Trustnet finds out which funds posted the highest returns last month… and which faced the biggest losses.

October was gold funds’ time to shine after a new record high for the yellow metal caused them to surge up the performance tables, FE fundinfo data shows.

Ben Yearsley, director at Fairview Investing, described October as “another fascinating month”, with the UK Budget causing volatility in the gilt market, banks like HSBC and Standard Chartered reporting strong earnings, and mixed results from the US tech sector putting their “sky high valuations” under the spotlight.

“Looking at indices, it was a pretty drab affair last month. It was all a bit turgid with the only bright spot being Japan where the Topix gained 2.19% despite an inconclusive general election result with the ruling LDP under new prime minister Ishiba recording the second worst result in their history,” he said.

“The FTSE, in anticipation of this week’s Budget, fell 1.45% placing it mid table. After the Chinese supercharged September, it was no wonder October was a bit flat – Beijing can’t keep up the stimulus the market demands.”

Source: FinXL

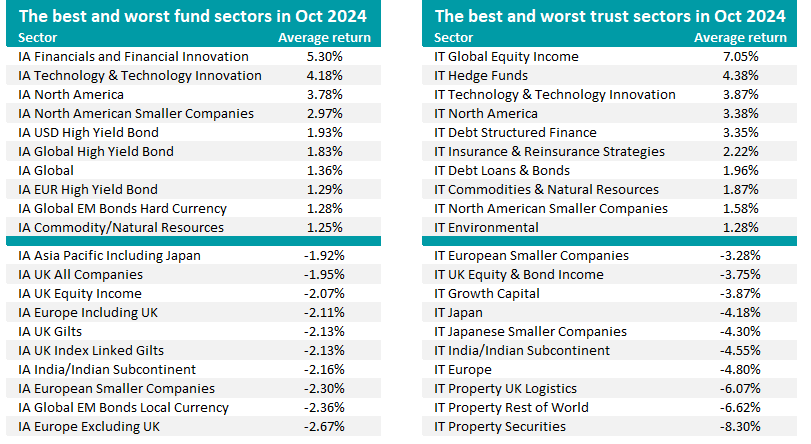

When it comes to the best and worst fund sectors of the month, the IA Financials and Financial Innovation peer group led the Investment Association universe with an average return of 5.3%. This was in part due to those strong earnings from banks during October.

IA Financials and Financial Innovation is the strongest Investment Association sector over 2024 so far thanks to an average return of 17.3%.

The IA Technology & Technology Innovation came in second place during October, followed by three peer groups focused on US assets (IA North America, IA North American Smaller Companies, IA USD High Yield Bond).

Yearsley put this down to “a strong dollar and weak pound boosting returns” in US-focused funds. “Currency was an important factor in returns last month with the US dollar performing strongly after a weak few months,” he added.

The IA Europe Excluding UK sector comes at the bottom of October’s leaderboard, as its average member made a 2.7% loss, while IA European Smaller Companies was the third worst. Europe has struggled of late, with the German economy flirting with recession and companies such as VW closing factories.

IA UK Gilts and IA UK Index Linked Gilts were also among the worst sectors after the gilt market was hit with volatility around the Autumn Budget, which saw chancellor Rachel Reeves hike taxes by £40bn while promising higher government spending.

In the investment trust universe, IT Global Equity Income led the month with an average return of 7.1% driven by the stronger dollar. Like in the open-ended peer groups, strategies investing in tech and US stocks also performed strongly.

Property, Europe and Indian trusts were among the worst performers.

Source: FinXL

Turning to individual funds, WisdomTree Blockchain UCITS ETF made October’s highest returns with a gain of 15.6%. Similarly, Invesco CoinShares Global Blockchain UCITS ETF was up 11.8%.

The outperformance of these ETFs is linked to the strong gains made by cryptocurrencies last month, with bitcoin passing $71,000 and nearing a new record high.

However, the big story among funds for Yearsley was gold and other precious metals, which have been rallying in recent months. Gold started October at $2,654 an ounce but passed the $2,800 mark; it fell back slightly to end the month at $2,749.

“Gold funds were the pretty clear winner in October – unsurprising with gold hitting another new all time high. Silver has joined in the rally too meaning it was gold and precious metals that delivered. Four of the top 10 funds were gold and precious metals with more in the top 20,” he noted.

“Gold has been a clear winner in 2024 with falling interest rates and geopolitics a clear driver. Gold equities had felt like they were lagging the actual price of physical gold, but it does seem as if equities are coming to the party now.”

Jupiter Gold And Silver, WS Charteris Gold & Precious Metals, HAN AuAg ESG Gold Mining UCITS ETF, SVS Baker Steel Gold & Precious Metals, WS Ruffer Gold and BlackRock Gold & General are among the month’s best funds.

The strong performance of financials is reflected by the presence of Guinness Global Money Managers and Jupiter Global Financial Innovation in the top 20 while WisdomTree Cloud Computing UCITS ETF and Dow Jones Internet UCITS ETF show investors’ continued interest in tech stocks despite high valuations.

Among investment trusts, Tetragon Financial was the best performer in October with a 35.5% total return. The trust focuses on alternative assets, investing in opportunities such as private equity stakes in asset management companies, venture capital and hedge funds.

British & American was up 23.9% while Atrato Onsite Energy gained 18.6% after a takeover bid was announced.

Source: FinXL

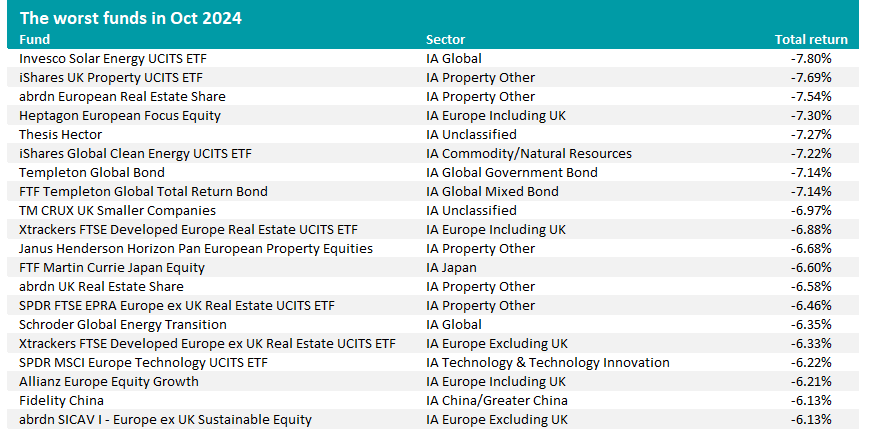

A couple of themes are also apparent among the worst performing funds of October.

Invesco Solar Energy UCITS ETF has hit with the heaviest loss, falling 7.8% over the course of the month. Other funds investing in similar stocks can be seen in the list of last month’s worst performers, including iShares Global Clean Energy UCITS ETF and Schroder Global Energy Transition.

There are also plenty of property funds among the month’s worst performers, such as iShares UK Property UCITS ETF, abrdn European Real Estate Share, Xtrackers FTSE Developed Europe Real Estate UCITS ETF, Janus Henderson Horizon Pan European Property Equities and abrdn UK Real Estate Share.

Pension funds are no longer a tool for passing wealth to the next generation.

Nothing is certain except death and taxes, and now the Budget has “put up death taxes too”, according to Charlene Young, pensions and savings expert at AJ Bell.

Unspent pension funds will form part of people’s estate from April 2027 onwards, ending pension funds’ previous immunity to inheritance tax (IHT).

This change has the potential to transform how people invest and manage their pension funds, as well as how they pass on money to the next generation.

Alex Cummings, a wealth planner at Succession Wealth, said his clients had been “using alternative assets to fund retirement spending, with pensions being used for passing on wealth”, but that approach “could be turned on its head”.

“I can see trust-based whole-of-life and gifting strategies becoming a bigger focus going forward,” he added.

His colleague Hayley Burns, also a wealth planner, advised people to discuss succession planning with their families and to consider gifting money earlier.

“From a long-term care planning perspective, it may become more attractive to purchase long-term care annuities to remove funds from the estate”, she continued, “especially if that would mean keeping the estate within allowances”.

Everyone can pass on £325,000 before IHT is due but this amount has been static since 2009 and the chancellor has extended the freeze until 2030. The allowance is therefore shrinking in real terms (once inflation has been taken into account).

If any part of the £325,000 threshold is not used, the remaining allowance can be passed on to a surviving spouse or civil partner, potentially amounting to a £650,000 allowance per couple.

What’s more, unused pensions can still be transferred to a spouse or civil partner without incurring IHT, but pension money will be taxed if given to anyone else.

In light of this, Chris Flower, chartered financial planner at Quilter Financial Advisers, said “it is imperative to review and, if necessary, update any existing expressions of wishes to ensure your pension goes to the correct beneficiary”.

There are many other ways to save for the next generation other than pensions, said James Norton, head of retirement and investments at Vanguard Europe. He suggested using junior ISAs to invest up to £9,000 tax-free on behalf of a child under 18.

AIM-listed stocks were previously exempt from IHT and, for some people, were an integral part of intergenerational wealth planning, but that has changed too.

AIM stocks now have a 50% reprieve from IHT, which is better than the full removal many experts had feared, but this still means that AIM stocks will be subjected to a new 20% IHT levy.

Anthony Cross, head of Liontrust’s economic advantage team, encouraged investors to look at AIM on its own merits. “There remains a huge valuation opportunity and upside in investing in AIM – these companies are not valuable because of their tax treatment but because of their underlying fundamentals,” he said.

"With interest rates reducing, growth returning, a stable government and [the tax] question now resolved, we believe the headwinds that have been plaguing AIM have now turned into tailwinds.”

Oliver Bedford, fund manager at Hargreave Hale AIM VCT, was encouraged by the continuation of tax benefits for venture capital trusts (VCTs) and enterprise investment schemes (EIS).

“Whilst the past few months have been very difficult for AIM – and by extension, AIM VCTs – confirmation that the government remains committed to the VCT and EIS schemes through to 2035 and news that AIM investors can still benefit from business property relief, albeit at a lower level, demonstrates the government’s continued support for two important constituents of the AIM investor community,” he said.

The ‘bed, spouse and ISA’ manoeuvre could save couples thousands of pounds in taxes.

What impact will this week’s Budget have on your finances?

The answer – joked Douglas Scott, investment manager at Aegon Asset Management – depends on whether you are a “chain-smoking private equity fund manager who will be flying to their soon-to-be-purchased third home by private jet to catch up with the four kids on a break from boarding school”.

Yet many people with far less lavish lifestyles could be liable for a much larger tax bill.

Capital gains tax (CGT) was hiked in Wednesday’s Budget from 10% to 18% for basic rate taxpayers and from 20% to 24% for those on a higher rate. This follows the previous government’s decision to reduce the annual CGT allowance from £12,300 to £3,000.

However, investors have a few tricks up their sleeve to guard against the chancellor’s tax grab.

First and foremost, they should be making full use pension funds and ISAs to invest in equities and other asset classes tax free.

Second, a manoeuvre called ‘Bed and ISA’ or ‘Bed and SIPP’ involves selling assets that are outside of a tax wrapper and rebuying them within an ISA or self-invested personal pension (SIPP) so that any future gains are tax free.

Selling the assets could potentially incur a CGT liability now, said Laith Khalaf, head of investment analysis at AJ Bell, but “investors can mitigate this by judicious use of their annual £3,000 CGT allowance”.

“Investors who feel they might breach the £3,000 annual CGT allowance using this approach might consider pairing the sale of a profitable investment with a loss-making one. Losses can be used to offset gains, thereby reducing the capital gains tax liability, then either or both investments can be rebought within the ISA to avoid tax on future gains,” he explained.

People in a committed relationship who are happy to plan their finances jointly have even more tools at their disposal to avoid the ravages of higher taxes.

A couple has recourse to both partners’ annual £3,000 CGT allowance on profitable share sales.

“By doing a ‘Bed and Spouse and ISA’, it’s also possible to use two sets of the annual ISA allowance of £20,000 to shelter those assets from future capital gains,” Khalaf noted.

Furthermore, transferring assets to a spouse or civil partner can be done free of CGT and is especially useful if one person is a higher rate taxpayer and the other is not. Even when capital gains exceed the annual CGT allowance of £3,000, it is better to pay 18% than 24% tax.

Another option for wealthy, adventurous investors who have filled their pension and ISA allowances would be to invest in early stage, fast-growing businesses through venture capital trusts (VCTs) and enterprise investment schemes (EIS).

“Capital gains on investments held within both VCTs and EIS are free from tax and in addition, an EIS investment provides the opportunity to defer capital gains made elsewhere, whereas a seed enterprise investment scheme (SEIS) investment comes with a 50% exemption on gains made elsewhere,” Khalaf explained.

Nonetheless, “investors should ensure they don’t let the tax tail wag the investment dog”, he warned. “VCTs and EIS invest in small, early stage companies which might fail and have low levels of liquidity.”

Another move investors may wish to consider is shifting money into multi-asset funds or investment trusts because fund managers can buy and sell assets and rebalance their portfolios without incurring tax.

Investing in gilts is a further option because capital gains on government bonds are tax free. “A theoretical gilt yielding 4% entirely through capital gains is equivalent to a cash account yielding 6.7% in the hands of a higher rate taxpayer and 7.2% in the hands of an additional rate taxpayer,” he noted.

The increase in CGT was less than some experts had anticipated but was problematic for four reasons.

First, basic rate taxpayers face a far more severe CGT hike than for those on a higher rate, which seems unfair.

Second, CGT smacks of double taxation. “For most people, capital gains build up on assets purchased with money that has already gone through the income tax wringer, so capital gains tax represents a second wave of taxation,” Khalaf explained.

In addition, “both the complexity and rate of capital gains tax serves to discourage investment in the stock market”, he continued, although “this is mitigated to a large extent by the protection afforded by pensions and ISAs”.

Last but by no means least, hiking CGT is unlikely to bring in much money for the Treasury.

Rachael Griffin, tax and financial planning expert at Quilter, said: “While this move is aimed at boosting revenue, is likely to have the opposite effect, as it discourages investment and leads to reduced economic activity across key sectors.

“In statistics produced by the government which model the revenue impact of certain policies, this is laid bare. For example, it found that a 10 percentage point increase in the higher CGT rate shows a significant negative impact, reducing revenue by £400m in 2025-26, £985m in 2026-27, and £2.25bn in 2027-28.”

High tax rates discourage people from selling their assets, which “has the effect of locking wealth into certain asset classes, reducing the flow of capital into the economy”, she explained. “This behavioural shift could undermine the government’s revenue-raising objectives, as fewer transactions mean less CGT collected overall.”

This paradox makes the CGT increase all the more frustrating.

Invesco’s new ETFs aim to capture long-term growth trends in the artificial intelligence, cybersecurity and defence sectors.

Invesco is adding three new products to its range of thematic exchange-traded funds (ETFs), offering exposure to the “powerful long-term trends” of artificial intelligence (AI), cybersecurity and defence.

The Invesco Artificial Intelligence Enablers UCITS ETF will focus on companies that drive the technology, infrastructure and services behind the growth and functionality of AI.

Invesco Cybersecurity UCITS ETF will hold firms specialising in protecting business and devices from unauthorised access via electronic means.

Finally, Invesco Defence Innovation UCITS ETF will invest in companies working on advanced weaponry and defensive systems to secure national borders.

All three will have an annual charge of 0.35%.

The ETFs will track indices developed by Kensho, a division of S&P Global Indices, which uses artificial intelligence and other ‘next generation’ technologies in constructing thematic benchmarks.

Gary Buxton, head of EMEA and APAC ETFs at Invesco, said: “While the potential of AI has really captured people’s imagination, solutions for cybersecurity and defence are now gaining traction as threats emerge across the globe.

“For investors, the question is how best to capture these opportunities today and into the future. We chose to work with Kensho for their intelligent approach to applying AI but also their expertise in understanding these rapidly evolving new technologies.”

Kensho’s methodology for index construction begins with a global pool of stocks screened through natural language processing (NLP) to identify companies associated with each thematic concept. Analysts at Kensho then classify companies based on their relevance to each theme, sorting them into ‘core’ and ‘non-core’ categories.

Core companies generate a significant portion of revenue from theme-aligned products and services, while non-core companies contribute indirectly, supplying essential components or infrastructure but not delivering the end-products themselves.

An overweight factor is applied to core companies to enhance pure-play exposure to the theme. Both categories use equal weighting, subject to diversification and liquidity constraints.

The AI and Cybersecurity indices also apply environmental, social and governance (ESG) filters, excluding companies with low ESG scores, involvement in controversial activities or non-compliance with principles from the United Nations Global Compact.

These new funds expand Invesco’s thematic ETF range, which already includes portfolios focused on blockchain, biotechnology and clean energy stocks.

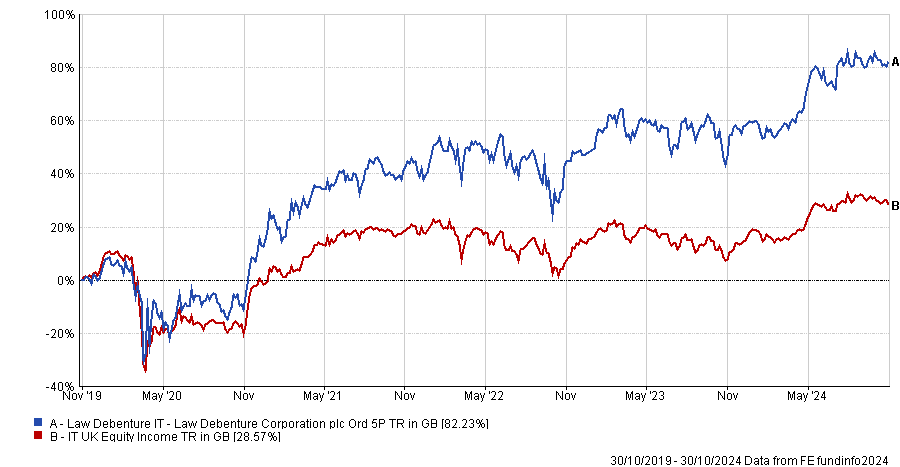

With alternative energy stocks, AIM-listed companies, investment trusts and zero-dividend shares, Law Debenture is far from a typical UK equity income fund.

Law Debenture may be one of the Association of Investment Companies’ Dividend Heroes but income is not the managers’ top priority. Instead, FE fundinfo Alpha Manager James Henderson and Laura Foll focus on growing the overall pot, first and foremost.

They have the luxury of investing for capital growth because alongside its equity portfolio, Law Debenture houses a professional services firm. Worth 20% of the trust’s assets, it contributes more than one-third of the income, providing a cushion.

Henderson said: “My view is that income funds should always focus on growing the capital first. If you grow the capital and have a bigger pot of money, it's much easier to produce sustainable income growth. If you try too hard on the income and you bleed the capital to produce the income, you [hit] a brick wall.”

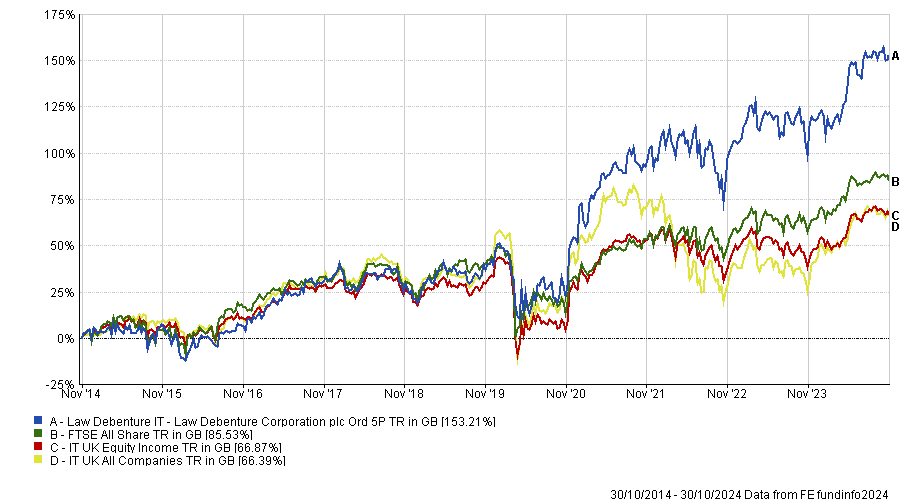

This approach has paid off. Law Debenture is the best performing investment trust in the IT UK Equity Income sector over both five and 10 years. Not only that, but it has pulled ahead of every single trust in the IT UK All Companies sector and beaten the FTSE 100 and FTSE All Share indices over five and 10 years as well.

Performance of trust over 10yrs vs UK sector averages and FTSE All Share

Source: FE Analytics

It has also increased its dividend for 14 consecutive years, with a five-year annualised dividend growth rate of 11.1% as of 12 March 2024. The trust’s dividend yield was 3.7% as of 30 September 2024.

Below, Henderson told Trustnet why he is increasing his exposure to AIM-listed shares and which stocks have been his best performers.

Please describe your investment process

We use a contrarian approach to investing by focusing on value, but always with the belief that things are not just cheap, they are going to grow. Growth is what helps you avoid value traps.

How does having a professional services firm within the trust impact your investment approach?

Law Debenture’s professional services firm amounts to 20% of the trust’s assets but contributes 35% of the income. This allows us to have a lower-yielding portfolio than most income funds and a bigger universe of stocks we can look at.

In 2020, when a lot of companies were cutting or stopping their dividend because of the pandemic, half the income from the quoted sector disappeared. The professional services business contributed 65% of the trust’s overall income that year.

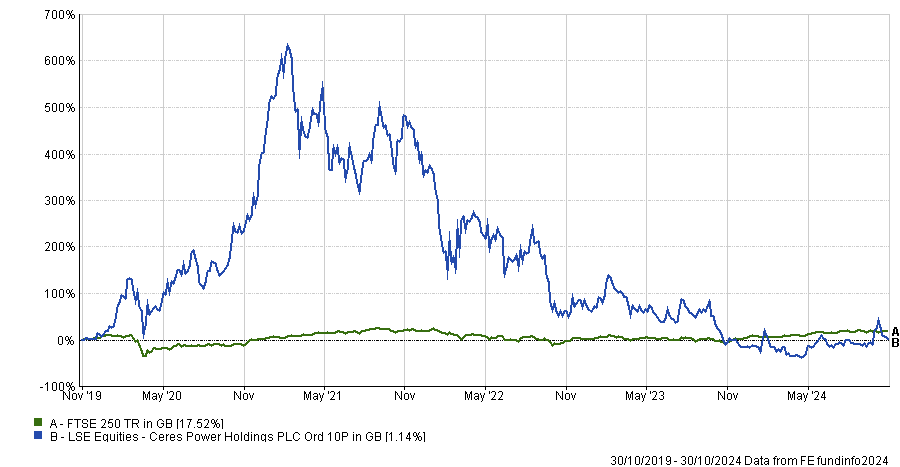

The board made a bold decision that year to put £70m into the UK equity market. I had the freedom to buy zero-yielding shares that had sold off without worrying about the income, which was the main reason for the trust’s strong five-year track record. We were able to hold companies such as Ceres Power Holdings and Rolls-Royce, which have been our biggest contributors over five years.

Performance of trust vs sector over 5yrs

Source: FE Analytics

What changes have you made recently?

We are increasing our AIM weighting, which is at 7% and I wouldn't go beyond 10%. We own small- and mid-cap stocks too but the real valuation anomaly is on AIM, because people have been so nervous about tax changes.

Before the Budget, people were saying that scrapping inheritance tax (IHT) relief on AIM stocks would see them fall as much as 30%. The market went up straight after the Budget, which tells you the doom had been priced in.

Some investors have concerns about the liquidity of AIM stocks but we can buy less liquid things and that's a real privilege we need to use. It's what you do differently that makes you perform differently.

We’ve been buying some alternative energy stocks. You wouldn't normally see them in an income fund because they're not going to pay dividends for another 10 years, but they should help grow the trust’s overall pot, which produces the income.

I’ve also been buying investment trusts that have fallen to very large discounts including Grit, which invests in African properties, and VH Global Sustainable Energy Opportunities.

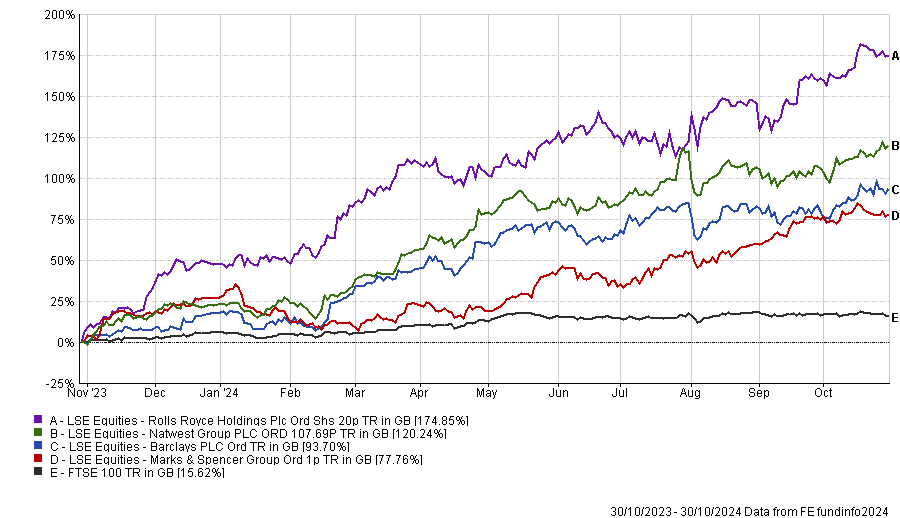

What have been your best and worst performers recently?

In the past year, the biggest contributor by quite a considerable amount is Rolls-Royce and, after that, Marks & Spencer. NatWest and Barclays are up there.

Performance of shares vs FTSE 100 over 1yr

Source: FE Analytics

Ceres has been dreadful this year, but on a five-year view it has been a top contributor. I sold quite a lot of the holding in 2022 and 2023 and I've been buying it back recently.

Ceres Power vs FTSE 250 over 5yrs

Source: FE Analytics

With Ceres, the market got over-excited about how quickly hydrogen would replace more traditional fuels in fuel cells and people thought hydrogen might even go straight into cars. When things didn't happen as quickly as people had hoped, disappointment set in.

Something out of left field that hurt us was Morgan Advanced Materials, which had a cyber-attack. Everyone came to work one morning to see a pirate flag on their screens and, shortly after that, they couldn’t see where any of their stock was or what they'd sold. That caused a lot of disruption, which led to share price weakness.

What do you enjoy doing outside of investing?

I train racehorses. I used to ride in jump races, but I now just ride my horses at home.

Brunner’s Bishop dissects the arguments for and against owning Nvidia.

Semiconductor manufacturer Nvidia has been the most successful company of the past few years. Portfolio managers who own it have seen their returns skyrocket and those who don’t say it’s a controversial stock to buy.

Julian Bishop, co-manager of the Brunner investment trust, belongs to the latter cohort, but if he could go back, he would certainly buy it, he admitted, as not owning Nvidia has had the greatest negative impact on the trust over the past year.

“When calculating the combination of percent declines and position size, the worst active contributor for us was not holding Nvidia. That cost our relative performance quite a lot,” he said.

A natural question could therefore be why he still hasn’t bought it, and Bishop said this conversation has been “talked about to death” at Brunner.

The pros are fairly evident and self-explanatory. According to Bishop, Nvidia is “incredibly profitable” and far from being a “dot-com bubble-type, nonsense stock”. It also has “a very high market share”, and what it does is “absolutely critical” to the build-out of artificial intelligence (AI) infrastructure.

“These are all things that we would typically look for in a company,” admitted the manager. “On top of that, there is also the exceptional growth in the past few years, as AI has exploded onto the scene.”

But there are quite a few cons that stopped the Brunner portfolio from welcoming the semiconductor darling.

Firstly, people are spending “an absolute fortune” on AI already. Next year, Nvidia is expected to sell $100bn worth of chips, which is “by any stretch of the imagination, a vast amount of money”.

Around that, one must also take into account the data centres needed to make AI work which “would probably add another $100bn” to the amount tech companies are spending.

“With $200bn of costs in a year, they would need to generate at least $400bn of sales to get an adequate return,” he said.

“But at the moment, we're not even close. Let's not forget that at the moment, no one is actually making any money with AI.”

Beyond this question mark over demand, there are also barriers to entry to consider, as “everybody is trying to break the moat around Nvidia”.

Because it only sells to a few customers (the likes of Meta, Google, Microsoft, Amazon and Tesla), it is even more vulnerable, as they are all trying to develop their own versions.

“When Microsoft is spending $10bn a year on these chips, its procurement department has every interest of breaking down Nvidia’s moat,” Bishop said.

“There is a saying in technology that at the end of the day, all hardware is a toaster. Ultimately, everything, no matter how complex it looks, can be replicated by somebody somewhere, and it becomes commoditised. With time, prices deflate and profit pools get eroded.”

The second question mark was therefore: How much in the ecosystem is built around Nvidia? Or, to use an analogy: Is Nvidia Apple, or is it Samsung?

Apple makes great profits selling smartphones for the only reason that it has been able to create an ecosystem around them – the apps, all the software, the brand, the retail network. But most smartphones are commoditized, the manager explained.

“You would be amazed at how little money Samsung makes making smartphones,” he said. “Even though it is probably making as many smartphones as Apple, they're the commoditised end of the spectrum.”

Nvidia does have some software and systems around what it does, it isn't just a microchip that might get commoditised with time. So for Bishop, the real debate is how much of an ecosystem is around Nvidia, and whether that will protect it against competition.

Finally, the manager was also mindful of previous technological revolutions. All the top companies at the time of the dot-com bubble, for example, “just faded to nothing”.

Bishop recalled Cisco Systems, which built all the routers that were used to sort internet traffic, or Global Crossing, which laid the fibre optic cables across oceans that exist to this day but went bankrupt because “loads of other people had cables too”.

“Companies such as these did the world a favour by building incredible infrastructure that allowed all this technology, but it is companies down the road, such as Amazon and Google, that made use of this technology and the most of the money. We think it might be similar this time,” Bishop said.

“I have no doubt that AI’s influence will be probably overestimated in the short term and underestimated in the long term. But it's not quite clear to us that the people who build it will be the ones that make money.”

Performance of trust against sector and index over 5yrs

Source: FE Analytics

So far, these considerations have stopped Bishop from buying Nvidia, preferring instead “guaranteed winners” such as Taiwan Semiconductors, the trust’s best contributor over the past year (which makes up 3.3% of the portfolio), and Microsoft, the trust’s top holding at 6.4%.

But he “certainly wouldn't rule out” buying it in the next 12 months or so.

“It's part of our job to protect our clients from the madness of crowds when bubbles develop and irrationality can settle in. But Nvidia is not in that class, and the valuation, if it can prove that the moat is strong enough, is not crazy. It is possible we could buy it in the year to come, absolutely,” he concluded.

GCP Infrastructure is improving its risk-adjusted returns and is on track to narrow its discount.

You could argue that investing in infrastructure is boring. Long-term contracts, predictable cash flows, must-have assets, availability rather than demand-linked revenues, inflation-linked income and counterparties with strong credit ratings ought to make for ‘sleep at night’ investments.

For many years, the ratings on listed infrastructure funds reflected these characteristics. That all changed in 2022 as interest rates started to rise. Money was diverted into cash deposits and bonds. Selling pressure allowed discounts to open up, that left some investors disillusioned, which compounded the problem.

Today, even though rates are coming back down again, every London-listed infrastructure fund is trading on a discount. However, the security of income from these funds was not really in doubt. Trusts kept hiking dividends and now they all trade on attractive dividend yields.

While all of these funds look too cheap to my eyes, one rating appears particularly anomalous – that of GCP Infrastructure, a £700m market cap investment company. Managed by Phil Kent and Max Gilbert, supported by an experienced team at Gravis, the company invests across a range of different infrastructure sectors, although its focus has shifted more towards renewable energy infrastructure over the last few years, which gives it strong environmental, social and governance (ESG) credentials.

The main difference between GCP Infrastructure and the bulk of its peers is that it structures its investments as loans. That means they are protected by a ‘cushion’ of equity that takes the first hit if anything goes wrong. However, that margin of safety is not reflected in its rating.

Barring Digital 9 Infrastructure (which took a number of wrong turns and is now in wind up mode), GCP Infrastructure’s shares trade on the widest discount (currently almost 30%) and the highest yield (9.2%) within its infrastructure subsector.

My belief is that the company was particularly badly affected by selling pressure related to the cost disclosure problems that have plagued the investment company sector but, fortunately, are now being addressed.

In an effort to remedy its discount, the board of GCP Infrastructure launched a capital recycling programme in 2023. The ambition was to release £150m (roughly 15% of the portfolio) to rebalance sector exposures, apply funds towards a material reduction in the revolving credit facility and support the return of at least £50m in capital to shareholders before the end of 2024.

GCP Infrastructure’s first disposal, raising £31m, was of its interest in loan notes secured against a 52.9MW Scottish wind farm. The price was a 6.4% premium to asset value and the money was used to reduce the outstanding balance on its revolving credit facility. By the end of September 2024, that balance was down to £57m (from £154m as at end December 2022 and £104m as at 30 September 2023).

However, the company has dropped a heavy hint that something more substantial is in the works. On 24 October 2024, it announced its net asset value as at end September 2024. The figure (105.22p per share) came in a little lower than the value at end June.

Normally, GCP Infrastructure would provide a detailed breakdown of the underlying movements that contributed to this, but this time it declined to do so. The statement said the company is in active due diligence and negotiations on disposals of material components of its investment portfolio and does not wish to risk such processes through publication of further detail on the constituent movements in the NAV.

It sounds to me as though we could be on the verge of a disposal large enough to restart its buyback programme. Currently, this has not been reflected in the share price, which feels like an opportunity too good to pass up.

There is more to GCP Infrastructure than the short-term discount narrowing opportunity and the chance to lock in an attractive yield. The manager sees the potential to use the capital recycling programme as a way of improving the quality of GCP Infrastructure’s portfolio, reducing the portfolio’s sensitivity to factors such as volatile power prices and removing exposure to supported living accommodation (thereby reducing the duration of the portfolio).

At the end of June 2024, supported living accounted for around 12% of the portfolio, around a quarter was exposed to private finance initiatives, public-private partnerships and similar assets, and the balance to a broad spread of renewables assets. These range from onshore wind and solar, through to geothermal (it financed a well that is being used to heat the Eden project in Cornwall) and electric vehicle charging.

In addition to the disposal activity related to the capital recycling programme, there is a natural pattern of loan maturities and reinvestment. The advent of higher interest rates is allowing the managers to improve the portfolio’s risk-adjusted returns. Once the disposal programme is complete, I would expect that the improved quality of the portfolio will be easier to appreciate. That should support a more permanent narrowing of the discount.

James Carthew is head of investment companies at QuotedData. Thew views expressed above should not be taken as investment advice.

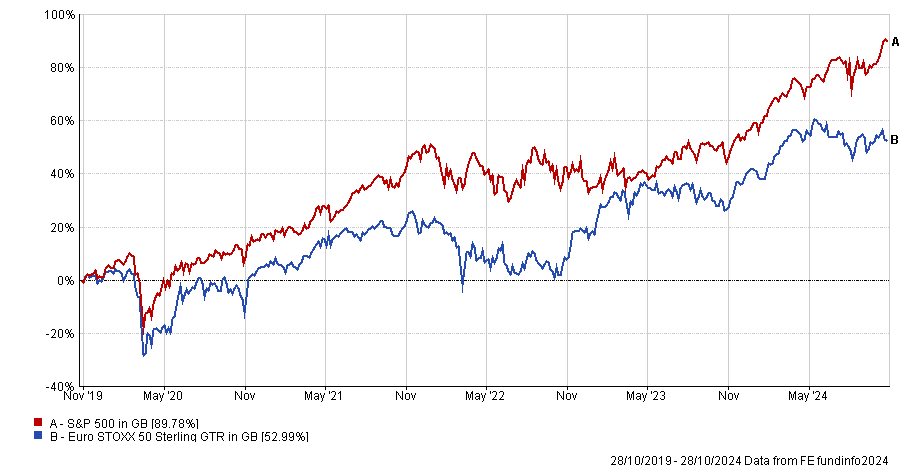

Trustnet examines which European funds delivered the best risk-adjusted returns during the past five years.

Contested elections, geopolitical tensions, the Covid-19 pandemic and investor apathy have tested European equity managers to the limit in recent years.

While this is true of many regions, Europe has also struggled by dint of being less exciting than the US. The Euro STOXX 50 has gained a relatively lacklustre 53% over the past five years, compared to the S&P 500's 89.8% rise, as the chart below shows.

For active managers in this challenging market, striking the right balance between risk and reward has been crucial.

Performance of indices over 5yrs

Source: FE Analytics

As part of an ongoing series, Trustnet is focussing on funds with top-decile returns as well as top-decile Sharpe ratios over five years. Below we look at funds in the IA Europe Excluding UK, IA Europe Including UK and IA European Smaller Companies sectors.

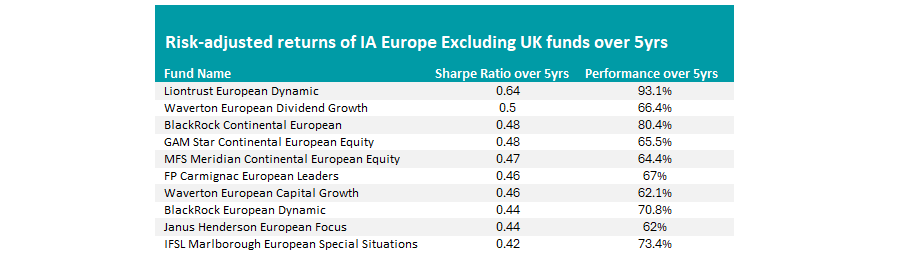

First, in the IA Europe Excluding UK sector, a range of strategies achieved top decile risk-adjusted returns over the past five years.

However, it was the £1.5bn Liontrust European Dynamic fund, led by James Inglis-Jones and Samantha Gleave, which stood out.

Risk-adjusted returns of IA Europe Excluding UK funds over 5yrs

Source: FE Analytics, total returns in Sterling, Data to 30 Sep 2024

Over five years, this portfolio enjoyed best-in-class returns of 90.3%. Given its seventh-decile volatility of 16.5%, it was one of the more 'gung-ho' approaches in the peer group. This higher risk, higher reward strategy resulted in a five-year Sharpe ratio of 0.64, better than its nearest competitor by 0.14.

Moreover, the strategy has enjoyed long-term success with consistent top-quartile returns across other periods. For example, over three years the fund was up by 24.2% and over 10 years it surged by 214.3%.

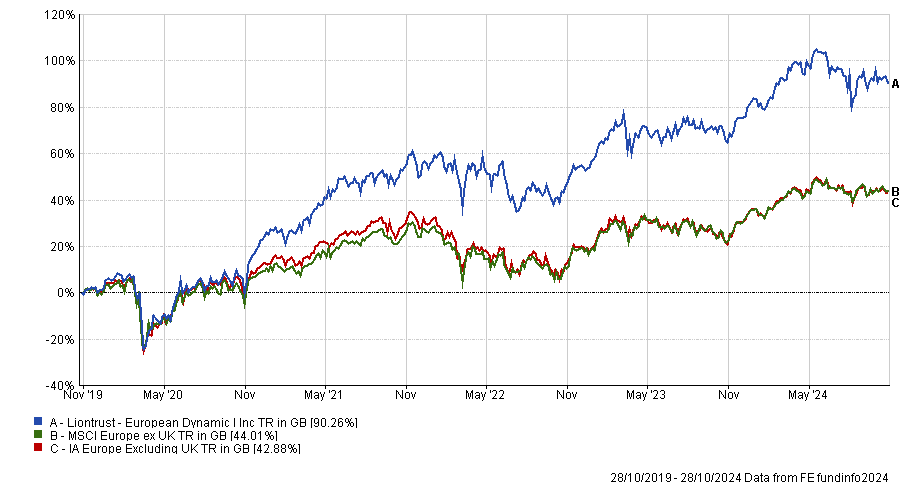

Performance of fund vs sector and benchmark over 5yrs

Source: FE Analytics

Due to its consistent success, the portfolio has been awarded an FE fundinfo Crown Rating of five. Analysts at FE Investments said: “The combination of deep quantitative underpinnings combined with intelligent execution and stock picking from two highly experienced investors is very attractive.”

Inglis-Jones and Gleave “have proven their ability to outperform independent of whether the value or growth style is in favour, providing a compelling core offering for investors in European equity”, the analysts continued.

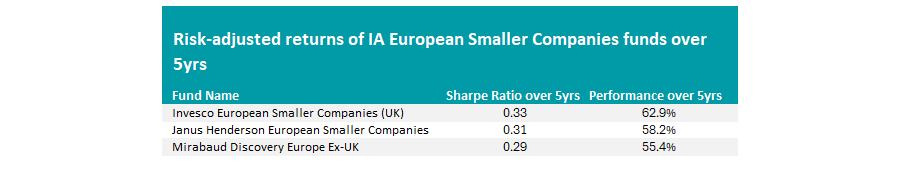

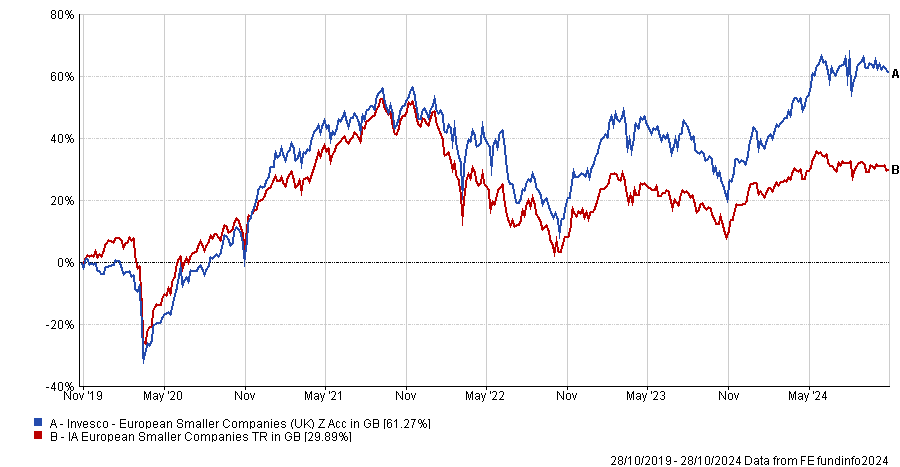

Turning to the IA European Smaller Companies sector, just three portfolios matched our criteria.

Risk-adjusted returns of IA Europe Including UK funds over 5yrs

Source: FE Analytics, total returns in Sterling, Data to 30 Sep 2024

While the differences between risk-adjusted returns were minimal, this was another sector where more aggressive strategies, such as the £220m Invesco European Smaller Companies portfolio, shined.

Over the past half a decade, it surged by 62.9%, the best performance in the peer group. With an eight-decile volatility of 20.2%, the strategy paired a higher-risk approach with high rewards, leading to the best risk-adjusted returns in the sector of 0.33.

It has replicated these results more recently, ranking in the top quartile for returns over the past one and three years.

Performance of fund vs sector over 5yrs

Source: FE Analytics

However, it has not been smooth sailing for the Invesco strategy over the past five years. Its high volatility approach has led to frequent fluctuations in performance, which may have tested investors' patience. For example, in 2023 and 2021, it slid into the second and third quartiles for calendar year performance.

Moreover, 2019 proved particularly challenging for the fund, which rose in value by just 0.3%, one of the worst results in the sector.

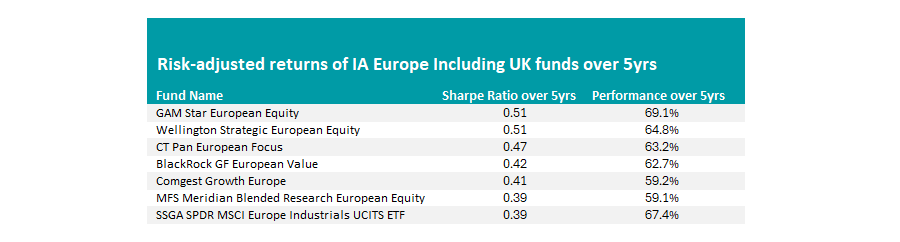

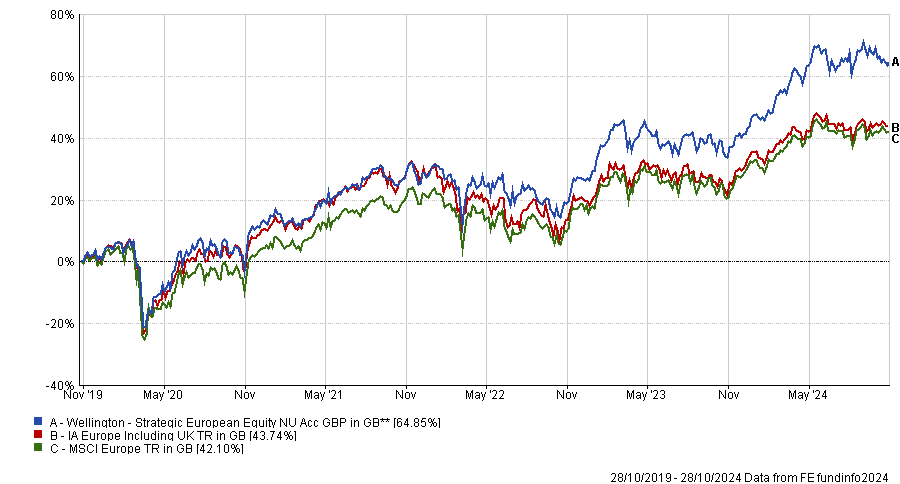

Finally, in the IA Europe Including UK sector, two funds enjoyed the best five-year risk-adjusted returns: the £2.6bn Wellington Strategic European Equity and the £44m GAM Star European Equity funds.

Risk-adjusted returns of IA Europe Including UK funds over 5yrs

Source: FE Analytics, total returns in Sterling, Data to 30 Sep 2024

While both funds boasted a five-year Sharpe ratio of 0.51, Wellington Strategic European Equity stood out as one of the most cautious strategies on our list.

At 13.9% volatility, it ranked in the third decile for risk over the past half-decade. Despite a comparatively low-risk approach, it enjoyed some of the best results in the whole sector, climbing by 64.8% over the past five years.

Moreover, the portfolio generated 2.4% in alpha, one of the best results in the sector. This indicated that during periods of strong performance, the fund delivered supranormal returns compared to its benchmark.

Performance of fund vs sector and benchmark over 5yrs

Source: FE Analytics

The portfolio successfully replicated these results in the near and longer term. Over 10 years, it rose in value by 184.9%, the fourth-best return in the peer group.

It has enjoyed further top-quartile performance over the past one and three years, rising 22.4% and 27.9%, respectively.

Previously in this series, we have looked at the IA Mixed Investment and Flexible Investments, IA North America, IA Global and the IA UK All Companies sectors.

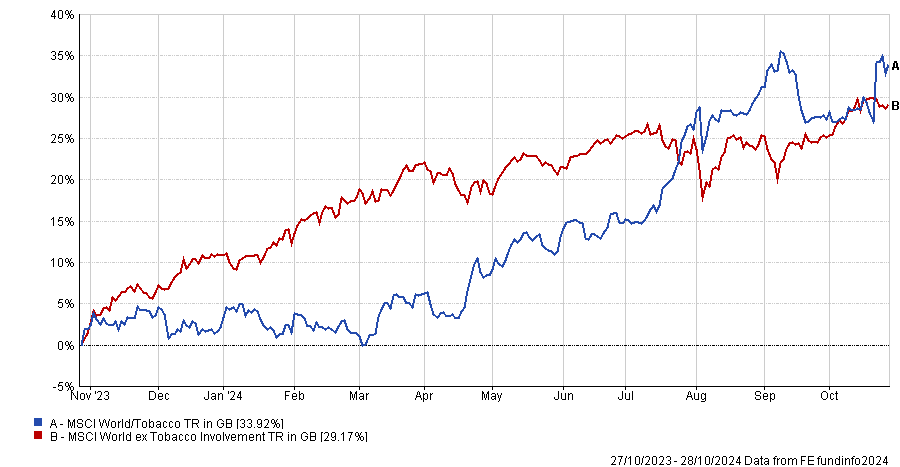

“There is nothing that combines the quality, value and income attributes of the tobacco sector”, said Troy Asset Management’s James Harries.

Tobacco is making a comeback. In the past six months, tobacco companies have risen above the rest of the global equity market, as the chart below shows.

They are also going through an evolution, offering less harmful products such as ‘heat not burn’ and vapes, and becoming more sustainable businesses, all of which might make them more palatable to investors, said Trojan Global Income manager James Harries. In the future, he thinks they will become known as “nicotine consumer products companies”.

Performance of indices over 1yr

Source: FE Analytics

“Although people are smoking less, you could argue that consumption of nicotine is increasing,” Harries said. At 5.1%, British American Tobacco is the third-largest holding in his portfolio.

Harries is not alone in backing the revival. Imperial Brands, formerly Imperial Tobacco, is the largest holding in Fidelity Special Values, taking up 4.2% of the portfolio.

But while FE fundinfo Alpha Manager Alex Wright, who manages the trust, considers tobacco to be a defensive play, cigarette manufacturers have made it into growth funds as well.

Stephen Yiu, who runs the £1.1bn Blue Whale Growth fund, has built up a “sizable” 4% position in Philip Morris this year.

“Everyone wants to talk about Microsoft, but the stock has gone up just about 15% this year, so it has been tracking the market,” the Alpha Manager said. “And yet interestingly, Philip Morris, this little boring consumer staples company, has gone up about 30% this year.”

Yiu was impressed by Philip Morris’ plans to return to the US (a market it exited in 2008) and expand the reach of its ‘I quit ordinary smoking’ (IQOS) machines, which use ‘heat not burn’ technology and have been approved for sale in the US.

“On top of that, two years ago the company acquired Swedish Match, meaning that over 50% of the business is now in non-traditional cigarettes,” Yiu noted.

BNY Mellon Multi Asset Income manager Paul Flood took profits from British American Tobacco’s corporate bonds in June and re-invested the proceeds in the company’s shares.

“The equity valuation was very low and the company was paying a 9% to 10% yield, so it seemed like a sensible thing to do from an income fund perspective. It has also helped us to bring the duration down a little bit as the year went on,” he explained.

To address potential concerns around environmental, social and governance (ESG) principles, Yiu said that Philip Morris is “trending towards being more environmentally-friendly than one could expect”, given the less harmful products it now focuses on.

Harries agreed that “these companies are able to offer products without tobacco, which would be attractive to some investors”.

The ethical version of the Troy fund, Trojan Ethical Global Income, excludes tobacco companies and other sectors. For this reason, it has a marginally lower yield, although its income is growing at slightly faster pace. The ethical version might therefore be suitable for younger investors with more of a total-return mindset, he explained. On the other hand, the non-ethical version is a more classic income fund that might appeal to an older cohort.

As Halloween approaches, it’s time for the Bond Vigilantes’ yearly round-up of the spookiest charts in global finance.

It’s not just ghosts and ghouls that are causing fear this Halloween – financial markets are also giving us plenty of reasons to be spooked. From crumbling consumer confidence to rising debt burdens, the economic landscape is littered with eerie signs of instability.

The five charts below from M&G Investments' Bond Vigilantes reveal unsettling trends in global markets. While surface-level data may look reassuring, a deeper dive shows that the scariest threats could be the ones lurking just out of sight.

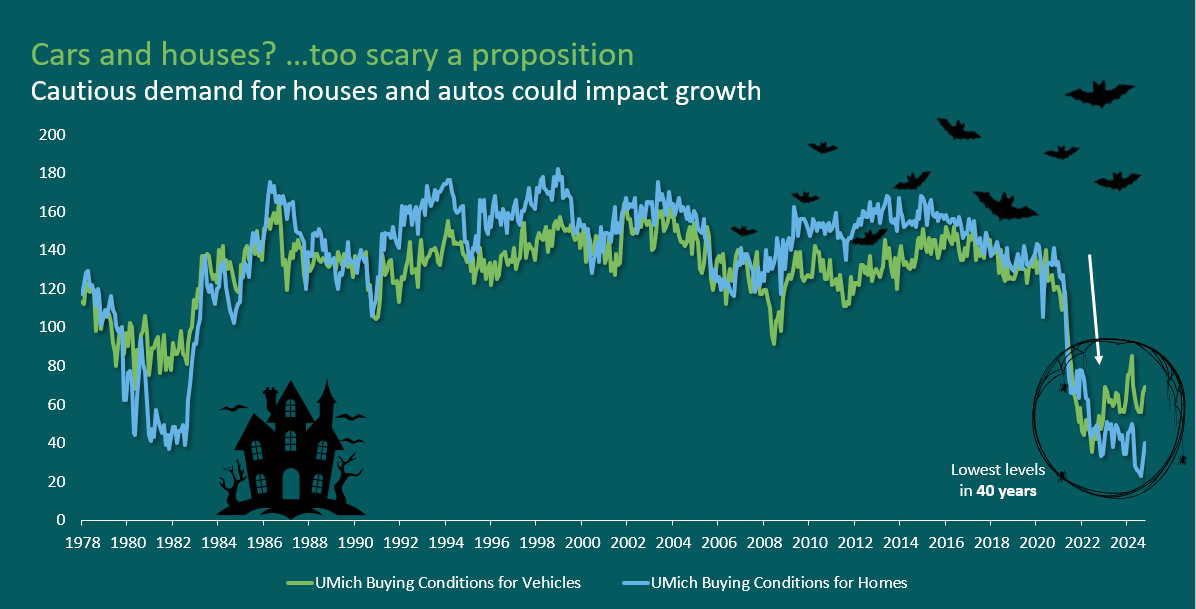

Cars and houses? … Too scary a proposition

According to University of Michigan surveys, consumers view this as the worst time in 40 years to buy a house or car – a worrying sign for consumer intent. Big purchases like these can be crucial drivers of economic growth and with buying intent so low, we could be underestimating the severity of the slowdown.

Sources: M&G, University of Michigan, Bloomberg, data to Oct 2024

As consumer intent wobbles, could the labour market be telling its own tale of uncertainty?

Employees frightened to quit; companies frightened to hire

The US labour market appears healthy, especially after September’s non-farm payrolls exceeded economists’ expectations and unemployment fell to 4.1%. However, beneath the surface, both hiring and quits rates have dropped to levels typically seen in recessions.

Sources: M&G, Bloomberg, data to Oct 2024

Companies are hesitant to hire full-time workers, and employees are reluctant to quit due to job security concerns and fewer opportunities available. These signs of weakness suggest that the effects of restrictive monetary policy may be more severe than the headline labour market numbers imply.

It may not be just the labour market – economic fragility is reverberating through the economy, driven by the enduring grip of monetary policy.

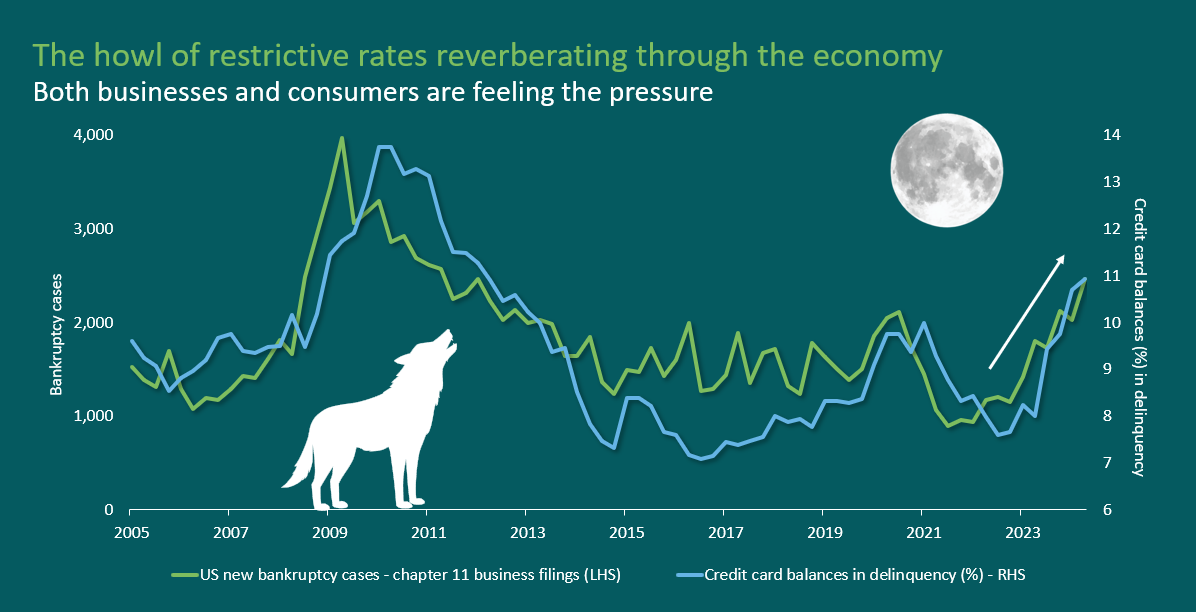

The howl of restrictive rates reverberating through the economy

Monetary policy was restrictive for a long time and since it works with a lag, its effects are only now becoming evident.

Although central banks have begun easing, policy remains more restrictive than what might be deemed neutral and this is impacting both businesses and consumers. In the US, Chapter 11 filings are rising steadily, while credit card delinquencies over 90 days are climbing to levels last seen following the global financial crisis.

Sources: M&G, Bloomberg, data to Oct 2024

Until monetary policy significantly loosens, these trends may continue to persist.

While economic and financial pressures mount, are all risks being priced into credit markets?

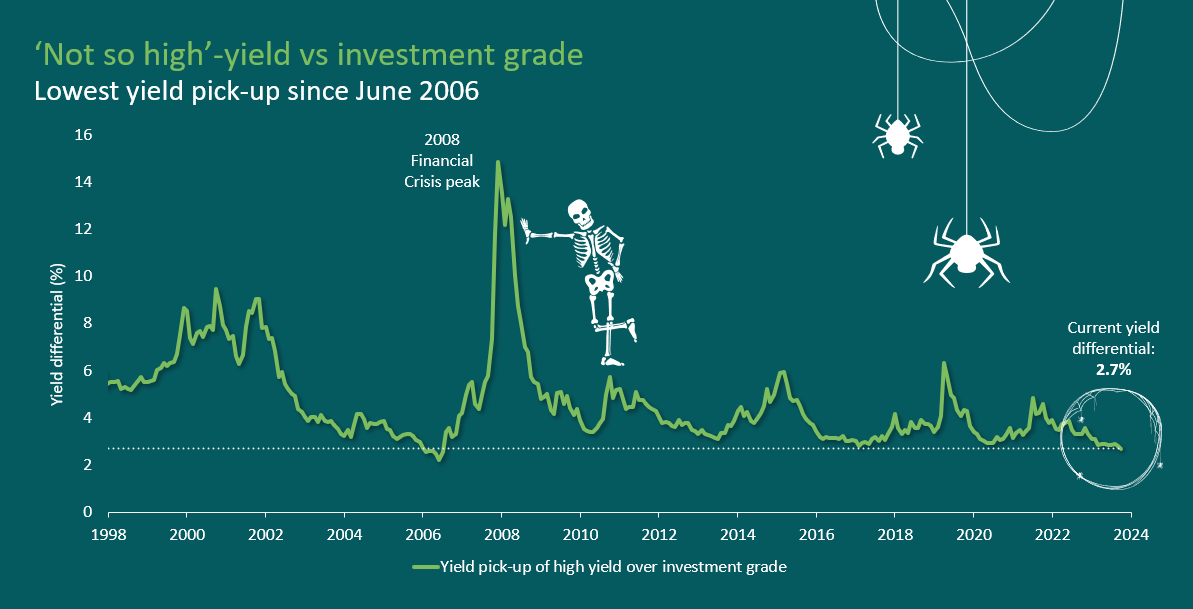

‘Not so high’-yield vs investment grade

Despite the unsettling warning signs, credit markets are pricing in minimal risk of a major slowdown, let alone a recession that could significantly impact credit fundamentals. In fact, the spread between investment grade and high-yield bonds has narrowed to just under 2.7% — the lowest level since 2006.

Could investors be underestimating the potential for economic turbulence ahead?

Sources: M&G, Bloomberg, data to Oct 2024

Beyond the bond markets, another haunting issue brews in the form of rising government debt…

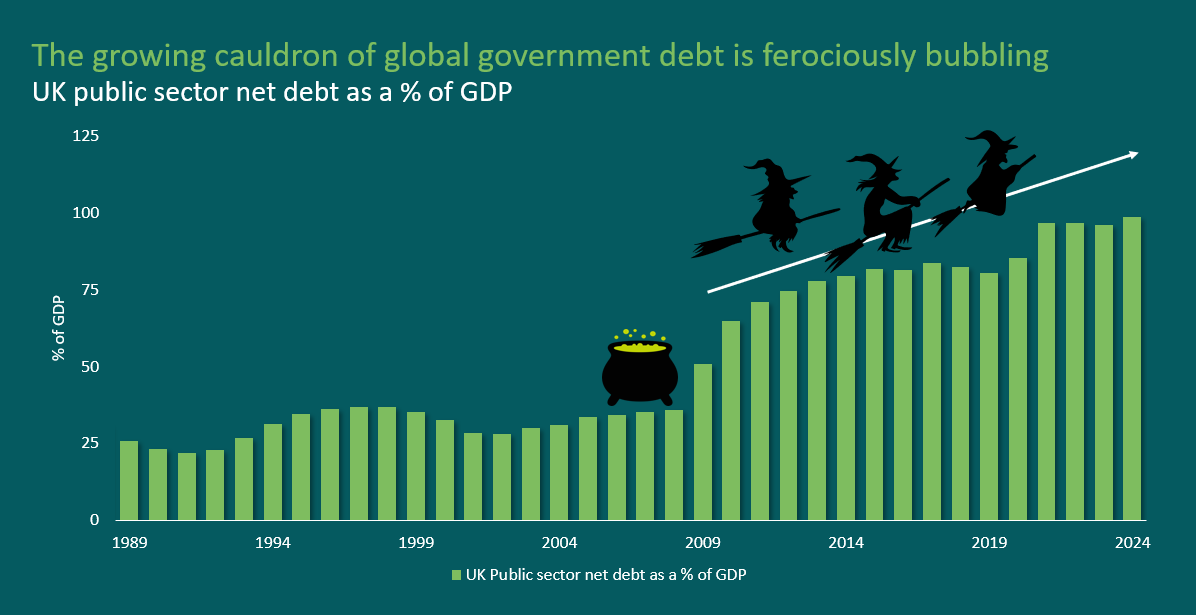

The growing cauldron of global government debt is ferociously bubbling

It’s no surprise that global government debt levels have been steadily rising, but it’s worth highlighting how concerning this trend is. In the UK, for example, public sector net debt as a percentage of GDP is alarmingly high.

Sources: M&G, Bloomberg, data to Oct 2024

High debt can impact growth by diverting government spending away from productive investments toward debt servicing. It may also force central banks to consider fiscal risks when raising interest rates, as aggressive hikes could destabilise public finances.

With current debt levels resembling those seen during recessions, will governments be able to respond when the next downturn hits?

Joe Sullivan-Bissett is a fixed income investment director at M&G Investments. The views expressed above should not be taken as investment advice.

Government bond markets have taken fright but equity investors seem remarkably complacent and that could come back to haunt them.

Government bond markets appear well and truly spooked this Halloween. Yields on US treasuries have surged in the past six weeks in reaction to concerns about Donald Trump’s potential return to the White House, US fiscal irresponsibility, the sceptre of rising inflation and geopolitical tension.

Equity markets, on the other hand, have been remarkably complacent but that could come back to haunt investors, according to Emma Moriarty, a portfolio manager at CG Asset Management.

Asset valuations are divorced from what’s happening in the real world

The valuations of equities and corporate bonds are starting to look unrealistic given the latent risks, Moriarty said. “Asset valuations have become way out of alignment with what is actually happening in the real economy. There does seem to be this de-linking going on,” she said. Valuations are “starting from a really inflated place”.

US equity valuations are the most obvious example of an expensive asset class but the same is true of corporate bonds. “We've now been in a situation where interest rates have been elevated for some time. We know that there's this wall of refinancing that has to happen in the US and the UK next year and yet, credit spreads are at historical lows at exactly this point when, actually, risk sentiment should be a little bit more elevated,” she explained.

The Bank of England’s Financial Policy Committee recently said that valuations across several asset classes, particularly equities, were “stretched” and “markets remain susceptible to a sharp correction”.

The question then becomes whether there is an imminent catalyst for a correction – and if the US election could be it.

“One thing we can say is that a Trump victory would crystallise this path of much wider fiscal deficits so that is probably a potential moment for a treasury market repricing,” Moriarty observed.

The impact of a Trump victory on equity markets is much harder to forecast, especially because Trump's policies are “not necessarily clear or consistent with each other”, she added.

Complacency has been building up

In a similar vein, Chris Metcalfe, chief investment officer of IBOSS Asset Management, said financial advisers and their clients are all focused on the potential upside from equity markets. While everyone is asking questions about further stock market gains to make sure they aren’t missing out, very few people are asking about downside risk, drawdowns or volatility, he said.

Complacency has been increasing because “equities have been going up so well for so long”, he observed.

It is not complacency per se that could spook investors but the disappointing returns it presages. “There is always complacency” just before market corrections, Metcalfe observed. “You don’t tend to get markets with a lot of fear [leading into] sell-offs”.

Nick Clay, manager of TM Redwheel Global Equity Income, thinks investors are pinning all their hopes on a soft landing in the US and are under-prepared for any other scenario. “What scares me is when markets are convinced that a particular outcome is a foregone conclusion, as this is invariably when risk is most elevated,” he said.

“Today, markets continue to push through all-time highs on the conviction that the Goldilocks outcome is a certainty that nothing can derail, impervious to geopolitical tensions, upcoming US elections or slowing growth in many areas.”

US equities could flatline in real terms

All this complacency is setting the scene for disappointment. Goldman Sachs reckons that the S&P 500 will return just 3% per annum over the next decade. After accounting for 2% inflation, fund managers’ fees and foreign exchange risk, those meagre gains could be eroded to almost nothing.

The investment bank’s forecasts are more pessimistic than its peers because it has factored in the extreme concentration of US equity markets. The S&P 500’s 10 largest stocks now amount to 36% of the benchmark. An extremely concentrated index reflects a less diversified set of risks so will probably be more volatile, said David Kostin, chief US equity strategist at Goldman Sachs.

Yield on 10-year treasuries could spike to 5%

Turn to the bond markets and everything looks much more frightening.

The yield on 10-year treasuries has surged by about 60 basis points since the US Federal Reserve cut interest rates by 50 basis points on 18 September.

Arif Husain, head of fixed income at T. Rowe Price, thinks the bond market sell-off could gather momentum and that the 10-year treasury yield could “test the 5% threshold in the next six months”.

Gael Fichan, head of fixed income at Bank Syz, said yields have risen due to “multiple forces at play: stronger-than-expected US macroeconomic data, commodity price inflation fuelled by Chinese stimulus measures, and recent statements by Fed policymakers advocating a higher terminal rate”. The increasing probability of a Republican ‘sweep’ (taking the presidency, Senate and House) is also fuelling market anxieties.

The MOVE index, a barometer for bond market volatility, hit a one-year high on 7 October 2024 – surpassing levels seen during the Silicon Valley Bank collapse and the Fed's 75-basis-point rate hike in June 2022.

“According to MOVE creator Harley Bassman, this marked the first time that one-month options extended beyond the election date, reflecting heightened political anxiety around future yields,” Fichan said.

The AIM market breathes a sigh of relief, while sterling and equities surge.

Chancellor Rachel Reeves delivered the first Labour Budget in almost 15 years today. Financial markets responded positively, as did many fund managers.

Rathbone UK Opportunities manager Alexandra Jackson said equity markets liked the Budget, with sterling also rallying in the immediate aftermath. The chancellor has “threaded the needle of raising the taxes she needs without spooking investors”, she concluded.

Adrian Gosden, UK equities fund manager at Jupiter Asset Management, said the Budget was “tough but fair” and declared: “The UK is open for business”.

AIM stocks get a reprieve

The AIM market rallied on news that inheritance tax (IHT) relief had not been abolished altogether, even though it was halved. Abby Glennie, manager of the abrdn UK Smaller Companies fund, said that the government “did not quite throw in the hand grenade for AIM entrepreneurs and investors that many expected”.

Even so, investing in AIM stocks is now less attractive, she said. “With tax benefits halved, investors will need to be more positive on return prospects to allocate cash to AIM and this could swing allocations towards other areas.”

Capital gains tax hikes could impact investment decisions

Richard Stone, chief executive of the Association of Investment Companies, expressed disappointment at the increase in capital gains tax (CGT), coming “from a government which has put so much emphasis on investment and growth”.

“Increased tax on profits from shares is a disincentive to invest in the stock market outside an ISA or pension,” he said.

“Bringing all AIM shares and pension funds into the scope of inheritance tax will act as a disincentive to build and retain those long-term investments for the benefit of future generations.”

As a consequence of a higher CGT, multi-asset portfolios should become more appealing, according to BNY Investments’ head of retirement Richard Parkin.

“We expect the higher CGT rates will lead to more advisers looking at multi-asset funds rather than model portfolios. While CGT is still payable on these funds, using a single fund structure makes it easier for advisers to time when gains are realised,” he said.

“These higher rates of CGT and lower thresholds make it even more important to maximise tax-advantaged investments such as ISAs and pensions and it’s good to see that the tax benefits of these vehicles have largely been maintained.”

That said, Rachael Griffin, tax and financial planning expert at Quilter, pointed out that CGT is paid by only 350,000 people per year (equating to 0.65% of the adult population).

“This will not be a change that is felt throughout the nation. But while this move is aimed at boosting revenue, is likely to have the opposite effect, as it discourages investment and leads to reduced economic activity across key sectors,” she said.

"One key problem with raising CGT is that it doesn’t necessarily guarantee more tax revenue, because it results in fewer people selling their assets to avoid triggering the tax. This has the effect of locking wealth into certain asset classes, reducing the flow of capital into the economy.”

Gilts yields fell initially then rose

Yields on 10-year gilts fell initially when the Budget was announced but then shot up during yesterday afternoon, in anticipation of increased government borrowing.

Shamil Gohil, fixed income portfolio manager at Fidelity International, said: “With £20bn more of issuance pencilled in skewed to the long end, that will lead to some curve steepening.”

Monetary easing is likely to boost emerging market local currency bond prices, but active investors should find plenty of idiosyncratic opportunities since easing cycles will not be synchronized.

Emerging market local bonds returned a stellar 12.7% in 2023 in US dollar terms but lost 3.7% in the first half of 2024 amid a strong dollar, concerns about fiscal discipline in Brazil and the prospect of post-election institutional deterioration in Mexico.

The asset class recovered strongly between July and September, delivering a 9% return in a single quarter despite market turbulence and the unwinding of yen-funded carry trades. While Brazil and Mexico’s issues persist, investors are shifting their focus to US events that are moving the dollar and potentially boosting local assets in emerging markets.

The US presidential race appears very tight. Kamala Harris is slightly ahead in the national polls but Donald Trump could still win, given that the results for many swing states will be a toss up, according to opinion polls.

The dollar would likely strengthen under a Trump victory and weaken otherwise due to two economic reasons: taxes and tariffs. Trump has promised to extend the corporate tax cuts he introduced during his first presidency, which increased competitiveness and attracted capital flows from corporations and resulted in a stronger dollar. Harris, on the other hand, has promised that the wealthiest Americans and largest corporations will pay their fair share.

If elected again, Trump would impose more tariffs on China and potentially on the rest of the world. A country facing higher tariffs will see its currency weakened by market forces to compensate for lower competitiveness. This was evident in the Chinese yuan during the 2018 trade wars.

We expect the US-China rivalry to continue regardless of the outcome of the election, though it is likely to be less disruptive under Harris.

Taxes and tariffs point towards a stronger dollar if Trump wins. If Harris wins, the sentiment towards emerging markets should improve amid prospects of a weaker dollar.

Can we stay in the middle of the so-called US ‘dollar smile’? Currencies strengthen when their economies are doing well and vice versa, but the US dollar also strengthens in times of crisis on safe haven flows due to its reserve currency status.

The dollar remained strong after the Covid pandemic on the back of strong US growth. A hard landing would imply dollar strength on safe haven flows.

But in our soft-landing baseline, we could move towards the middle of the smile: weaker US growth and a weaker dollar. Should this occur, it would be a game changer for sentiment towards emerging market local currency debt and we would expect double-digit returns to ensue.

Real rates remain high in emerging markets amid orderly disinflation; many major emerging market central banks hiked rates faster and more aggressively than their developed market counterparts in 2021 and 2022 after the pandemic and cut rates earlier starting in 2023. These rate cuts contributed towards the double-digit returns achieved in 2023. Many emerging market central banks paused through 2024, while others continued to cut but more cautiously, waiting for the US Federal Reserve.

Local currency bonds are also set to benefit from the easing monetary cycles overseen by most developed market central banks, which includes the Fed after September’s 50-basis points cut. The effect of these cycles is indirect, but still powerful.

Emerging market central banks have already been cutting rates since last year but some of them have paused or taken a more cautious approach in 2024. Now that the Fed has started cutting rates, several of them have resumed and may accelerate their own rate cutting cycle.

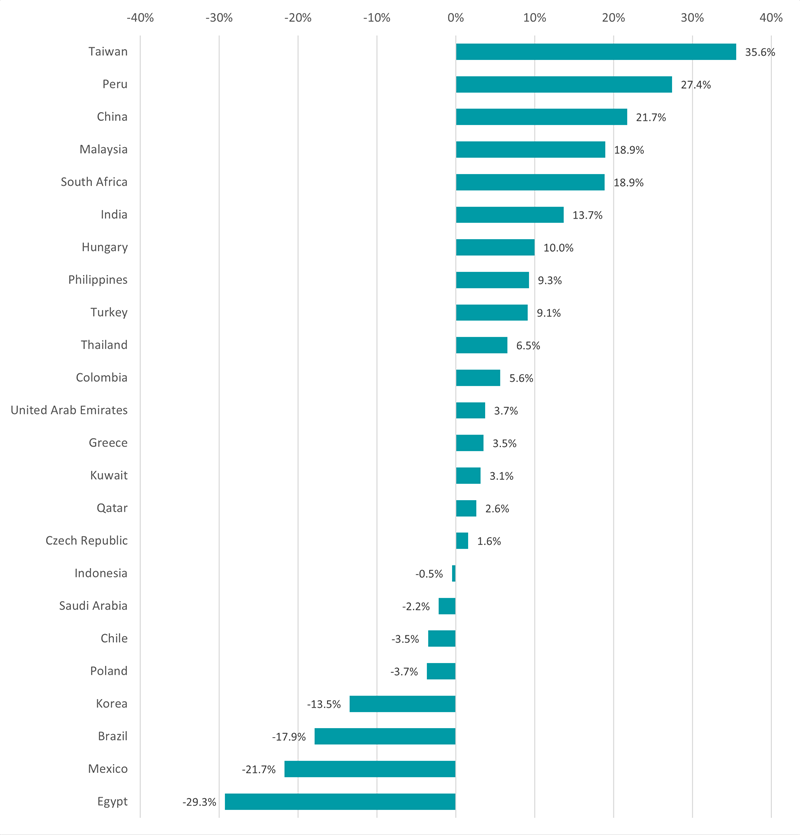

Indonesia’s central bank cut rates on the same day as the Fed, while South Africa, China, Hungary, Czechia, Mexico, Costa Rica, Dominican Republic among others followed suit soon after. Only Brazil bucked the trend with a 25bps hike.

This global easing cycle is likely to boost emerging market local currency bond prices and lower domestic borrowing costs for sovereigns and corporates.

Active investors are likely to find plenty of idiosyncratic opportunities since cycles will be much less synchronized, as not all countries have been equally successful in their fight against inflation.

Carlos de Sousa is an emerging market strategist at Vontobel. The views expressed above should not be taken as investment advice.

Capital gains tax shoots up to 18% and 24% for the basic and higher rates, from 10% and 20% respectively.

Chancellor Rachel Reeves today delivered Labour’s first Budget in 14 years, announcing £40bn of tax rises to rebuild public services and restore the stability of public finances.

The bulk of the tax hikes will fall on the shoulders of businesses, with employer national insurance contributions rising by 1.2 percentage points to 15% by April 2025. National insurance contributions will be payable on salaries over £5,000 rather than the previous threshold of £9,100. However, the Employers Allowance for National Insurance has been increased to £10,500 a year, meaning that many small businesses will be exempt.

These measures should raise £25bn annually by the end of the forecast period, the chancellor said.

Capital gains tax hiked

Capital gains tax (CGT) will increase to 18% from 10% for basic rate taxpayers and to 24% from 20% for those on the higher rate. CGT rates on property sales will remain at 18% and 24%. The UK will still have the lowest CGT of any G7 economy, Reeves said.

CGT on business assets will rise from 10% this year to 14% in 2025-26 and then 18% in 2026-27. The lifetime limit for business asset disposal relief remains £1m.

IHT relief halved for AIM shares

Shares traded on AIM will be subject to a new 20% inheritance tax (IHT) rate.

Amisha Chohan, head of small cap strategy at Quilter Cheviot, said: “While it is disappointing that AIM shares will no longer be fully exempt from inheritance tax, we are pleased the government has seen sense to retain some sort of incentive to help drive the growth of this country’s smaller companies.

“With an effective tax rate of 20%, instead of IHT’s headline rate of 40%, AIM businesses, along with their growth potential, continue to give investors a compelling offer.”

Reeves also announced that the current IHT freeze, which was due to end in 2028, will be extended to 2030.

However, inherited pensions will become subject to inheritance tax from 2027 onwards.

Business and agricultural assets worth less than £1m will not be subject to IHT, enabling small family farms to be passed down to the next generation. Assets worth more than £1m will be granted 50% relief, leading to an effective IHT rate of 20%.

EIS and VCTs extended; ISA allowance frozen

Labour has extended the Enterprise Investment Scheme (EIS) and Venture Capital Trust Scheme to 2035, meaning that investors will continue to access tax relief, including income tax, capital gains tax and the exemption of EIS shares from inheritance tax.

There were no material changes to ISAs in this Budget although the ISA allowance has been frozen until 2030. Since the ISA allowance was last changed in 2017, it has effectively fallen by £6,000 in real terms, said Chris Rudden, head of UK investment consultants at digital wealth manager Moneyfarm.

Furthermore, Reeves has confirmed that the British ISA will not go ahead.

Good news for working people on income taxes and living wage

As part of Labour’s manifesto commitment not to increase taxes on working people, Reeves has not altered income tax, value added tax (VAT) or employees’ national insurance contributions. The current freeze on income tax and national insurance thresholds, which ends in 2028-29, will not be extended. As a result, personal tax thresholds will once be uprated in line with inflation.

The national living wage is set to rise to £12.21 an hour, an increase of roughly 6.7%. In line with this, the government will move towards the introduction of a single adult wage by raising the minimum wage for 18 to 20-year-olds by over 16% to £10 an hour.

Finally, state pensions are set to benefit from the triple lock. In line with updated figures on national wage growth, the new state and basic pensions will be uprated by 4.1%, bringing about £470 into pensioners' pockets next April.

Stability and investment rules introduced

The Budget confirmed plans to make “responsible reforms” to the government’s fiscal framework, to improve certainty, transparency and accountability, by implementing two rules.

The first is the ‘stability rule’, which aims to move the current budget into balance so day-to-day spending is met by revenues. This means the government will only borrow for investment.

Meanwhile, the ‘investment rule’ will reduce net financial debt as a proportion of GDP. This marks a technical change to the way debt is measured: it will take into account not just the debt that government owes but the financial assets that are expected to generate future returns.

The Budget said this rule “keeps debt on a sustainable path while allowing the step change needed in investment”.

Reeves said both of these rules will be met in 2027-28, two years ahead of the previous target of 2029-30.

Analysis by the Office for Budget Responsibility (OBR) predicts that the current deficit will fall from £55.5bn (or 2% of GDP) this year to a surplus of £10.9bn (0.3% of GDP) by 2027-28. It will then narrow to a slightly smaller surplus of £9.9bn in 2029-30.

In her speech, Reeves also listed the latest GDP forecasts from the OBR, which said real GDP growth will be 1.1% in 2024, 2.0% in 2025, 1.8% in 2026, 1.5% in 2027, 1.5% in 2028 and 1.6% in 2029.

The body also expects consumer prices inflation to average 2.5% in 2024 and 2.6% in the following year, then 2.3% in 2026, 2.1% in 2027, 2.1% in 2028 and 2% in 2029.

The self-styled ‘king of debt’ would increase the US’s already exponential deficit and his policies would be inflationary, causing bond yields to soar, fund managers said.

If Donald Trump wins the US election next week, inflation would rise, the budget deficit would increase and the Federal Reserve would probably cut rates at a slower pace than currently expected, fund managers predict.

Nicolas Trindade, who manages the AXA Global Short Duration Bond fund, said a Republican victory would be “very disruptive” for bond markets and would drive treasury yields higher, causing a rapid steeping of the yield curve that “could potentially be really painful for a lot of fixed-income investors”.

Both presidential candidates have made spending pledges that would increase the US government’s deficit, although Trump – who once called himself the ‘king of debt’ – is expected to ramp up borrowing more than Kamala Harris.

FE fundinfo Alpha Manager Trindade believes Trump would extend a series of tax cuts that are due to expire, creating a tailwind for growth but adding inflationary pressure. Tariffs on imports from China, Europe and elsewhere, as well as a clamp down on immigration, would also cause prices to rise in the US.

The scale of Trump’s potential victory would be a critical factor, according to Raphael Olszyna-Marzys, international economist at J. Safra Sarasin Sustainable Asset Management. “A Republican sweep is the worst outcome for bonds,” he said.

“President Trump’s policies with lower taxes, more deregulation, tighter immigration policies and the likely implementation of broad-based tariffs will lead to higher inflation expectations, a significant increase in budget deficits, but also increased policy uncertainty. Markets would likely price a shallower Fed rate cut cycle and a higher term premium to account for the additional uncertainty.”

If Congress is divided, however, Trump would have less leeway to implement his policies and the market reaction would be more muted, Olszyna-Marzys explained.

Global government bonds have been selling off rapidly during the past six weeks – not just in anticipation of a Trump presidency but also in reaction to strong US economic data, said Ashok Bhatia, co-chief investment officer for fixed income at Neuberger Berman.

“Bond yields have surged because, after a weak August, September saw a string of US releases deliver upside surprises, including a blockbuster payrolls report and warmer-than-expected retail sales and inflation,” he explained.

Bhatia thinks “this could be just the beginning of a surprisingly sustained move higher in yields”.

He expects the Fed to cut rates by 0.25% next week and in December, but it could then potentially take a pause during the first quarter of next year. “It is hard to imagine the Fed next year mechanically delivering rate cut after rate cut in the face of 2.5% GDP growth and increasingly stubborn inflation.”

A Fed pause could spark fears of a return to rate hikes and have an outsized impact on the yield curve, the co-CIO said.

“The recent sell-off has taken yields back only to the levels of late July, just before a very weak US payrolls report and the unwind of the yen carry trade created a big bid for bonds. It would not be surprising to see the US five-year yield add another 50 basis points from here, taking us back to the mid-2024 highs.”

Arif Husain, head of fixed income at T. Rowe Price, also expects yields to continue rising. “The 10-year treasury yield will test the 5% threshold in the next six months”, he predicted, up from 4.3% on 29 October.

“Ongoing issuance by the US Treasury to fund the government’s deficit spending is flooding the market with new supply,” Husain explained. “The Federal Reserve’s quantitative tightening has taken a large, reliable buyer of treasuries out of the market, further skewing the balance of supply and demand in favour of higher yields.”

Managers are preparing for this eventuality by shortening duration. David Roberts, co- manager of the Nedgroup Investments Global Strategic Bond fund, has started selling down the US, shortening interest rate exposure. The fund is underweight US bonds and “closer to the election, I may go further – possibly to zero or, whisper it… short”.

In client portfolios where Neuberger Berman has the most freedom, Bhatia and his colleagues have reduced duration to around 3.5 years; just over half the duration of the major investment grade benchmarks.

“Moreover, with US investment grade corporate bond spreads as tight as they have been for almost 20 years, we are also cautious on corporate credit, where a move back to 4.5% in the five-year yield could cause a disorderly exit,” he said.

“Investors who need exposure would be better off looking at structured products such as investment grade collateralised debt obligations or mortgage-backed securities, where spreads still offer a thicker cushion.”

Trindade also expects short-dated bonds to weather the oncoming storm better. He is keeping duration at two years in his AXA Global Short Duration Bond fund, which has a 5% yield, meaning that it could withstand a rise in yields of 250 basis points before posting a negative total return.

“If we see treasury yields rising further, then we'll have plenty of space in the strategy to add duration at better levels,” he continued. About 20% of the portfolio matures each year and in a rising rate environment, the proceeds can be reinvested into bonds with higher yields.

With emerging markets strengthening, Trustnet asks the experts for their favourite funds for this asset class.

Funds managed by Artemis, Lazard and GQG Partners are among those that investors could look to if they think emerging markets are poised for a rebound, fund pickers have said.

As Trustnet examined yesterday, a strong economic backdrop, stimulus in China, attractive valuations and a weaker dollar are some of the reasons why investors are starting to feel more confident in their outlook for emerging markets.

Below, we look at five funds the experts are tipping for investors looking to buy into emerging markets.

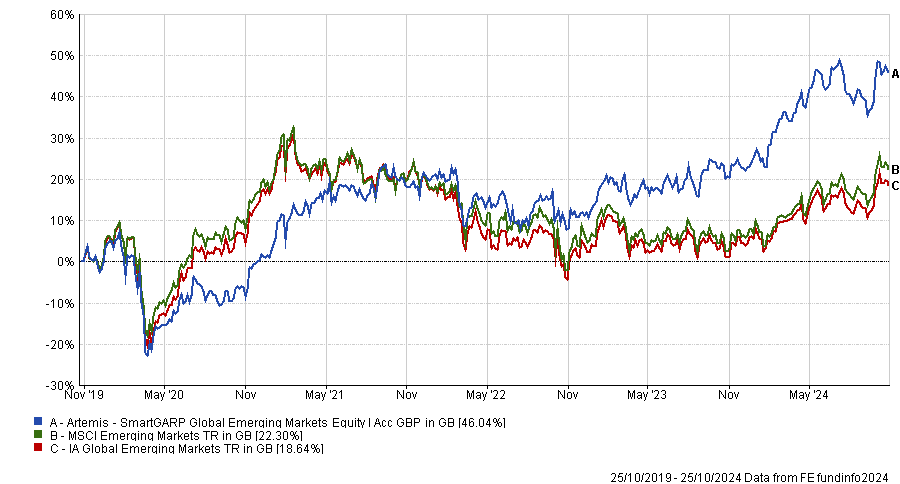

Artemis SmartGARP Global Emerging Markets Equity

We start with FE Investments, where emerging markets fund analyst Tahia Tahmin picked out Raheel Altaf’s £1bn Artemis SmartGARP Global Emerging Markets Equity fund.

She said the approach taken by the £1bn fund is not a conventional one but has proven to be successful with the fund outperforming over one, three and five years, as well as since its launch in 2015.

Performance of Artemis SmartGARP Global Emerging Markets Equity vs sector and index over 5yrs

Source: FE Analytics

“The manager incorporates both a systematic process from his quantitative tool SmartGARP to screen for stocks and eliminate the potential for any behavioural biases, as well as applying a qualitative layer to the process, which allows the manager to factor in top-down risks and carry out sanity-checks on all investment decisions,” Tahmin explained.

In looking for stocks that are growing faster than the market but trading on lower valuations, the fund ends up with a value tilt. Top holdings at present include Taiwan Semiconductor Manufacturing Company (TSMC), Tencent Holdings, Kia Motors and Petróleo Brasileiro.

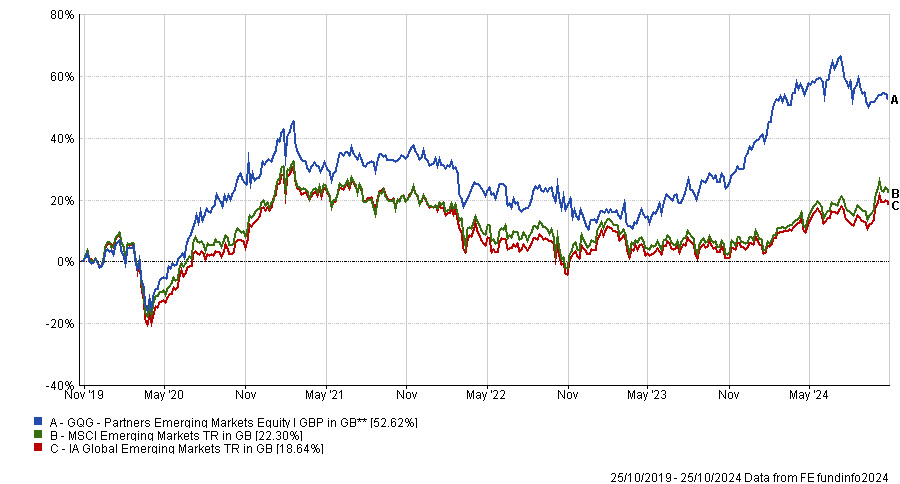

GQG Partners Emerging Markets Equity

Darius McDermott, managing director at FundCalibre, thinks investors need to watch the strength of the US dollar and the impact of China’s stimulus package as both factors will influence the performance of emerging market equities from here.

To cope with this uncertain environment, McDermott highlighted the $3bn GQG Partners Emerging Markets Equity fund. It is run by Rajiv Jain, Brian Kersmanc and Sudarshan Murthy, all of whom hold FE fundinfo Alpha Manager status.

Performance of GQG Partners Emerging Markets Equity vs sector and index over 5yrs

Source: FE Analytics

“This fund benefits from inherent flexibility, allowing it to quickly adapt to market opportunities,” he explained. “Moreover, it is managed by a highly experienced team that has delivered stellar returns for investors since its launch.”

GQG Partners Emerging Markets Equity’s process seeks out companies with attributes such as stable financial and solid balance sheets, profitability, efficiency, sustainable businesses and liquidity, giving it a quality-growth bias. Top holdings include TSMC, Petróleo Brasileiro, TotalEnergies and Adani Enterprises.

Invesco Emerging Markets ex China

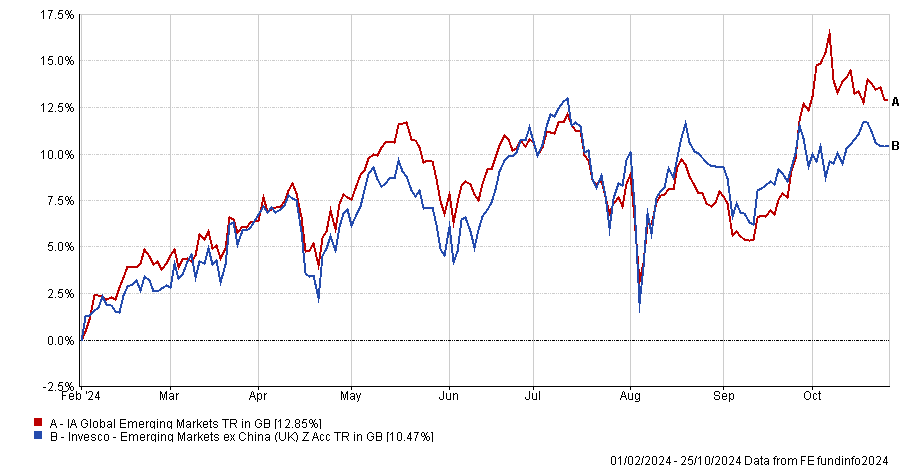

McDermott also suggested the Invesco Emerging Markets ex China fund for investors who want an emerging markets fund without exposure to China. This could be for several reasons, including scepticism about the outlook for China or because they already own a dedicated Chinese equity strategy.

Performance of Invesco Emerging Markets ex China vs sector since launch

Source: FE Analytics

Managed by James McDermottroe and FE Alpha Manager Charles Bond, the £240m fund has a contrarian approach that looks for companies in unloved parts of the market. It’s another fund with TSMC in its top 10, which sits alongside the likes of Samsung, HDFC Bank and Naspers.

“The process adopts a value focus, with returns largely driven from stock selection. It is still relatively early days, but performance since launch has been very promising,” McDermott said.

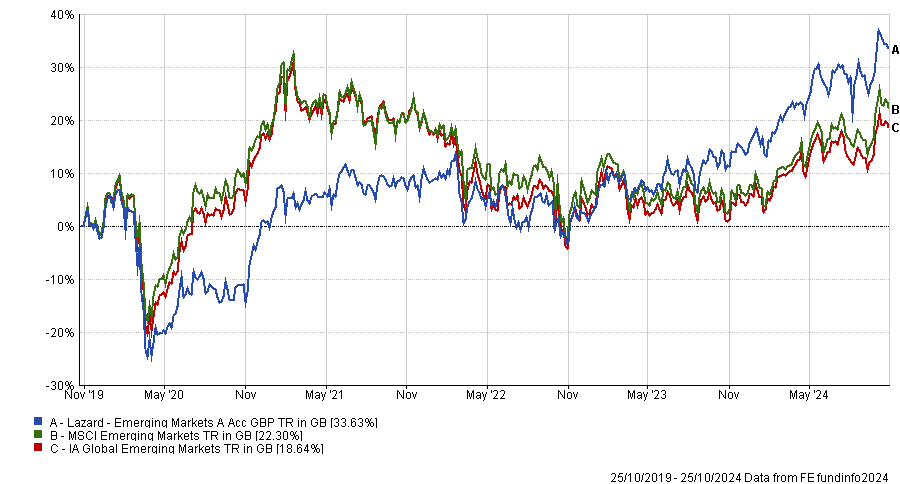

Lazard Emerging Markets

Rob Morgan, chief analyst at Charles Stanley Direct, pointed out that the long-term opportunities of emerging markets are currently offset by high valuations in the Indian market and political and economic uncertainties in China.

“To balance the opportunities and the risks we favour an active approach that combines elements of quality and value to navigate this disparate sector. As such Lazard Emerging Markets is a good fit,” he said.

Performance of Lazard Emerging Markets vs sector and index over 5yrs

Source: FE Analytics

“The fund adopts a patient and strict ‘value’ approach, buying into shares in unloved companies at a significant discount to their true worth. However, James Donald’s philosophy could be better summed up as ‘quality at a discount’.

Morgan said the fund should appeal to those who believe an active manager can add value by prioritising quality and avoiding problem companies or those most adversely impacted by the political or regulatory landscape.

Lazard Emerging Markets’ largest holdings include TSMC, China Construction Bank, Alibaba and Indus Towers.

HC Sephira GEM Long-Only

Simon Evan‑Cook, manager of Downing Fox multi-asset funds, told Trustnet yesterday that active managers he invests with are optimistic about benign economic conditions, good companies and cheap valuations in emerging markets.

One lesser-known fund that Evan-Cook uses to play this space is HC Sephira GEM Long-Only fund, which is managed by Jason Mitra, the founder and chief investment officer of Sephira Investment Advisors.

“He runs a highly active strategy investing in high-quality businesses. He also focuses heavily on risk management of the portfolio, as he is aware that even the highest quality companies in emerging markets can face risks above and beyond those of more established markets,” he added.

“This can result in higher turnover, but we believe this is no bad thing if the manager can demonstrate that trading is adding value above its costs.”

HC Sephira GEM Long-Only uses a bottom-up approach that looks for high-quality, undervalued companies in the overlooked areas of emerging markets. Top holdings include DiDi Global, TSMC, Star Health and Allied Insurance.

Experts discuss if investors have become too short-termist with their investments.

Markets have always moved rather quickly, but for some experts, the biggest challenge facing the market is investors' obsession with short-term results.

Certainly, no stock can rise forever and for investors hoping to make the most of their money, it is crucial to know when to get out to avoid a potential downturn in performance. However, for many experts, making investment decisions on the back of short-term price movements is a dangerous game and is one too many investors have begun to play.

Louise Kernohan, co-manager of the £1.4bn BNY Mellon Global Equity fund, said: “I think often stocks are moving away from fundamentals and valuations and being carried by momentum. I think it is the case that markets have become too fixated on the short term.”