Whisper it quietly but after years of negative sentiment, Chinese equities finally appear to be holding their ground. What could sustain the recovery from here?

As contrarian investors, we believe it often pays to bet against the crowd. Bargains can sometimes be found where there is controversy and when performance has been poor. China has been the world’s unloved market since 2020, with 2023 marking the fourth consecutive year of losses for the Hang Seng Index.

Our positioning in China

Contrarianism is built on the premise that we might go where others do not. Valuations are compelling, and many individual stocks trade on single-digit price-to-earnings multiples and unusually high dividend yields.

Our conviction has grown as short-term uncertainties – while real – have faded in importance relative to the rarity of the long-term opportunity.

We typically look further afield to find our best ideas in parts of the market where others are not looking. But, given the unrelenting sell-off in Chinese markets and January’s additional 10% capitulation, even the well-known names within our benchmark had been ‘for sale’.

Chinese e-commerce leaders Alibaba and JD.com trade on price-to-earnings (P/E) multiples of 8x and 9x, respectively. Baidu, China’s Google, trades on a P/E multiple of under 5x core earnings, after adjustments for cash and investments.

Late last year, we initiated a position in Tencent (a stock we regrettably haven’t owned for most of our history), a high-quality, dominant social entertainment platform that underperformed last year, in line with the China benchmark, despite delivering sequential revenue and earnings growth and its P/E multiple touching 12x P/E at the lower end of its own range.

To use our car analogy for price relative to value, we assessed we were getting a high-quality Ferrari at a bargain price.

China rebounds

Despite a sea of negative sentiment, equities in the world’s second-largest economy have held their ground in recent months. So, what has changed in China’s macro picture to drive up these stock prices?

Perhaps it is the beginning of the unwinding of the negative expectations and relentlessly bearish sentiment that dominated the market earlier this year. The initial rebound may have been triggered by economic data and policy measures that support the ‘less bad’ economic situation.

For example, we have seen a resilient economy which grew faster than expected in the first quarter of 2024 – expanding at an annual pace of 5.3% and beating growth expectations, thanks to strong performances in the industrial and services sectors.

There have also been government-mandated purchases of large-cap stocks by state-owned funds to boost the benchmarks, as well as a pledge of continued support for the economy and new housing policy measures to alleviate the property sector’s drag on the economy and revive the property market.

We are also witnessing a ramp-up in special bond issuance and newly announced ultra-long-dated government bonds. All actions that give us reason to be optimistic.

But momentum is slowing and markets have now entered a vacuum period as investors wait for the government’s upcoming Plenum meeting in July.

The party is expected to roll out measures aimed at boosting consumption and providing further relief to the beleaguered property sector.

A 'head fake' or is this rally sustainable?

Forecasting anything in the short term is a fool’s game. The fundamental bottom of China’s bear market may only come with clear signs of life in the property market. China has been throwing everything at solving its property problem.

Intervention by government and regulators is also beginning to provide a backstop for markets. Most notably, the monetary easing and selective fiscal provision put in place from the end of 2023 have started to take effect and there are signs of sequential improvements of macro data. Growth indicators have exceeded expectations in recent months, bolstered by manufacturing activity and a recovery in exports.

The rally in Chinese stocks has gained momentum, but these equities are still trading at depressed multiples, with near-record large discounts relative to their historical averages, and to their emerging and developed market counterparts.

Attractive valuations may have more appeal if earnings accelerate as consumer and business confidence recovers and growth conditions improve.

Shareholder returns provide a floor

A key factor driving China’s comeback story has been the recent increase in shareholder returns through dividends and buybacks, initially at state-owned enterprises (SOEs) but increasingly at privately-owned companies too.

Not only do these provide strong valuation support, but they also make a compelling case for equity investment in a rate-cut environment.

It’s worth bearing in mind that, while other countries are facing inflation, China is witnessing deflation. This makes equities attractive for domestic investors when compared against low interest rates offered by bank accounts and could provide additional future support for the market.

Listed companies have strong balance sheets and cashflow, even more so for our holdings, and the dividend and buyback is sustainable. So, even if this isn’t the bottom, we are happy owning our companies given the valuations and shareholder returns.

After three years in a bear market, few believe in China, and it remains a consensus underweight. Valuations remain attractive, however, and sustained market moves higher may convince more people to buy and eventually real money will come.

James Cook is head of investment specialists and investment director, emerging markets at Federated Hermes. The views expressed above should not be taken as investment advice.

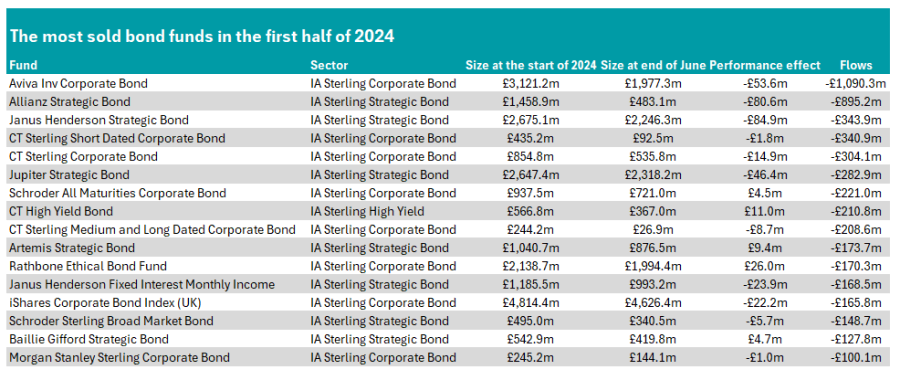

Trustnet begins its half-year flows series with the main UK fixed income sectors.

Investors took more money out UK bond funds than they added during the first half of the year, according to data from FE Analytics.

In all, there were 16 funds focused on fixed income in the IA Sterling Corporate Bond, Strategic Bond or High Yield sectors where investors withdrew more than £100m over the first six months of the year. Conversely, there were just 10 that were bolstered by more than £100m.

The unfortunate fund with the highest withdrawals was Aviva Inv Corporate Bond, where investors took out more than £1bn, the majority of which came in the second quarter of the year.

It has been among the worst funds in the IA Sterling Corporate Bond sector over three, five and 10 years, where it sits in the bottom quartile among its peers, although it climbed to the third quartile over one year. The fund failed the firm’s value assessment earlier this year, with performance cited as the main factor.

The second-most sold fund in the bond space came from the IA Sterling Strategic Bond, where investors have pulled £895m from Allianz Strategic Bond so far in 2024. Again performance has been poor, with the fund in the bottom quartile of the sector over one, three, five and 10 years.

However, much of the outflows may be explained by the announcement in May that manager Mike Riddell is leaving Allianz this month to join rival Fidelity.

Source: FE Analytics

It is a stark drop down to the next fund, where Janus Henderson Strategic Bond sits. Investors pulled £344m from the fund in the first half of the year. There were a trio of funds with outflows of more than £300m, with the other two – CT Sterling Short Dated Corporate Bond and CT Sterling Corporate Bond – both residing in the IA Sterling Corporate Bond sector.

The only constituent of the IA Sterling High Yield sector on the list was the CT High Yield Bond, with investors taking out £211m over the past six months. Columbia Threadneedle dominated the list with four funds out of 16.

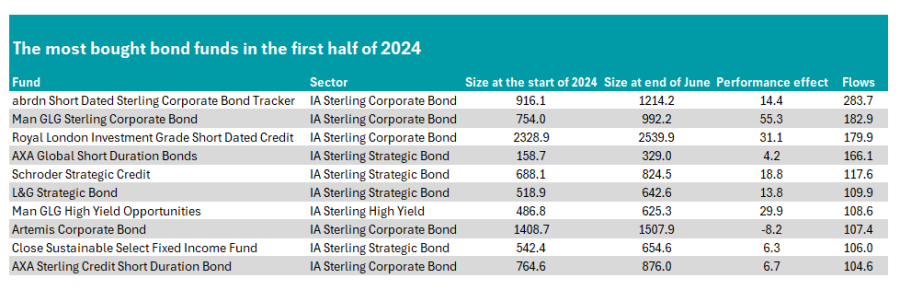

In cheerier news for bond fund managers, there were 10 that achieved inflows of more than £100m, with the most bought being a passive fund.

Abrdn Short Dated Sterling Corporate Bond Tracker took in the most money (£284m) over the first half of 2024, taking its assets under management from £916m to £1.2bn.

This is despite poor performance over the past year, in which the fund sits in the bottom quartile of the IA Sterling Corporate Bond sector. However, it is in the top quartile of its peer group over three years.

Overall inflows were lower than the outflows, however, with no other funds on the list taking in more than £200m.

The next best was FE fundinfo Alpha Manager Jonathan Golan’s Man GLG Sterling Corporate Bond fund, which raked in £183m in new money. The fund has been the best performer in the IA Sterling Corporate Bond sector over the past year.

Royal London Investment Grade Short Dated Credit rounded out the top three, which all came from the IA Sterling Corporate Bond sector. Another top-quartile performer over three years, it also boasts some of the highest returns over five years, despite making a modest 7.4% during this time.

Source: FE Analytics

Man GLG had two entrants on the list, including the only member of the IA Sterling High Yield sector: Man GLG High Yield Opportunities. Managed by Alpha Manager Michael Scott, it has been the best performer in the sector over five years and has been in the top quartile among its peers over one and three years as well.

The other firm with two on the list was AXA, with both the AXA Global Short Duration Bonds and AXA Sterling Credit Short Duration Bond funds taking in more than £100m over the first half of 2024.

Trustnet researches the four active funds in the IA UK All Companies sector with less than £100m in assets under management that charge less than 1%.

Funds with fewer assets under management (AUM) have an edge when investing in small- and mid-caps because they do not face the same liquidity constraints as larger funds.

As a result, they can delve even deeper into the market-cap chain to generate more alpha, taking bigger positions in minnows that would be unachievable with too much money to manage.

However, smaller funds often charge higher fees as they do not have the scale to spread costs across a large pool of investors.

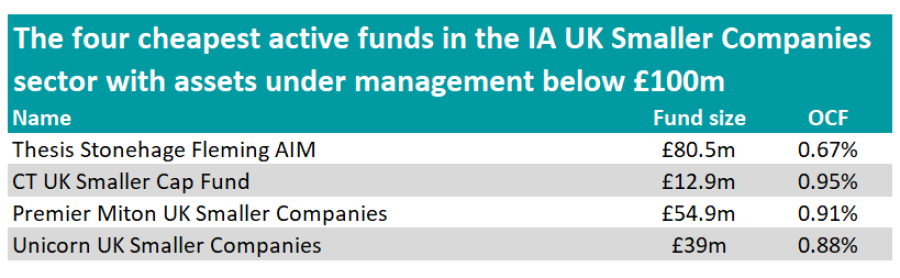

As such, below, Trustnet highlights the four active funds in the IA UK Smaller Companies sector with less than £100m in AUM and charging less than 1%.

Source: FE Analytics

The £80.5m Thesis Stonehage Fleming AIM, managed by Paul Mumford and Nick Burchett, is the cheapest ‘sub-scale’ fund in the sector, with an ongoing charge figure (OCF) of 0.67%.

The fund invests in shares listed on the UK Alternative Investment Market (AIM), although its mandate allows it to hold names that have been transferred to the main market as long as they only form a small portion of the overall portfolio.

It is the second-best performing fund over the past 10 years in the IA UK Smaller Companies sector. However, this outperformance has come with higher volatility, making it one of the 10 most volatile funds over the same period.

Performance of funds over 10yrs vs sector

Source: FE Analytics

Furthermore, Thesis Stonehage Fleming AIM is one of the three most consistent UK small-cap funds, as it has outperformed the Numis Smaller Companies (Excluding Investment Trusts) index more regularly than most of its peers.

The £12.9m CT UK Smaller Cap Fund is the smallest fund on the list, but also the most expensive, with an Ongoing Charge Figure (OCF) of 0.95%.

Managers Catherine Stanley and Patrick Newens focus on companies displaying above-average growth rates or growth potential relative to the Numis Smaller Companies (excluding Investment Trusts) index. Indicators such as earnings and sales growth are used to assess the growth potential of a stock.

CT UK Smaller Cap Fund sits in the second quartile of the IA UK Smaller Companies sector over 10 years but has been one of the least volatile funds during that period.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

Trustnet recently identified Stanley as one of the few ‘veteran’ managers in the IA UK Smaller Companies sector still producing top returns.

The £54.9m Premier Miton UK Smaller Companies also made the list. It charges investors 0.91% and is managed by Gervais Williams and Martin Turner, who aim to identify companies with information gaps and significant potential for mispricing and returns.

The fund focuses on small- and micro-caps, with 68.4% of the holdings indexed on the FTSE AIM, 8.2% on the FTSE Small Cap, and 6.4% on the FTSE 250, while 7.2% are unindexed.

In terms of performance, the fund sits in the bottom quartile of the IA UK Smaller Companies sector over 10 years, as most of the returns achieved during that period were eroded from the second half of 2021 onwards.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

At the beginning of the year, Williams shared his view that UK equities within sectors such as insurance, financial, manufacturing, defence and commodity have become “exciting again”, if inflation persists.

Finally, the £39m Unicorn UK Smaller Companies, managed by Simon Moon and Fraser Mackersie, charges 0.88%.

Although the managers do not base their portfolio construction on macroeconomic views, the fund shows a preference for the engineering and financial services sectors, which make up 19.9% and 17.5% of the portfolio, respectively. In contrast, the fund has no exposure to the oil and gas, mining, and biotechnology sectors.

It sits in the second quartile of the IA UK Smaller Companies sector over 10 years, but has made top-quartile returns over more recent periods. It has also been more volatile than its sector peers, ranking 24th out of 40 in terms of volatility.

Performance of funds over 10yrs vs sector

Source: FE Analytics

The managers recently bought shares in the UK technology firm Raspberry Pi, which listed last month. They believe that various industries will increasingly adopt the company’s single-board computer.

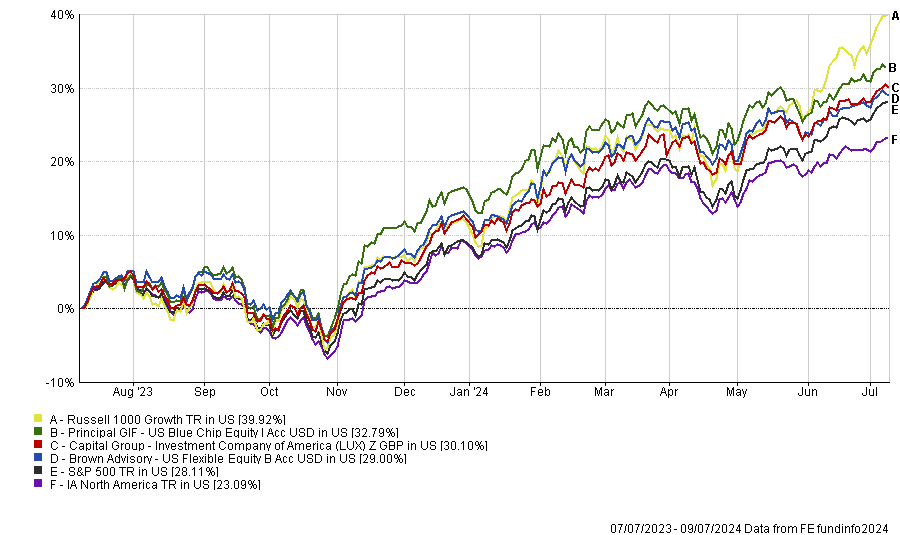

Having no or low exposure to Nvidia was a significant headwind over the past year but three funds still delivered top-quartile returns without loading up on the chip designer’s shares.

US equity managers have been rewarded lately for sticking closely to their benchmark’s largest stocks, whether their investment process mandates a small tracking error or high conviction, focussed bets.

Across the board, most US equity funds’ top 10 holdings read like a roll call of tech giants, with some combination of Nvidia, Microsoft, Meta, Amazon and Alphabet in there, and sometimes all five.

Nvidia has been the star performer and all but three funds in the IA North America sector with top-quartile returns over the past 12 months count it amongst their largest 10 positions.

For the three outliers – Brown Advisory US Flexible Equity, Capital Group Investment Company of America and Principal GIF US Blue Chip Equity – having low or no exposure to Nvidia was a headwind to relative performance, for which they had to compensate with superior stock-picking elsewhere.

This they managed, with all three funds outperforming the S&P 500 over the past 12 months, against which Brown Advisory and Capital Group are benchmarked. Principal US Blue Chip Equity is benchmarked against the Russell 1000 Growth, however, which it lagged.

Performance of funds vs benchmarks and sector over 1yr in dollars

Source: FE Analytics

The funds made up ground by owning other ‘Magnificent Seven’ names amongst their top 10 positions. All three funds hold Microsoft, Amazon and Alphabet. Brown Advisory and Capital Group own Meta Platforms while Capital Group also has Apple.

Other technology companies loomed large. Maneesh Bajaj at Brown Advisory has a stake in Taiwan Semiconductor Manufacturing Co., Capital Group holds Broadcom and Principal owns Intuit, a financial software provider.

The funds have exposure to beneficiaries of artificial intelligence and technological innovation themes in other sectors as well, through Mastercard, Visa and Netflix. All three funds own Mastercard while Principal holds the other two stocks.

Two of the funds own defence and aerospace manufacturing companies, which have soared on the back of rising geopolitical tension and defence spending. Capital Group holds General Electric and RTX Corp. (formerly Raytheon Technologies), while Principal has TransDigm Group.

Financial services also feature. Thomas Rozycki and K. William Nolin at Principal Global Investors own the insurer Progressive Corp. and the Canadian investment group, Brookfield Corporation. Bajaj holds Warren Buffett’s Berkshire Hathaway and private equity firm KKR.

The only healthcare stock amongst the three funds’ top 10 holdings was medical insurer UnitedHealth, which Brown Advisory’s $781m fund owns.

Meanwhile, Capital Group’s $449m fund has exposure to travel and leisure with Royal Caribbean Cruises.

Despite not piling into Nvidia, these three funds’ performance was still closely correlated to their respective benchmarks, with at least a 0.95 correlation.

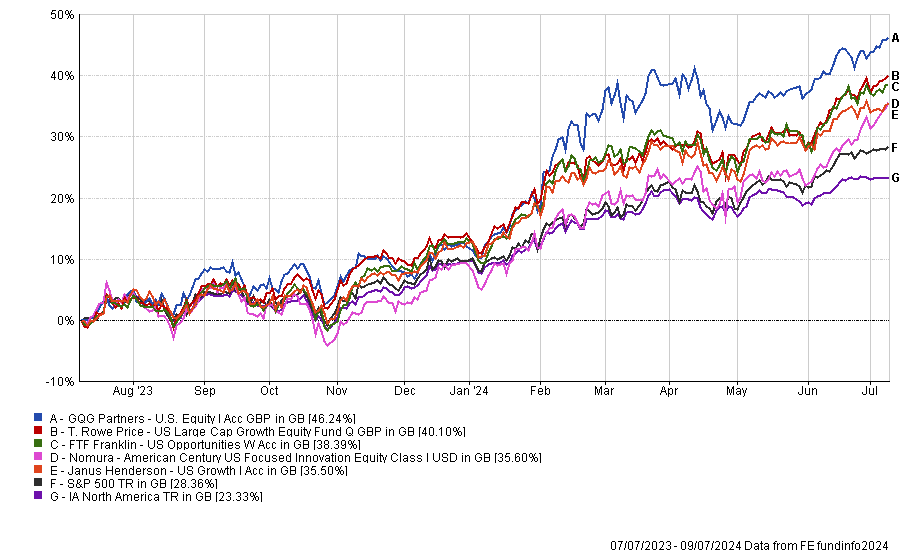

For investors with passive exposure to the US stock market who want to use active stock pickers for diversification: GQG Partners US Equity had the lowest correlation to the S&P 500 amongst all the funds with top-quartile one-year returns, despite Nvidia being its largest holding. Its correlation to the benchmark was 0.74 during the year to 9 July 2024.

GQG Partners U.S. Equity is managed by three FE fundinfo Alpha Managers, Rajiv Jain, Brian Kersmanc and Sudarshan Murthy. The $1.6bn fund’s largest positions include Eli Lilly and Novo Nordisk, which dominate the diabetes and weight loss drugs market, alongside a clutch of tech stocks: Nvidia, Meta Platforms, Microsoft, Amazon, Broadcom, Uber Technologies and the less well-known app developer AppLovin Corp. It also owns Visa.

Performance of funds vs S&P 500 and sector over 1yr

Source: FE Analytics

Close by, T. Rowe Price US Large Cap Growth Equity had a 0.75 correlation, while three top-quartile funds had a 0.77 correlation to the S&P 500: FTF Franklin US Opportunities, Janus Henderson US Growth, Nomura American Century US Focused Innovation.

FE fundinfo Alpha Manager Brian Kersmanc explains why his kids’ college education savings are invested in his funds.

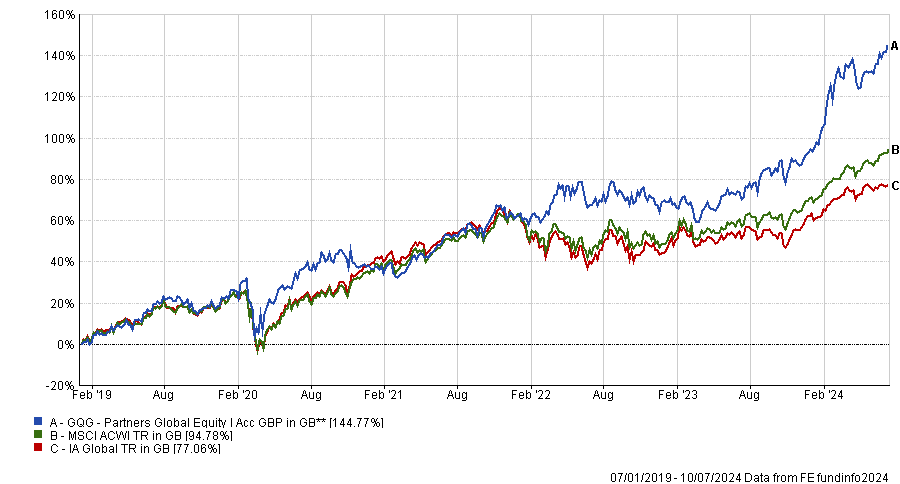

There has been no shortage of crises since the beginning of the decade, with the world grappling with a pandemic, wars in Ukraine and the Middle East, and a resurgence of inflation. While many global equity funds have struggled amidst these paradigm shifts, GQG Partners Global Equity has managed to navigate through the storm relatively unscathed.

The fund is the sixth best performer in the IA Global sector over three years and has not experienced losses in any calendar year since its launch in 2019.

Performance of funds since launch vs sector and benchmark

Source: FE Analytics

Below, FE fundinfo Alpha Manager Brian Kersmanc discusses how the quality of a stock can fluctuate wildly over time and why his portfolio is like a football team.

Could you explain your investment process?

We want to compound capital over the course of time and we want to do it with less risk.

We're more focused on the absolute return and expect 200 to 300 basis points of relative outperformance on an annualised basis over the full market cycle.

Our philosophy is built on three main pillars: a long-term focus, quality bias and capital preservation.

We won’t add any name to the portfolio if we do not have a five-year view on it. That being said, we move the portfolio pretty aggressively at times.

How do you reconcile long-term focus and aggressive turnover?

We try to have the optimal version of the portfolio based on the five-year outlook that we see today. The more the information flow changes over the course of time, the more we adjust and adapt the portfolio.

The analogy I like to use is a sports team. You put the players on the field that you think are going to execute well over the next few quarters.

As the game progresses, players perform differently than you expected, some get injured or tired, the other team makes unexpected moves, the weather changes, etc. You're going to adjust based on those factors.

And just because I put a player on the bench doesn't mean my five-year view of that player is necessarily shattered. It may just not be the optimal time to have that player on the field right now. We substitute our players in and out, which allows us to keep the portfolio as optimal as we can over the course of time.

What is your definition of quality?

Plenty of managers invest for the long run in high-quality names. Where we tend to be different is that we're very open-minded about where quality can come from. We believe quality ebbs and flows over time, so we don't screen out any particular area. Instead, we try to identify where quality is emerging.

For example, if I had asked a room full of people whether Exxon Mobil was a high-quality business two years ago, I might have seen only one hand in the air out of 30. Most people would have said: ‘It’s a commodity business that pumps oil out of the ground, has no differentiation and is subject to the economic sensitivity of oil prices, so it’s a low-quality business.’

But if I had asked the same question 10, 20 or 30 years ago, 29 out of 30 people would have raised their hands, saying: ‘Absolutely, it’s a blue-chip stock, the highest market-cap company in the entire world, with the ability to compound through cycles.’

Why was it considered high quality then? Why was it not considered high quality over the past couple of years? Are the elements in place for this to be a high quality execution story going forward?

We apply this approach across the board to identify where quality is deteriorating, where quality is improving and where the gap in perception between the two of those things is.

Why should investors have your fund in their portfolios?

We have a firm belief in client alignment. At GQG Partners, we have a policy that forbids us from having personal trading accounts. We are only allowed to invest in either GQG strategies or broad-based indexes. Half of my own personal savings are invested alongside our clients.

The reason I bring this up is that both performance and risk management matter to us. If the market goes down 15% and we're only down 10%, I'm still going to have a conversation with my wife at home as she would rightly ask, ‘Brian, why did you lose 10% of our kids' college education savings last year?’

Also, we are the only industry in the world where clients can get average for free. I can't buy an average car or an average mobile phone for free, but if I want an average investment product, I can buy an index tracker for almost nothing. Therefore, there is no reason for us to exist if we don’t deliver outperformance.

Is there anything the market is underestimating?

The market is hyper focused on the US Federal Reserve and the trajectory of interest rates. If the Fed lowers rates, it probably means it is seeing a significant deceleration in economic outlook. We would have bigger problems and I don't know if it's necessarily a good thing.

An underappreciated element of higher rates is that higher cost of capital creates a higher barrier to entry, favouring mega-cap companies.

What do you do outside of fund management?

If you have a passion for something, you end up devoting most of your time in that particular area. So, investment is what I devote a lot of my time and energy toward. When my wife watches the TV, I'll be reading annual reports next to her because that’s what makes me tick.

Gold has quietly ticked to new highs in the past few months.

In an era of higher interest rates, it makes no logical sense for gold to perform well. After all, why own an asset that offers no return (other than speculative capital gains) when you can make circa 5% in a bank account?

Yet gold may well have been a saviour for some portfolios over the past few years, with the precious metal quietly on an incredibly strong run.

Since 2021, when the S&P GSCI Gold Spot price index slipped back 3.4%, it has tracked consistently higher, gaining 11.8% in 2022, 6.5% and so far this year it has enjoyed its biggest rise, up 15.2% (in sterling terms).

Gold has sparkled thanks to its place as a safe haven. With plenty of election uncertainty in 2024, as well as geopolitical instability, wars and economic jitters, there are many reasons why investors might be looking to be more defensive.

Perhaps Labour’s victory – heralded as a positive for the UK after years of dysfunctional Conservative rule – may also have been good for the metal. As one expert explained this week, change can be scary, and a new government can often be a boost for the gold price. Gold rallied after Tony Blair was elected in 1997 too.

Gold is also a direct play on the US dollar, which shot higher versus the pound during former prime minister Liz Truss’ ill-fated administration in September 2022, but has softened around 17% since.

For these reasons, gold set its third consecutive quarter-average record at £1,853 and also set new month- and quarter-end highs at £1,845 on the last day of June.

So can the yellow metal continue its unheralded move higher?

Data from BullionVault earlier this month suggests that fresh highs last month did nothing to dissuade investors, who continue to hold the precious metal despite its price.

Demand was particularly positive in France in the lead up to the country’s general election, when fears of Marine Le Pen and the far right movement gaining a majority were high.

The number of first-time bullion buyers in Europe's third largest economy also set its highest quarterly total in three years amid the political upheaval of the snap election called by president Macron.

This did not happen, but the lack of a majority for either side could cause big blockages in the government. Even so, the fractious parliament represents uncertainty, which should be to gold’s benefit.

Adrian Ash, director of research at BullionVault, said earlier this month: “After finishing the first half of 2024 at new quarterly records, the price of gold looks set to continue its underlying uptrend as the UK and US follow France to the polls. Political uncertainty is adding to gold's appeal as investment insurance. Longer term, the fiscal and monetary backdrop is supportive for gold prices too.”

With the US election still to come – and plenty of question marks over issues such as president Joe Biden’s health and former president Donald Trump’s resurgence – gold may continue ticking higher for the next few months at least.

The firm has introduced both passive and blended options for investors.

Premier Miton has launched its managed portfolio service (MPS), to be led by Ian Rees, head of the multi-manager team. The service will offer two actively managed portfolio ranges – Index and Blend – with target OCFs of 0.25% and 0.45% respectively.

Four portfolios each will be available as part of the Index and Blend funds, which are expected to go live across several investment platforms this year.

The Premier Miton Liberation fund, which currently holds £87.9m in assets, will be included as “core part” of each fund in the Blend range. This will give investors access to more specialised investments not usually available through an MPS, the firm said.

The Index range will be a made up of trackers selected by the Premier Miton team, while the Blend portfolio will use both active and passive strategies.

Jonathan Wilcocks, global head of distribution at Premier Miton said the launch of the MPS range was due to an “increasing demand from advisors” for “cost-effective investment solutions”.

Experts highlight which investment companies should benefit from Labour’s efforts to build homes, reform planning laws, boost the renewable energy sector and stimulate economic growth.

Chancellor Rachel Reeves has barely been in office a week but has already announced planning reforms to “get Britain building again”.

In her first speech as chancellor, she promised to restore mandatory local housing targets, end the ban on building new onshore wind farms in England and prioritise energy projects within the planning system.

Hassan Raza, investment manager of Capital Gearing Trust, said genuine planning reform could provide “real tailwinds to a range of property, private equity and infrastructure trusts”.

Below, fund selectors highlight which investment trusts stand to benefit from the Labour government’s policies.

Housebuilding, property and construction

Labour promised in its manifesto to build 1.5 million new homes during the next five years and is establishing a housing task force to tackle stalled, large housing schemes. The new government also wants to release ‘grey belt’ areas of ugly but protected land.

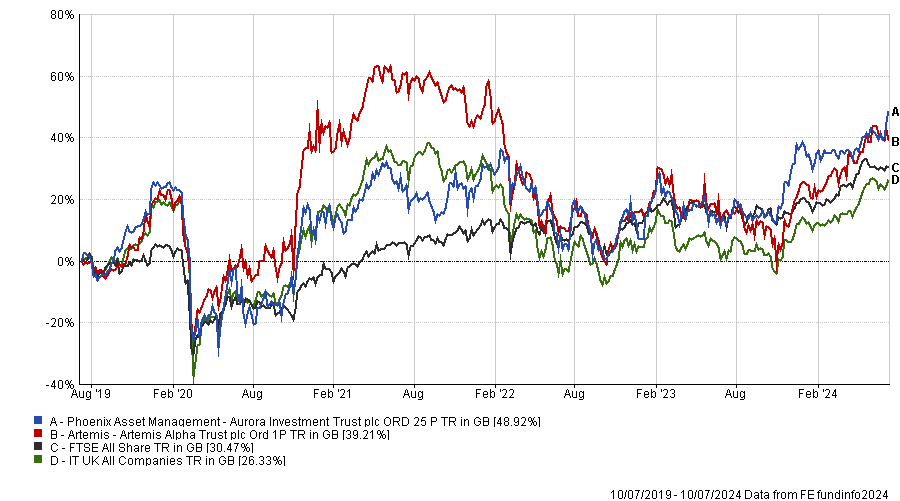

All this bodes well for housebuilders and trusts that own them, such as Aurora Investment Trust, which holds Barratt and Bellway. Managed by Phoenix Asset Management Partners’ chief investment officer, Gary Channon, the trust has a concentrated portfolio of 12 to 20 investments.

Peter Hewitt, who manages the CT Global Managed Portfolio Trust, described Aurora as “a real play on domestic UK”. It has a £189m market capitalisation and an 8.1% discount.

The Artemis Alpha Trust holds several of the same stocks as Aurora and has about 15% in housebuilders, including Redrow and Barratt. Managed by Kartik Kumar and John Dodd, it is trading on a 12.5% discount and has a £123m market cap.

Performance of trusts vs sector and benchmark over 5yrs

Source: FE Analytics

For a purer punt on real estate, Hewitt suggested TR Property. Marcus Phayre-Mudge, a partner at Thames River Capital, has managed the £1.1bn trust since 2011. Most of its assets are in continental Europe, but it still has substantial domestic exposure with 35.7% in listed UK property companies and 6.3% in UK bricks and mortar. Shares sit on an 8.7% discount.

Wind power

Greencoat UK Wind, which owns and operates UK wind farms, is in pole position as Reeves ends the ban on onshore wind farms. Not only will more wind farms be built, but Hewitt expects the value of the trust’s existing assets to rise. He anticipates interest from potential acquirers now that the sector has a “clearer road ahead” and the government is making “positive noises”. The £3.2bn trust is trading on a 13% discount, which has been as wide as 20%.

The lifting of the onshore wind farm ban could prove to be a double-edged sword, warned Juliet Schooling Latter, research director at Chelsea Financial Services.

“Whilst it will likely create more opportunities, increased renewable energy generation means lower long-term power prices that will also be more volatile. We've sometimes seen power prices go negative when it's particularly windy or sunny, which is actually bad for renewables,” she said.

Performance of trust vs sector over 5yrs

Source: FE Analytics

Clean energy

Labour wants to make Britain a clean energy superpower and its ambitions stretch far beyond wind power. Raza expects GB Energy and the National Wealth Fund to “play a critical role in mobilising existing technologies (solar, wind and biomass) and commercialising new ones (hydrogen and carbon capture).”

This should improve conditions for the disposal and development pipelines of trusts such as the NextEnergy Solar Fund and JLEN Environmental Assets, he said.

Labour's renewable push will also require more battery infrastructure to stabilise the grid, which could help some of the battery trusts which have been “massively out of favour”, Schooling Latter said.

Peter Walls, manager of the Unicorn Mastertrust fund, agreed. “More intrepid investors may want to look at the battery storage trusts, although prices here are expected to remain volatile, with greater sensitivity to energy prices and uncertainty about the National Grid.”

Meanwhile, Raza believes that investment in the national grid and broader infrastructure to support electrification should provide a boost for trusts such as International Public Partnerships.

Infrastructure

Many infrastructure investment trusts are trading on wide discounts due to higher interest rates and borrowing costs but some of this pressure will ease as and when the Bank of England cuts rates.

Labour’s reforms are a further tailwind, including the creation of a £7.3bn National Wealth Fund to invest in ports, gigafactories and steel.

Walls said: “While UK interest rates may well stay higher for longer, the direction of travel is downwards and this combined with the Labour party’s stated policies, increases the attractions of trusts such as HICL Infrastructure and Pantheon Infrastructure, which trade at wide discount to net asset value.”

Performance of trusts since Pantheon’s inception

Source: FE Analytics

James Carthew, head of investment companies at QuotedData, highlighted Downing Renewables & Infrastructure Trust (on a 34% discount) and Pantheon Infrastructure (on a 28% discount).

UK equities

Prime minister Keir Starmer has declared it his mission to “kickstart UK growth” and comes to power at a time when UK equity valuations are compelling, despite strong performance in recent months.

Small-caps are the cheapest part of the market, after a rough few years, said Walls, highlighting Aberforth Smaller Companies and Henderson Smaller Companies as good options.

Carthew also pointed to “big bargains” and wide discounts in the UK Smaller Companies sector, naming Montanaro UK Smaller Companies (on a 14% discount), Rights & Issues (13%) and BlackRock Throgmorton (10%).

Moving from listed small-caps to private equity, Hewitt tipped Literacy Capital, which is managed by the father and son team, Paul and Richard Pindar. They invest in small, privately-owned UK companies such as housebuilder Antler Homes and recruiter Kernal, often enabling the founders to partially cash out, and they professionalise how these businesses are run.

Performance of trust vs sector since inception

Source: FE Analytics

The £304m trust has already performed well and will prosper if the UK economy picks up, Hewitt said. It donates 0.9% of its net asset value every year to help disadvantaged children learn to read.

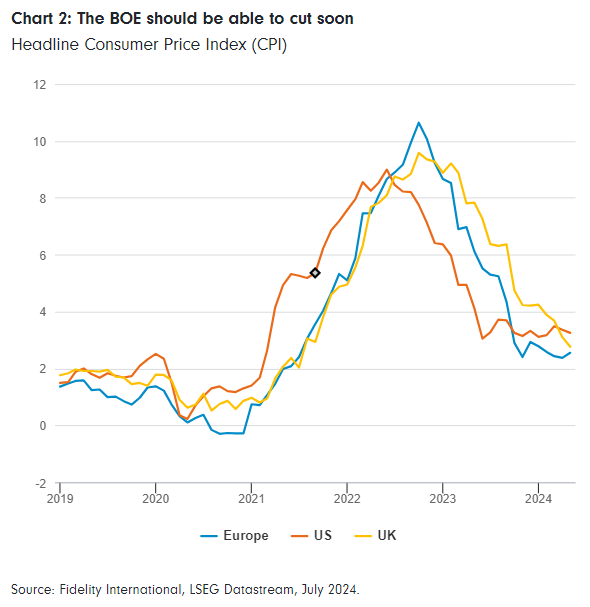

The Republican candidate’s inflationary tax plans could forestall rate cuts.

With the mental acuity of current US president Joe Biden under scrutiny, bond markets have begun to price in a victory for former president Donald Trump in the upcoming election, according to AJ Bell investment director Russ Mould.

If successful, Trump would become only the second president in US history to win a second term having previously been ousted from office, following in the footsteps of Grover Cleveland.

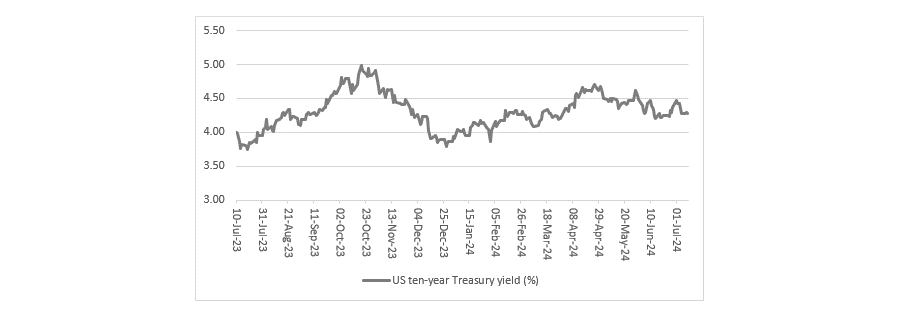

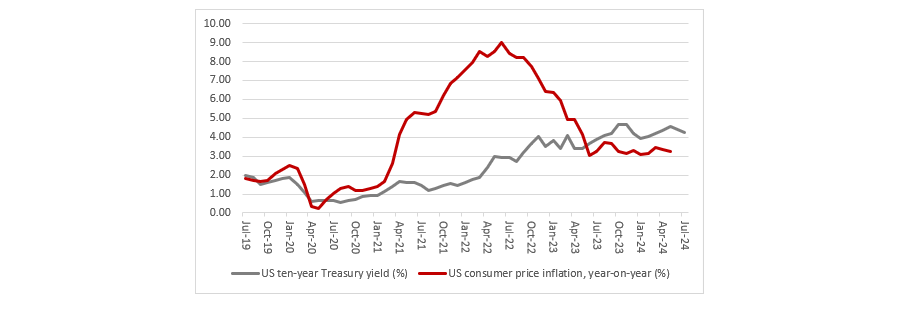

“This can be seen most clearly in how the US 10-year Treasury yield responded to the presidential debate hosted by CNN late last month. The benchmark US government bond saw prices fall and yields rise sharply in response to the broadcast, as fixed income investors began to anticipate a Trump win and the inflation they feared that would bring,” said Mould.

Not all agreed, however. Algernon Percy, managing director of Waverton Investment Management, noted that 10-year US Treasury yields have been “fairly static” over the past quarter, moving between a low of 4.2% and a high of 4.7%, before settling at 4.4% at the end of June.

US 10-year Treasury yields over 12 months

Source: AJ Bell, LSEG Datastream

“This reflected the ebb and flow of sentiment regarding US economic growth and inflation – with the most recent data indicating a gradually slowing US economy that is broadly helpful to a benign inflation outlook, notwithstanding somewhat sticky services inflation and wage growth,” he said.

However, Percy admitted that “short-term noise” around “economic statistics and political shenanigans” could impact yields in the coming months.

On Trump, Mould said some of the former president’s main policies are likely to be inflationary. An extension of 2017’s tax cuts and promises of more to come, for example, should boost consumer spending, which would increase the demand side of the supply-demand dynamic and keep prices high.

This would also run up the US’ already large annual deficit, adding 6% per year to a figure that already stands above 100% of GDP.

“The situation would look even worse, if a soft (or hard) economic landing were to transpire and tax income recedes just as welfare payments rise, as it seems logical to assume that the annual deficit would balloon,” said Mould.

Second, more tariffs on imported goods – not just from China – will hike prices. Lastly, reducing immigration would limit the pool of workers available, with wages likely to rise as a result.

But Mould noted that Biden is “not promising hair-shirt austerity” either. Indeed, if the incumbent president wins, in his first term the US is expected to “rack up” an additional $7trn in borrowing.

This all comes at a time when US Federal Reserve chair Jay Powell is “dangling the carrot” of interest rate cuts, providing inflation continues to cool, Mould said.

This presents a dilemma. On the one hand, investors may want to lock in yields if the Fed does indeed start to cut in the Autumn of this year, as some expect. On the other, although yields are currently above inflation, as the chart below shows, any spike in prices would soon erode this return.

US 10-year Treasury yields vs inflation over 5yrs

Source: AJ Bell, LSEG Datastream

As such, bond investors need to ask themselves what an appropriate level for US 10-year yields might be. “The base case is the 2% inflation target. An investor may then wish to add some term premium to that, since the headline rate is stuck near 3%, thanks to strong services inflation,” he said.

“Then there remains the incipient inflation risk offered by both presidential candidates. And then there is America’s massive deficit which could both pressure the Fed to cut rates to keep the Federal interest bill manageable (since it is now running at $1trn a year) and oblige the US to offer tempting yields so it can find buyers for its newly issued debt.”

All of this implies 10-year Treasury yields are likely to stay above 4% for the foreseeable future, suggesting capital appreciation on these bonds (currently paying 4.28%) could be limited.

“Investors must then decide whether the coupon is enough to compensate for inflation risk, if US Treasuries are to form a part of a balanced, diversified portfolio,” concluded Mould.

The new fund highlights a growing appetite for emerging market funds among investors.

Stewart Investors has launched the Global Emerging Markets (ex-China) Leaders Sustainability fund to be helmed by fund manager Jack Nelson. The portfolio identifies 25-45 mid-to-large-cap companies outside mainland China, contributing to a more sustainable future for emerging markets.

The fund has been launched to work alongside a dedicated Chinese funds, which have proven popular among investors in recent years, the firm said. Most emerging market funds invest heavily in China, meaning people who own both are likely to be double dipping into the region.

However, the fund should also appeal to investors who have concerns over investment risk in Chinese markets.

It joins Stewart Investor’s range of sustainability funds, including the Asia Pacific Leaders Sustainability Fund, which holds £6.7bn in assets under management.

Nelson said there was a “real opportunity in the years ahead” for sustainable investors to make strong returns in the region. “Emerging markets are a melting pot for forward-thinking and innovative companies contributing positively to sustainable development,” he said.

British companies have a reputation for being tenacious and innovative, and their valuations are currently compelling.

With a newly minted prime minister and government, the UK has been under the spotlight this past week. But how does Blighty stack up from an investment perspective?

Elections aside, there has been a slew of negative news about the UK recently, further hitting investor confidence, which hasn’t picked up much since Brexit in 2016. In that time, the UK has dwindled to become the world’s fifth-largest stock market, its $3.5trn dwarfed in comparison to the US at $54.7trn and coming behind China, Japan and India. And will it shrink further? Maybe.

The exodus

Coutts, the Queen’s banker, recently announced it is slashing its UK exposure in its investment portfolios from 40% to a meagre 3.5% in some cases. The drop in confidence of institutional investors will likely creep to others and trickle down to private investors too.

And we have seen a plethora of de-listings in recent years, UK companies fleeing the London Stock Exchange (LSE) to list in other, what they see as more profitable shores. One of the biggest delisting stories was Cambridge-based ARM Holdings, a microchip manufacturer, which left London for New York in March 2023. Another is Paddy Power’s owner Flutter, which will follow ARM this summer.

AIM has also seen a sharp increase in de-listings, with 70 companies either moving to private ownership or relisting elsewhere – the LSE is on track to lose 30 or more £100m-plus companies this year alone. And rumour has it the NASDAQ is on the hunt to lure more firms from the beleaguered FTSE to New York.

Poor economic data

Economic news for the UK isn’t the best either. The Organisation for Economic Co-operation and Development recently downgraded its British growth forecast from 0.7% to 0.4%, making the UK the worst performer in the G7.

The International Monetary Fund (IMF) has also recently released a report telling the UK government it faces a £30bn funding gap that can’t be filled with higher growth or extra borrowing. A blow for the new chancellor.

Is it all bad?

So far, so depressing. But investors would do well to remember that it’s not all doom and gloom and to look beyond the headlines. The FTSE 100 is at an all-time high and still trading at attractive valuations.

It is also a misnomer to think that a bleak economic outlook for the UK is reflected in the stock market. This is certainly not the case for the FTSE 100, where up to 80% of its earnings come from overseas. More than two thirds of FTSE All Share revenues come from overseas and upwards of 50% for the FTSE 250, the oft-touted ‘domestic bellwether’.

Don’t confuse the stock market with the economy

Given the international earnings nature of the FTSE, it’s important not to confuse the stock market with the economy. Many UK smaller companies are international businesses, which are plugged into long-term structural growth trends, but they’re being valued as if they’re linked to the UK economy, or as if they’re in structural decline.

This is largely to do with valuations and investor perception. Market participants have long suggested that UK public limited companies (PLCs) deserve a lower valuation rating compared with international peers, specifically the US. This is usually due to investors pointing to profitability ratios such as return on equity and return on invested capital lagging behind the US, as well as our companies being prone to higher levels of cyclicality.

Valuations are attractive, especially in 'smid'-caps

Like-for-like valuation comparisons (Unilever versus Proctor & Gamble or Shell versus ExxonMobil, for example) show that UK companies tend to trade at a discount to international peers – those with near identical business models, cash flow profiles and end markets.

Then there are other points of reference, such as investment trust discounts, which in October 2023 reached levels that had last been witnessed in 2008, although they have since recovered a bit from the lows.

When you look beneath the surface at our small and medium-sized companies, you will find that valuations have reached extreme lows.

As at 31 October, the Numis Smaller Companies index was trading at a Shiller price-to-earnings (P/E) ratio of 13x. This is close to its all-time troughs, seen on three occasions: the great financial crisis, the tech bubble aftermath and the early 1990s recession. After these troughs, smaller companies went on to produce significant returns over many years.

Of course, ‘smid’-cap investing doesn’t come without risks (it tends to be significantly riskier than investing in larger companies) but it can have an important role to play in a diversified, well-balanced portfolio and we think there is currently an opportunity to buy UK equities at attractive prices.

Innovation isn’t just in tech

Another important point for investors to remember is that innovation comes in many forms and not just US technological disruption. This might provide some comfort to investors who are worrying they have missed out on the Magnificent Seven boom.

Longevity is a good signal of innovation – you need to stay innovative to succeed as a business. And there are some FTSE businesses that have been around for a long time.

Diageo, which owns the best-selling whisky and vodka brands in the world, has been adapting to consumer tastes for hundreds of years. And RELX, the world’s largest publisher and exhibitions company, was formed from the merger of Reed International, a publisher with roots harking back to 1895, and the older-still Elsevier, a Dutch academic publisher.

Further down the market-cap spectrum, the UK can also boast about engineering brilliance, with the likes of Spirax-Sarco and its world-leading thermal and steam systems and Rotork, a global market leader in valve actuators.

Having cheap valuations is one thing, but investors are keen to know about catalysts, and those are already happening.

There has been a surge in merger and acquisition activity, hitting the highest levels in decades. It’s a double-edged sword, as it means the UK is losing quality businesses to overseas buyers, but it’s also proof that we have something desirable and genuinely trading cheaply (not just optically cheap).

The ever-decreasing size of the stock market is also partly self-inflicted through record share buybacks and we expect more investors to take note and take part.

The UK has a reputation for being tenacious, innovative and ahead of the curve in many respects. So, although our markets will evolve and change and our economy will dip and thrive again, regardless of the broader macro-outlook, there will always be pockets of opportunity in the UK for investors.

Kamal Warraich is head of fund research at Canaccord Genuity Wealth Management. The views expressed above should not be taken as investment advice.

Only a handful of equity income trusts have delivered sector-beating returns as well as yields over 4%.

Now that UK government bonds offer a yield above 4%, equity income strategies have to work harder to justify their existence.

The argument for an equity income strategy is clear: dividend payouts plus the prospect of capital growth and higher total returns than those available from the bond markets. And with many investment trusts trading on a discount, investors can gain access to a portfolio of shares for less than they are intrinsically worth and potentially make additional gains if the discount narrows.

In practice, however, the holy grail of yields plus capital gains has been hard to achieve, with only a handful of investment trusts delivering top-quartile returns over three years with a yield payout in excess of 10-year gilts (4.2% as of 10 July 2024).

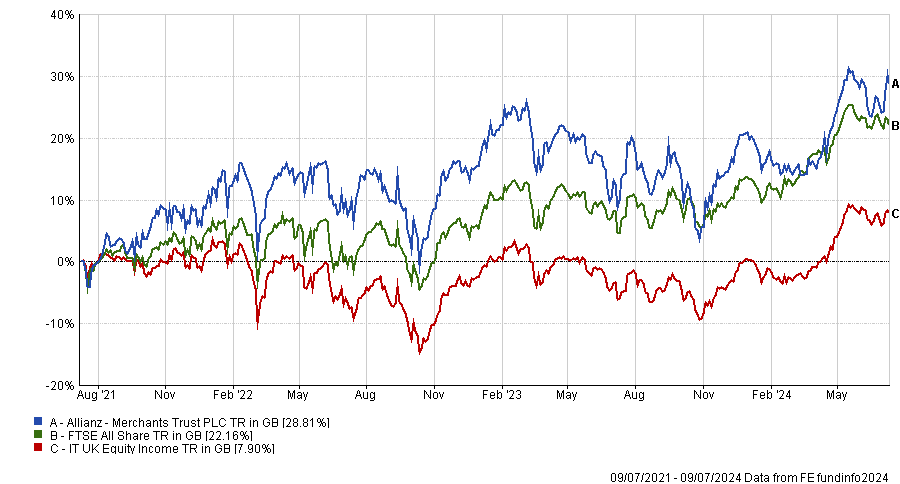

Within the Association of Investment Companies’ (AIC) UK Equity Income sector, Merchants Trust is the only one to make the mark with a yield of 4.9%. It is one of the AIC’s dividend heroes, having increased its dividend for 42 consecutive years.

Peter Hewitt, who manages the CT Global Managed Portfolio Trust and invests in Merchants Trust, said it can be relied upon to keep growing its dividend. “They will not drop the ball” he said.

The £859m trust is the third-best performer in its sector on a total return basis over three and five years. It is trading almost at par, with a very slight discount of 1.4% as of 31 May 2024.

Performance of trust vs sector and benchmark over 3yrs

Source: FE Analytics

Simon Gergel, chief investment officer for UK equities at Allianz Global Investors and head of the value and income team, helms the trust. RSMR analysts described its investment style as contrarian and value-orientated, with an income bias.

Two Asia Pacific equity income trusts achieved top-quartile returns over three years with a yield above gilts: abrdn Asian Income with a 5.7% yield and Schroder Oriental Income paying out 4.5%. The two trusts have grown their dividends for 15 and 17 consecutive years, respectively.

The abrdn Asian Income trust was trading on a 12.4% discount by 31 May and has a £348m market capitalisation. Richard Sennitt’s £690m Schroder Oriental Income trust sits at a 4.2% discount.

Performance of trusts vs sector and benchmark over 3yrs

Source: FE Analytics

Other equity trusts making the grade included BlackRock Latin America (a 6.4% net yield and a 12.9% discount), BlackRock Frontiers (a 4.4% yield and a 5.9% discount) and Schroders’ International Biotechnology Trust (a 4.5% yield and a 8.7% discount). The latter has committed to paying a 4% dividend from capital reserves.

Meanwhile, the Henderson High Income Trust is a top-quartile performer in the UK Equity & Bond Income sector and has a 6.4% yield. It is trading at a 9.7% discount.

For investors who prioritise income payouts, Henderson Far East Income has a 10.5% yield while the British & American Investment Trust boasts an 9% yield.

Two UK equity trusts paid an income over 7%: Chelverton UK Dividend Trust (7.8%) and abrdn Equity Income Trust (7.4%).

However, all four trusts underperformed their peer groups from a total return perspective over three years, which illustrates the difficulty of achieving both income and growth.

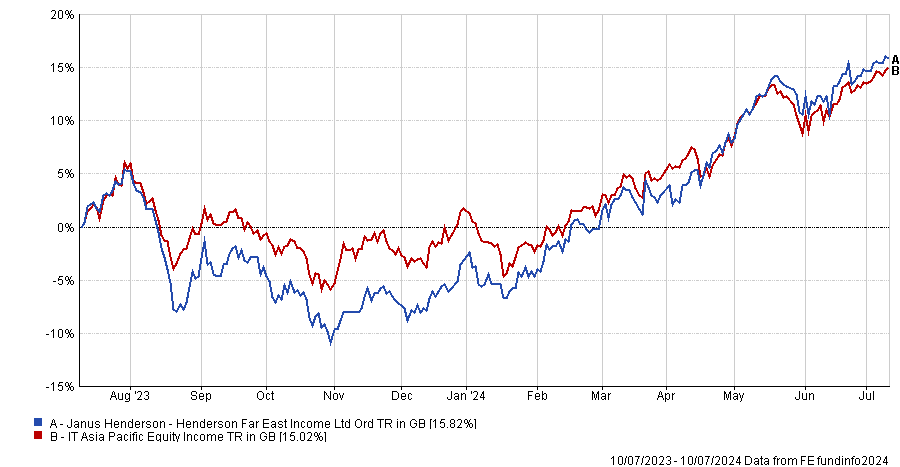

Henderson Far East Income’s performance has struggled, lagging its sector average over three and five years, but it changed hands last autumn when Mike Kerley retired and his colleague Sat Duhra stepped up to become lead manager. Since then, “it's really picked up”, Hewitt said. “He's sorted things out and I’m very impressed.”

Performance of trust vs sector over 1yr

Source: FE Analytics

The £376m trust has been consistently boosting its income by writing call options for a decade or more, Hewitt added.

Labour has inherited an economy in solid shape but clouds remain on the horizon.

The warmest May on record and a strong rebound in the construction sector pushed the UK’s month-on-month GDP growth to 0.4% in May – twice the level economists had expected.

Construction output grew by 1.9% month-on-month, its fastest rate in a year. After a wet April with flat GDP, housing and infrastructure output climbed 2.8% and 3.5% in May, respectively.

The services sector was a significant contributor, with output up 0.3% as consumers flocked to bars and restaurants, and production rose 1.9%.

Danni Hewson, head of financial analysis at AJ Bell, said: “It’s amazing what a bit of warm weather can do. As temperatures soared to record highs in May, shoppers shopped, builders built and lots of us downed a nice cold pint.”

May’s figures brought three-month GDP growth up to 0.9% – the fastest pace of growth since January 2022. Annual GDP growth to May stands at 1.4%.

Neil Wilson, chief market analyst at Finalto, said the GDP figures “hint at the existence of tailwinds for the UK economy just as the government takes office – a bit of luck on the side of Labour.”

Rob Morgan, chief investment analyst at Charles Stanley, agreed that “Labour has inherited a tepid but improving economy”. After last year’s slowdown, the UK is enjoying “a very gentle upswing in activity”.

Falling inflation combined with persistent wage growth at 6% means that households have greater purchasing power, whilst recent cuts to National Insurance and the increase in minimum wages are boosting consumer confidence further, he added.

However, Hewson warned that the economy’s prospects remain vulnerable to the vagaries of the British climate. “July is already looking a bit soggy and even if England can bring the Euros home, boosting pub profits along the way, the wet weather is likely to impact footfall on our high streets and productivity on our construction sites.”

Furthermore, better-than-expect economic growth is a double-edged sword because it makes interest rate cuts less likely.

Derrick Dunne, chief executive of YOU Asset Management, said: “These surprise growth figures for GDP, particularly considering it is the best growth over three months for more than two years, are creating a huge conundrum for the Bank of England (BoE). If the economy is beating inflation and tolerating much higher rates than it has done for over a decade, why cut?”

Robust GDP data has led to a modestly hawkish reaction in financial markets, said Sam North, an analyst at investment platform eToro, “with a slight uptick in the pound versus the dollar and a dip in bond futures”.

“The market's reaction suggests that the data may influence the BoE to maintain or tighten monetary policy, especially given ongoing concerns about services inflation and wage pressures. However, the extent of this adjustment is expected to be limited as market participants await upcoming key economic indicators, including the CPI, wage data and retail sales figures,” he explained.

Conversely, Morgan expects the BoE to cut rates sooner rather than later, now that the Consumer Prices Index (CPI) has hit its 2% target, although he thinks September is a more probable date than August for the first cut.

Overall, the economy in solid shape but it isn’t out of the woods. “The biggest danger is that inflation reaccelerates and interest rate cuts are shallower than anticipated and this acts as a brake on activity,” he cautioned.

The new government also has “some significant structural problems to deal with”, he continued. “Weak levels of investment and company formation alongside low labour force participation are impediments to economic expansion.”

Reducing friction at the border with the European Union would help, he added, as will liberalising planning laws and attracting long-term capital for investment.

Chris Forgan shares the two funds he has bought to benefit from the new government.

Labour’s landslide election result last week has spurred Chris Forgan, portfolio manager of the Fidelity Multi Asset Open range, to take an overweight position in the UK.

Now that the “dust has settled”, there are several reasons for investors to be optimistic about the UK market, including a potential economic recovery.

The economy is already on the up after a slowdown in 2023, with first quarter GDP being revised up to 0.7% by the Office for National Statistics. This was driven by an uptick in consumer spending, said Forgan, which could continue as consumers are saving more at present but might loosen their purse strings if inflation settles.

On this front, Forgan noted that price rises are also “looking more positive” with years of rampant inflation now seemingly behind us.

Although UK inflation was “stickier” and appeared more difficult to “get under control” compared to other regions last year, it has fallen “consistently” this year, he said.

“Services inflation is still higher than the Bank of England (BoE) would like, but we believe it has a dovish bias and that it will begin its rate cutting cycle before long. We believe this should further stimulate economic activity,” said Forgan.

On top of this, more mergers and acquisitions (M&A) being completed at “attractive premiums” and valuations that are “some of the most attractive in the developed market universe” suggest the UK has a lot to offer investors from here.

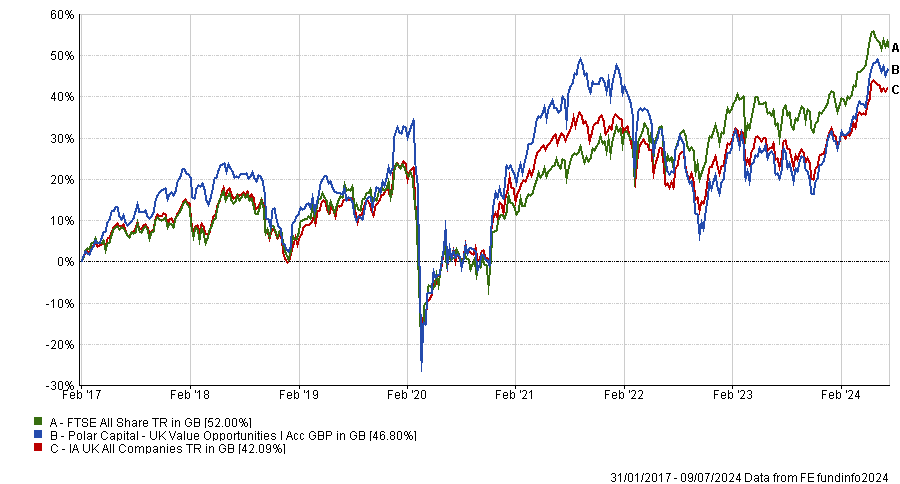

To go overweight the UK, the Fidelity Multi Asset Open range has bought two funds. The first is Polar Capital UK Value Opportunities, which Forgan described as a “market-cap agnostic” portfolio.

Managed by George Godber and Georgina Hamilton, the fund has been under the cosh for some time as it has been hit by the double-whammy of owning value stocks (which have struggled compared to their more growth-oriented peers) as well as mid-caps, which have lagged their large-cap rivals in recent years.

As such, the fund finds itself in the third quartile of the IA UK All Companies sector over three years. However, the fund has come into its own over 12 months and is now ahead of the average peer since its launch, although still lags the FTSE All Share.

Performance of fund vs sector and benchmark since launch

Source: FE Analytics

“We like the strategy’s investment process, which is entirely bottom-up, applying a replicable process to each company in the investment universe. The managers apply a value philosophy, looking for stocks trading at a temporary discount to their intrinsic value,” said Forgan.

“We also favour the mid-cap bias the fund currently adopts – nearly 70% is invested in small and mid-caps.”

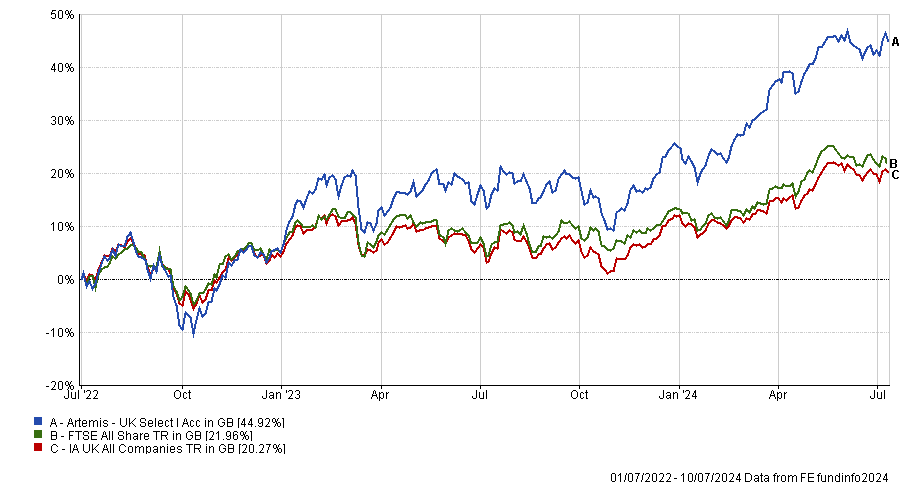

The other fund he uses is Artemis UK Select, headed by Ambrose Faulks and FE fundinfo Alpha Manager Ed Legget.

The strategy was added to the Fidelity Multi Asset Open range during the third quarter of 2022, since when it has been the second-best performer in the IA UK All Companies sector, beating both the FTSE All Share index and its average peer.

Performance of fund vs sector and benchmark since July 2022

Source: FE Analytics

“The strategy is a concentrated multi-cap best ideas fund run by experienced portfolio managers with a strong record of managing UK equity portfolios,” said Forgan.

Managers focus on earnings growth, cash flow and balance sheet resilience alongside re-rating potential, resulting in a portfolio that has no size bias and a value tilt.

Forgan was not the only Fidelity manager keen on the UK’s prospects following Labour’s victory. Salman Ahmed, global head of macro and strategic asset allocation, said there were a number of reasons to be positive from a macroeconomic standpoint.

First he highlighted the UK’s relationship with Europe, which should improve as the new government aims to be more “collaborative and constructive” than its predecessor.

“This approach may lead to smoother trade negotiations, reduced tariffs and more predictable regulatory frameworks, benefiting UK businesses operating within and trading with the EU,” he said.

An 11% gap has opened up between the UK’s pre-Brexit business investment trends forecasts and the current reality, according to the Centre for European Reform, with Ahmed noting that improved relations will be “critical to attracting European and global investors back to the UK market”.

Next is fiscal restraint, with the Labour party more likely to take a cautious approach to tax increases in the short term and an improved outlook for borrowing.

“Growth will be key and political stability, coupled with movement on EU relations, may help maintain the projected fall of the debt burden without crippling spending cuts or tax rises,” said Ahmed.

Lastly, political stability should help encourage investors back to the UK, with the current government in power for the next five years, barring any major setbacks.

“Already, we have seen the government announce changes to the planning laws to help alleviate housing shortages, which signals both a willingness to act quickly and the importance of having a strong majority when it comes to delivery,” he said.

Reduced political risk could lead to lower volatility in the stock market, particularly if Labour is “consistent and transparent” in its policymaking. This would “enhance the UK's reputation as a reliable investment destination”, said Ahmed.

Fund managers pointed to housebuilding, real estate and consumer discretionary.

There is a growing expectation that the Bank of England will soon cut interest rates, potentially as early as its next meeting in August.

Falling interest rates would stimulate economic activity, benefitting the more cyclical areas of the stock market, such as household goods and construction companies, utilities and retailers.

As Rebecca Maclean, investment director, UK Equities at abrdn, said: “Lower interest rates can reduce mortgage rates and debt servicing costs, thereby increasing discretionary income and bolstering consumer confidence.”

Below, managers of UK equity funds explain which sectors and stocks they expect to benefit from rate cuts.

Housebuilding and construction

Falling interest rates reduce the cost of mortgages, making home purchases more affordable, which should enable housebuilders to thrive.

The sector is also poised to benefit from the new Labour government’s commitment to build 1.5 million new homes over the next five years.

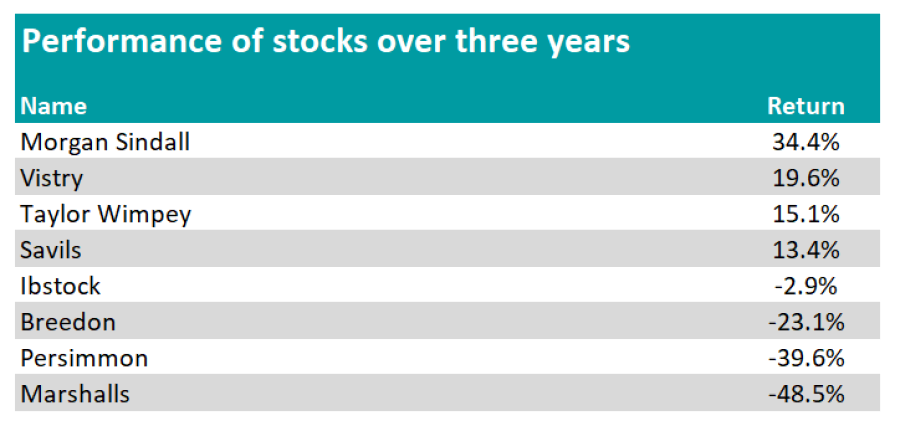

Hence Ambrose Faulks, co-manager of Artemis UK Select, believes housebuilding will be at the “epicentre” of a stock market revival and holds Vistry and Morgan Sindall within his fund.

Job Curtis, manager of The City of London Investment Trust, is also bullish on housebuilders, holding positions in Taylor Wimpey and Persimmon. Additionally, he invests in brick-maker Ibstock and Marshalls, which produces paving stones and roofing products.

“They should benefit medium-term as improved demand leads to more homes being built,” Curtis said.

Simon Murphy, manager of VT Tyndall Unconstrained UK Income, also focuses on businesses that serve the housing industry. For example, he invests in the aggregates business Breedon Group, buy-to-let mortgage provider OSB Group and property manager Savills.

Performance of stocks over 3yrs

Source: FE Analytics

Real estate

Some managers prefer the real estate sector and anticipate an upswing if rates are cut, due to reduced borrowing costs, increased property values and higher demand.

Therefore, Simon Moon, co-manager of Unicorn UK Smaller Companies, favours LondonMetric Property, a REIT focused on logistics and retail properties.

Meanwhile, Callum Wells, co-manager of the Castlefield Sustainable Portfolio funds, prefers Assura, which focuses on general practitioner and primary care buildings.

Charles Luke, manager of Murray Income Trust, believes that Safestore, the UK’s largest provider of self-storage, will thrive.

He said: “Firstly, the interest charged on its debt would decline. Secondly, the discount rate on which its assets would be valued would fall resulting in a higher asset value. Finally, for its customers, a lower interest rate would likely lead to an increase in disposable income and greater housing activity, both of which would be likely to benefit demand for Safestore’s product.”

Performance of stocks over 3yrs

Source: FE Analytics

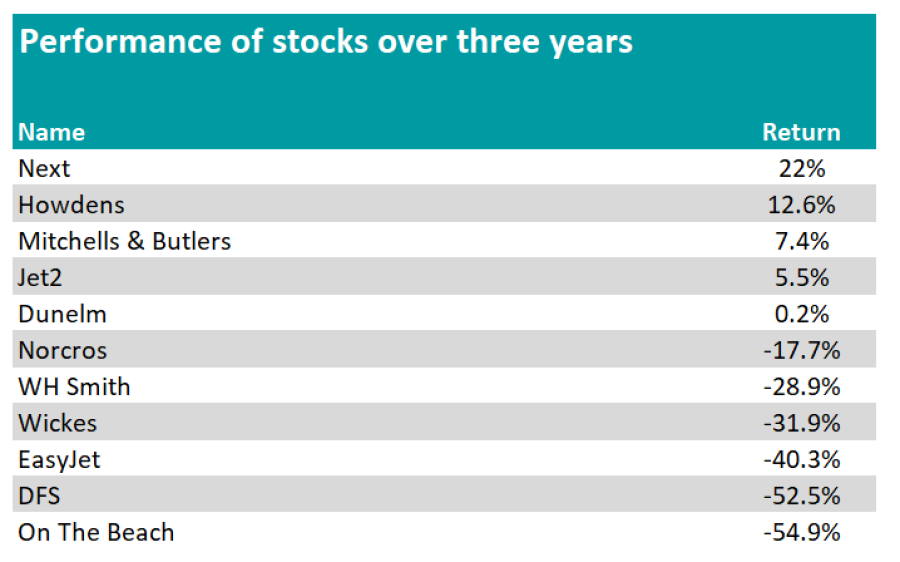

Consumer discretionary

For Andy Gray, co-manager of Artemis Special Situations, one of the “mysteries” of the past six months has been the lack of upturn in consumer spending.

“Covid savings are intact, unemployment is low, wage growth is strong, inflation has eased. Indeed, consumer confidence is back to pre-Covid levels. Yet consumer-facing companies are yet to see it,” he observed.

“Larger ticket consumer purchases in particular look overdue a recovery with volumes well below 2019 levels.”

Interest rate cuts might act as a catalyst to encourage UK consumers to increase their spending, particularly on larger items.

Therefore, Gray holds furniture retailer DFS and kitchen manufacturer Howden, noting that these companies have gained market share during the downturn and enhanced their product offerings.

Murphy, who also holds DFS and Howden in VT Tyndall Unconstrained UK Income, pointed to DIY retailer Wickes and home furnishing retailer Dunelm.

Will Tamworth, co-manager of Artemis UK Smaller Companies, is overweight in the UK consumer discretionary sector, anticipating that rate cuts will serve as a catalyst to encourage consumers to make major purchases.

In addition to investing in home-oriented businesses such as DFS and bathroom equipment retailer Norcros, Tamworth also favours travel-related businesses like low-cost airline Jet2 and online travel agent On The Beach.

Murphy also believes that travel and leisure are themes to play ahead of interest rate cuts. These sectors have been recovering since the Covid lockdowns but he expects increased disposable income after rates fall to provide a further boost.

His key holdings in this area are WHSmith and low-cost airline EasyJet.

Meanwhile, Artemis UK Select invests in clothing retailer Next and the pubs and restaurants group, Mitchell & Butlers.

Performance of stocks over 3yrs

Source: FE Analytics

Financials

UK banks have proven to be a terrific investment since central banks began their hiking cycle and Faulks expects them to continue performing well, even as macroeconomic concerns recede.

He said: “Due to their use of the five-year swap rate to hedge themselves, they are still meaningfully under-earning their full capacity, so we would expect their earnings to grow during the first falls in interest rates. Not least, this will ease deposit pressures.”

Yet, lower rates are likely to benefit the wider financial sector, driven by increased activity and investors seeking alternative income sources.

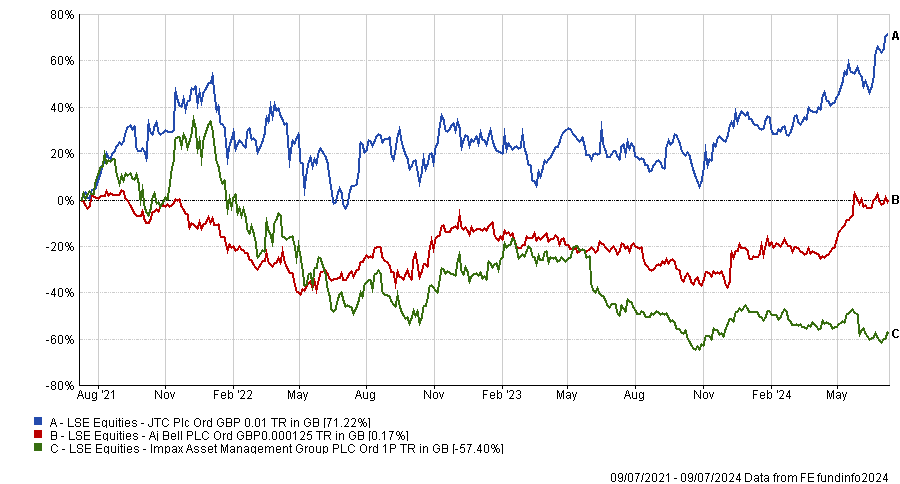

For example, Moon highlighted global professional services provider JTC, which could experience heightened demand for its fund administration and corporate services.

Similarly, investment platform AJ Bell could see gains from higher trading volumes and increased assets under management as investors become more active in a lower-rate environment.

Wells also sees potential in asset managers such as Impax, which are expected to benefit from increased assets under management due to rises in the value of their underlying investments.

Performance of stocks over 3yrs

Source: FE Analytics

Growth companies and small-caps

Finally, fund managers highlighted growth companies and small-caps, both of which suffered as interest rates were on the way up.

Maclean said: “The valuation of equities is sensitive to long-term discount rates. The compression of valuations for growth-oriented companies during the interest rate hikes of 2021 and 2022 exemplifies how heightened discount rates can dampen the present value of future cash flows, with the reverse true when rates fall.”

Moon has invested in recently-listed Raspberry Pi, known for its single-board computer, anticipating increased adoption across various industries.

He also believes that Microlise, a provider of telematics and fleet management solutions, will benefit from increased business investment in efficiency-boosting technologies.

Small-caps have suffered in recent years because they are often more closely connected to the health of the domestic economy, compared to their larger peers.

However, they are also among the first to benefit from interest rate cuts.

Wells concluded: “There is certainly value in small-caps, as evidenced by recent takeover activity, often by savvy private equity investors who have acted quickly to snap up bargains before interest rates reduce and valuations surge again.”

The regulator says it has made the ‘biggest changes to the UK listing regime in over three decades’.

The Financial Conduct Authority (FCA) is overhauling the rules for companies seeking to list on the UK stock markets. The regulator said its changes aim to “boost growth and innovation” and are the most significant amendments to the UK’s listing regime in more than three decades.

The new rules, which will come into effect on 29 July, abolish the need for shareholders to vote on significant or related-party transactions. They also introduce more flexibility around enhanced voting rights. Shareholders are still required to approve major events such as reverse takeovers.

Chancellor Rachel Reeves said: “These new rules represent a significant first step towards reinvigorating our capital markets, bringing the UK in line with international counterparts and ensuring we attract the most innovative companies to list here.”

The number of listed companies in the UK has fallen by about 40% since 2008, according to the government’s UK Listing Review. A spate of British companies – including chip designer ARM Holdings and building materials group CRH – have moved their primary listings to the US to boost their valuations and tap into the US government’s spending spree through the CHIPS and Science Act and the Inflation Reduction Act.

Between 2015 and 2020, the UK accounted for 5% of initial public offerings globally, more or less in line with the UK’s approximately 4% position in global indices, but this is a statistic the regulator wants to improve.

Sarah Pritchard, executive director of markets and international at the FCA, said: “A thriving capital market is vital in delivering investment to growing companies plus returns and choice to investors. That’s why we are acting to make it more straightforward for those seeking to list in the UK, while retaining vital protections so investors can help steer the businesses they co-own.”

Capital market reform, such as making it easier to float and undertake mergers and acquisitions, has “real momentum” behind it, said Sue Noffke, Schroders’ head of UK equities.

She also expects Labour’s planning reforms to help construction companies, while a reversal of the ban on onshore windfarms will favour utilities and the renewable energy sector.

“Such changes could open up great investment opportunities for companies involved in providing grid infrastructure for the renewable transition, while many quoted housebuilders should benefit from planning reform,” Noffke explained.

Going forward, Hargreaves Lansdown hopes that the new government will introduce regulation to improve retail investors' access to initial public offerings (IPOs) and secondary capital raising rounds. At the recent Raspberry Pi IPO, the investment platform was significantly over subscribed, which proves that demand from retail investors is there, said Tom Lee, head of trading proposition.

"Boosting retail investment on the stock exchange will have wider market benefits providing depth and liquidity, as well as boosting interest in investment with the wider public, unlocking further capital for UK-listed companies," Lee said.

However, Chris Beckett, head of equity research at Quilter Cheviot, warned that the listing rules are not the main reason for the London market’s demise and said reforming them is “very admirable” but “a bit of a red herring”.

“The main reason for the gloomy clouds over the City is the makeup of the main indices. London is home to large, legacy industry companies, such as miners, oil and gas and financials, which have been out of favour in the past decade and show no real signs of becoming loved once more,” he argued.

Beckett was sceptical about the government’s ability to attract exciting growth businesses to the UK. Growth investors gravitate towards the US, so “if a business wants to achieve an attractive valuation, it too will go to America”, he suggested. “Many of the companies in the FTSE 100 are global in nature too, so will naturally look to overseas markets if that is a better fit for them.”

Yet despite the UK’s underdog status versus North America, the investment community is optimistic about the new Labour government ushering in a period of stability, which fund managers hope will attract international investors back into UK equities.

John Ions, chief executive officer of Liontrust, said he was encouraged by the government’s “pro-growth agenda”. “Along with falling inflation and the expectation of a reduction in interest rates, this should encourage international investors to return to the UK and boost capital flows to the stock market,” he concluded.

The T. Rowe Price Global Select Equity fund invested in Apple with perfect timing in April 2024 but its underweight exposure nonetheless dragged on relative performance.

Timing when a stock will surge is notoriously tricky but so too is getting the position size right to profit from the movement.

With Microsoft, Apple, and Nvidia making up such a large part of the major indices (over 4% apiece of the MSCI World as of 31 May), active managers need to take substantial positions to keep pace with their benchmarks.

Peter Bates, manager of the T. Rowe Price Global Select Equity fund, invested in Apple in April 2024 with immaculate timing but his position size – 500 basis points underweight versus his benchmark, the MSCI World – weighed on relative performance. “That was a good buy but it still hurt me,” he said.

He initially bought Apple’s shares at $170, calculating a hard downside of $130, a soft downside of $150-160, an upside case of $200 and the best case scenario of $240-250 with an 18-month view.

At that time, Apple’s share price appeared to be on the way down so he did not want to go overweight, but the narrative has changed substantially since.

In the past couple of months, Apple has disclosed plans to embed more artificial intelligence (AI) functionality into its iPhones and talked about partnering with third parties. At a developer conference on 10 June, the company unveiled a range of AI features including writing assistance tools, customisable emojis, integration with ChatGPT and a reboot of its voice assistant Siri.

These developments propelled Apple’s share price from $170 to $228 by 9 July, including a 7% rise the day after last month’s developer conference.

Bates was left kicking himself for not having bought more of the stock. “It's pretty amazing how fast the stock has gone from $170 to $220 and it makes me question, why did I only buy 250 basis points? That's 50 basis points that I've lost in relative performance after doing all this work,” he rued.

“I got very fortunate with the timing and that's the funny thing about this business, where even when you make a good decision, you [ask yourself] why didn't I buy more of it?

“Even when you do a lot of work and you think you know what's going to happen, getting the timing right is fool's gold, so you just hope to be in the game.”

He does not plan to add to the position now, however, because the current share price is so close to his upside target.

Apple’s share price ytd

Source: Google Finance

Before April, Apple was struggling to grow and had not announced any innovative new products for some time, but Bates expected the company to find a way to embed an AI assistant into its iPhones and monetise that.

He sold a consumer stock to fund the position in Apple, which he views as the consumer staple of the tech sector. People tend to upgrade their iPhones every four or five years, so Apple’s sales are easy to predict by looking at volumes four years ago, he noted.

Part of his investment thesis for Apple is how valuable people’s phones are to them. “God forbid if your phone breaks, you immediately buy a new one.”

Apple hasn’t been the only top performer for the Global Select Equity fund, however. Indeed, its top-quartile performance in the IA Global sector over the past year is due to another tech giant, Nvidia.

Performance of fund vs benchmark and sector over 1yr

Source: FE Analytics

Bates bought into Nvidia last summer – having earlier looked at the stock in the autumn of 2022 when he decided to buy Advanced Micro Devices (AMD) instead, which he thought was closer to its valuation trough. Nvidia appeared too expensive, he said, admitting to underestimating its upside case. Six months later, AMD was up 60-70% but Nvidia had risen over 250%.

Bates admitted his mistake and revisited Nvidia, quoting Amazon’s ‘day 1’ culture of making decisions with a clean slate. His decision to buy into the chip designer proved prescient as its share price has risen 213% in the past year to 9 July 2024.

Nvidia’s share price over 1yr

Source: Google Finance

To put the difficulty of this decision into context: Will Low, head of global equities at Nikko Asset Management, also bought Nvidia in August 2023 and described it as “a potential egg in face scenario” given the share price had already doubled.

He was concerned about being accused of index hugging because he was buying one of the largest positions in his benchmark after it had run up significantly.

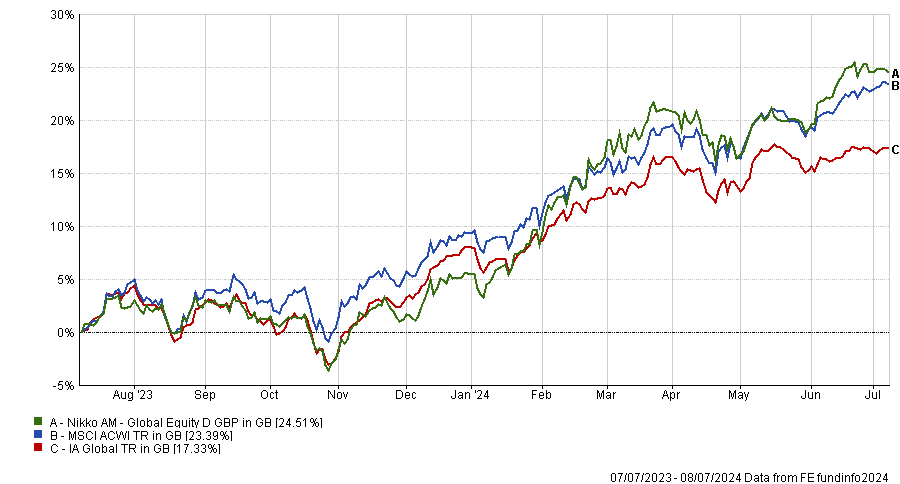

Performance of fund vs benchmark and sector over 1yr

Source: FE Analytics

The decision paid off as the Nikko AM Global Equity fund, which currently has 6.9% in Nvidia, is a top-quartile performer within the IA Global sector over one and five years.

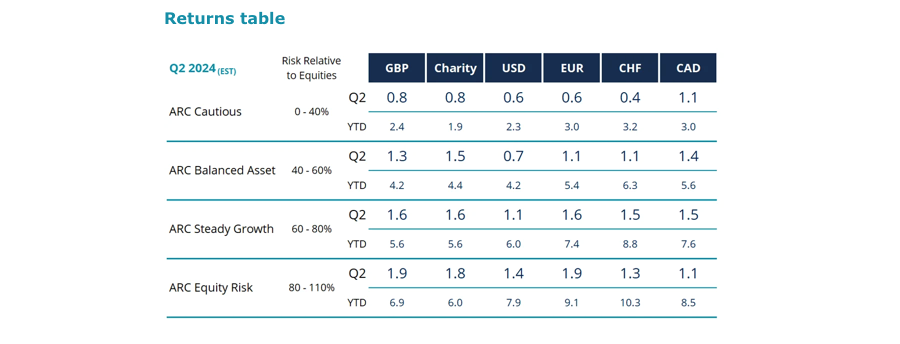

Those surveyed are significantly keener on equities than they were a year ago, according to recent research.

Despite a year of election fever, with more than 70 countries are expected to go to the polls, wealth managers have become more bullish on equities, according to a survey by Asset Risk Consultants (ARC).

Sentiment towards stock markets has risen to 57% amongst wealth managers, a dramatic rise from the -22% sentiment over the past 12 months. This swing suggests investment managers are becoming less concerned with the consequences of upcoming elections.

Additionally, 63% of the 90 surveyed chief investment officers (CIOs) from wealth management firms were now expressing positive views on equities, a rise from just 13% this time last year.

Source: ARC

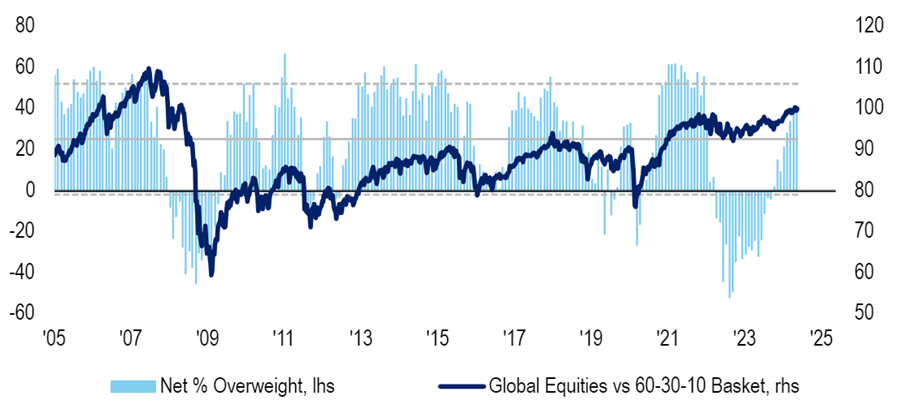

ARC CIO Grant Wilson said, while elections can drive market volatility, recent analysis suggests that new government proposals can boost demand.

“In the medium-to-long term, reforms could create a more favourable business environment and support sectors with a high domestic exposure.”