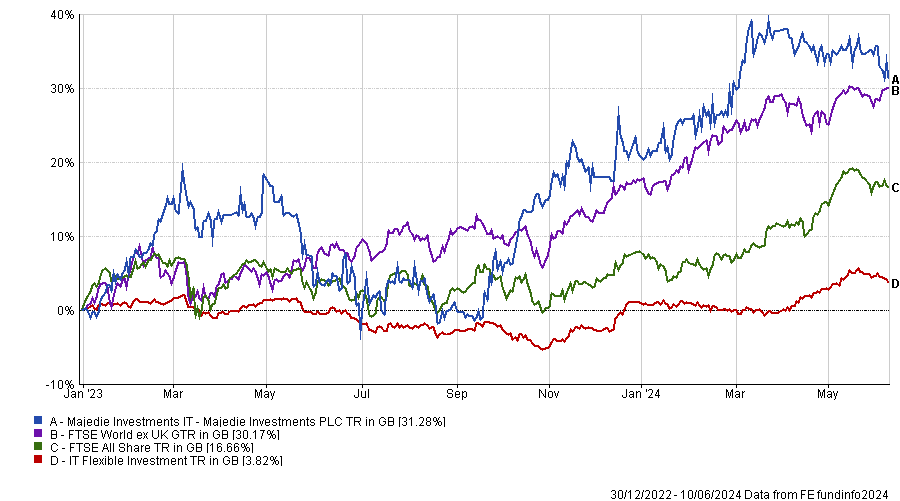

Majedie Investments has narrowed its discount from the high twenties in early 2023 to around 11% today.

A change of manager and renewed interest from shareholders have propelled Majedie Investments from a discount in the high twenties in 2022 to just 11% today.

Since the start of last year, the investment trust has made 31.3% on a total return basis, propelled by its discount narrowing, making it the top performer in the IT Flexible Sector.

The trust appointed Marylebone Partners as its investment manager in January 2023 and switched to a ‘liquid endowment’ investment strategy, with a return target of inflation plus 4%. The portfolio is split between external managers (56% of the trust), direct investments (24%), hard-to-access special investments (10%) and finally, bonds and cash (10%).

Performance of fund vs sector and indices since January 2023

Source: FE Analytics

Majedie recently announced its results for the six months to 31 March 2024, during which time its discount narrowed from 18.7% to 7.6%, although it has widened since then. The trust achieved a net asset value total return of 13.3% and a shareholder total return of 28.1% during the six-month period. Its total assets rose to £165m.

Given the discount has already come in substantially, Trustnet asked experts whether investors have missed the boat or if the trust still represents good value, and if there are any other similar multi-asset trusts that investors should consider instead.

Juliet Schooling Latter, research director at FundCalibre, said Majedie is now trading “at the slightly more expensive end relative to its long-term history” but for investors with a long time horizon, it is “likely to still represent a strong opportunity”. She also believes there are catalysts for the discount to continue narrowing.

“The whole investment trust sector has been considerably affected by worsening financial conditions and technical issues over the past few years, resulting in an almost synchronous widening of discounts. If factors that helped cause this decline, such as higher rates, inflation and less investor confidence, were to improve, and assuming the trust's underlying holdings continued to perform, there is no reason there might not still be a healthy upside for investors,” she said.

“Should wider financial conditions improve, coupled with the implementation of a promising new strategy, we believe there is still plenty to play for at Majedie.”

William Heathcoat Amory, managing partner at Kepler Partners, concurred. “We think the first year of the manager’s tenure represents a solid foundation for showcasing the potential of a liquid endowment-style model. If the managers deliver in line with their objectives, there’s scope for the current 11.4% discount to narrow further.”

Heathcoat Amory views Majedie as a “return-seeking diversifier” because it is correlated to stock markets, but aims to have lower volatility than equities. “Majedie has the potential to provide exposure to genuinely differentiated sources of returns,” he said.

Another differentiating factor is its fee arrangements. Marylebone Partners receives a flat fee based on the trust’s market capitalisation, not its net asset value, so it’s interests are aligned with shareholders.

James Carthew, head of investment companies at QuotedData, was less enthusiastic. “Majedie was struggling a bit before Marylebone Partners was appointed. It had created a great deal of value by establishing Majedie Asset Management (MAM), but its sale to Liontrust Asset Management did not end well (it exchanged its stake in MAM for Liontrust shares that then fell in value) and the funds that it was invested in were underperforming their benchmarks,” he recalled.

When asked to suggest alternatives, Carthew and Schooling Latter both pointed to RIT Capital Partners, which invests third-party funds and direct equities like Majedie, and has some private market holdings to boot.

Carthew said: “RIT Capital is trading on a discount of 27.2%, which reflects some investors’ (irrational in my view) dislike of its private equity holdings. RIT is committed to reducing the exposure to this part of the portfolio and is keen to narrow its discount.

“As a trade, to me RIT Capital might be a better bet. Majedie has had a good run over 2024, but RIT could catch up as it achieves some disposals from its private equity portfolio at premiums to carrying value (past disposals have followed this pattern).”

Schooling Latter pointed out, however, that “RIT’s performance has been less impressive with the trust on one of its widest discounts in its history. Poor sentiment and share price weakness have arguably gone too far, and it does certainly look cheap.”

Meanwhile, Majedie’s chairman Christopher Getley was bullish about the trust’s ability to continue its strong run, noting the “breadth of ideas” that have contributed to recent outperformance.

“Returns have been generated from positions in areas as varied as biotech, software, Chinese and copper stocks, as well as credit opportunities,” he said.

External managers made the biggest contribution to performance in the six months to 31 March, returning 9.1%, led by the Helikon Long/Short Equity fund. Other external managers include biotech specialist Paradigm BioCapital, Praesidium Strategic Software Opportunities, deep value manager CastleKnight, and several managers with expertise in stressed or distressed credit, including the Millstreet Credit fund.

Dan Higgins, chief investment officer of Marylebone Partners, described the trust’s investment philosophy as long-term fundamental investing, taking advantage of market inefficiencies and embracing alternative return sources.

“I don’t think I’ve ever used the word ‘differentiated’ as much as in the past 18 months,” he admitted. The trust “frankly only has the right to exist if it is offering something truly differentiated that shareholders can’t get elsewhere.”

The slowdown isn’t evidence enough for the Bank of England to start cutting rates, experts say.

Monthly real GDP is estimated to have shown no growth in April, the Office for National Statics (ONS) has announced today.

Following a stunted 0.4% uptick in March, experts are now blaming the weather for the disappointing figure of last month.

Lindsay James, investment strategist at Quilter Investors, said: “Persistent rain has kept consumers from spending and caused economic growth to grind to a halt, with sectors such as retail, construction and pubs all severely impacted”.

AJ Bell head of financial analysis Danni Hewson also wasn’t surprised by the reading, as ‘rain stopped play’ for builders, who shunned roof tops, as well as for shoppers, who deserted high streets in favour of their warm, dry sofas.

The figure hides a weak outcome for manufacturing, construction and industrial production, which worries Hewson. Output has fallen for three consecutive months, with “little surprise” that so much focus has been placed on housebuilding by political parties, all hoping their policies can deliver a sustained growth spurt for the UK.

There also was a stronger-than-expected services sector, however, which was possibly driven by ongoing wage growth, according to Neil Birrell, chief investment officer at Premier Miton.

But this slowdown won’t be moving the needle at the next meeting of the Monetary Policy Committee on 20 June.

“No one set of numbers will drive the Bank of England’s interest rate decision, but policymakers will now be looking to inject some stimulus as soon as they feel it is safe to do so," he said.

James echoed this, noting: “Wage inflation remains elevated and consumer price inflation is expected to tick higher in the coming months, and thus the Bank of England won’t want to deviate from its strategy just yet.”

On a positive note, the weather has improved of late, likely boosting May’s reading, according to James. Hewson also registered “a frisson of excitement in the air” that big events such as the UEFA Euro Cup and Taylor Swift’s Eras tour will help deliver “a decent boost” to the economic picture by the time we get the half-year result.

Although Seraphim Space reached the moon in 2024, experts recommend that investors stay grounded.