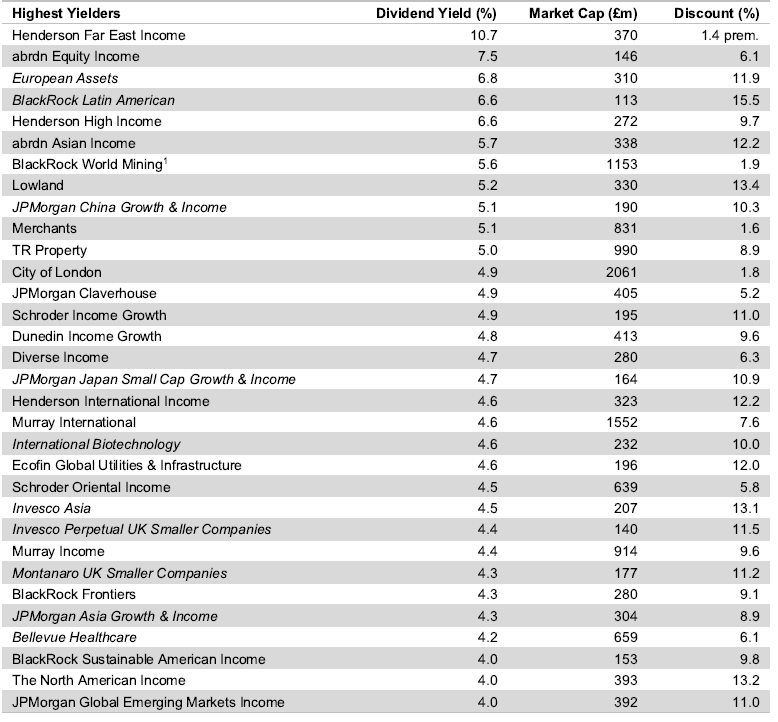

More than 30 investment trusts are offering yields above 4% but investors should take a closer look at how that income is generated before piling in, experts warn.

Income-seeking investors can find rich pickings amongst the investment trust sector, with many trusts offering yields above government bonds plus the prospect of capital gains and an extra kicker if discounts narrow.

Wealth manager Stifel found that 32 trusts investing primarily in equities have a yield of 4% or more and a market capitalisation above £100m. This compares to yields of 4.5% and 4.4% from two-year and 10-year gilts, respectively.

The highest-yielding equity investment companies

Sources: Stifel, Datastream as at 29 Apr 2024

Almost all of the trusts on Stifel’s list have increased their dividends in the past year as revenues from their underlying equity portfolios have grown, the exception being BlackRock World Mining.

Iain Scouller, managing director, investment funds at Stifel, said: “For those investors prepared to take equity risk, we think the yields on these trusts are relatively attractive.”

Before diving in, experts cautioned investors to research why yields are high in the first place.

Shavar Halberstadt, an equity research analyst at Winterflood Investment Trusts, said: “There is nothing wrong with investing in a trust because of its yield, but we encourage investors to assess whether this is share price-driven, enhanced by leverage or intrinsic, and which profile best suits their risk appetite.”

Edward Allen, private client investment director at Tyndall Investment Management, agreed. The first question to ask is whether or the dividend is covered, he suggested.

“If not, you are just paying income out of capital. Others use derivatives to boost their income, selling away some of the potential gain to boost income,” he said. “Again, I’m not a fan, as this blunts the potential total return of the investment.”

Dividend yields are a function of the income offered, as well as the share price. If a fund is trading on a steep discount to net asset value (NAV), the yield may be high as a result. Therefore, Winterflood makes a distinction between funds offering a high dividend and those that are simply out of favour, Halberstadt explained.

“To disentangle the effects of discounts to NAV, we looked at the highest dividend yield on NAV instead. If you exclude special situations (i.e. returns of capital driven by managed wind-downs), examples of relatively high income on an absolute basis are Henderson Far East Income, Chelverton UK Dividend, Aberforth Split Level Income and abrdn Equity Income, all with NAV yields ranging between 7% and 11%.”

To complicate matters further, some investment companies are “manufacturing” yield by funding a revenue shortfall out of capital, Scouller said. For instance, Montanaro UK Smaller Companies paid a 4.5p dividend for the year ended 31 March 2023, when its revenue earnings per share were 2.3p and the capital return was -21p per share. The dividend paid was only 0.51x covered by revenue earnings, he noted.

Ryan Lightfoot-Aminoff, investment trust research analyst at Kepler Partners, said some trusts use revenue reserves to pay dividends in leaner years, having replenished the coffers during better times.

He explained: “abrdn Equity Income is one example of this. In the most recent financial year (ending September 2023) the trust generated revenue after tax of £11.1m. It paid a total of £11.2m in dividends, using a small amount from reserves to cover the difference. This ensured the trust maintained its very high yield and impressive track record of growing the income.”

The trust had remaining reserves of over £10.1m, which could support the dividend in future if necessary, Lightfoot-Aminoff noted.

Halberstadt added that financing dividends from revenue reserves enables “a smoothing of dividend volatility over multi-year periods and the potential generation of dividend growth even when portfolio income stagnates”.

Trusts can also use debt financing – or gearing – to magnify their yield on NAV, he continued. “This is relevant for instance for Chelverton UK Dividend and Aberforth Split Level Income, who each have debt levels exceeding 30% of NAV.”

Another factor to consider is whether a trust’s yield appears to be high because of special dividends that may not continue.

Meanwhile, James Carthew, head of investment companies at QuotedData, warned investors to look out for value traps, where yields are high because the share price is cheap and likely to fall further. The best way to avoid value traps is to steer clear of the highest decile of high-yield equities, he noted.

“I think this explains Henderson Far East Income, which produces a yield far higher than most competing Asian income trusts yet its long-term total returns are by far the worst in its peer group (an average of 4.7% per annum over the past 10 years compared to 6.6% for abrdn Asian Income – the next worse – and 10.3% for Invesco Asia – the best),” Carthew said.

“Similarly, abrdn Equity Income is the worst-performing trust in its peer group (2.4% per year over 10 years, compared to 4.0% for Lowland, the next worse). However, there is another factor at play here, both trusts have highish exposures to smaller companies, which have been lagging their larger peers.”

At the other end of the spectrum, Carthew believes Henderson High Income is a better choice.

“It has a trick up its sleeve when it comes to generating its attractive yield. It borrows money long term at fixed rates and invests that in higher-yielding bonds. That generates income that goes toward the dividend and allows David Smith, the fund’s manager, to avoid the value traps and buy lower-yielding stocks with better business models and faster dividend and earnings growth. Investors in Henderson High Income get the best of both worlds, therefore.”

In some cases, a high income can be indicative of a timely investment opportunity, Allen pointed out. “Trusts paying a high income out of received income might indicate an area out of favour with markets and a potential opportunity; some Asian income trusts fit this bracket, and potentially some of the UK trusts too.”

Valuations in Indian large-caps do not appear stretched and are justified by the nation’s structural growth.

The Indian elections are in full swing, with current prime minister Narendra Modi hoping he has done enough to stay in power for a third term.

With a process lasting more than six weeks and with more than 970 million registered voters, the country has been dubbed ‘the world’s largest democracy’. To put this into context, the entire population of Europe is 741 million.

Modi is widely expected to retain power, with recent estimates indicating his Bharatiya Janata Party (BJP) will win around 300-320 seats – with a few more going to its allies (543 Lower House seats are divided up, with a 272-seat majority needed).

Modi’s policies have transformed India in the past decade. They cover banking, manufacturing, inflation management and an increased focus on physical and digital infrastructure, all of which have boosted the long-term growth potential of the economy.

The numbers speak for themselves – at a time when growth has been challenging across the globe, GDP in India stood at 6.7% and 6.4% in 2022 and 2023 respectively, with estimates that it can grow at 6.7% consistently over the next decade.

This is aided by some significant tailwinds benefitting the economy. They include demographics (50% of the population will be comprised of Millennials and Gen Z’s by 2030) and a growing middle class (the percentage of high and upper middle-income households in India is expected to rise from 26% in 2021 to 45% in 2030). In short, the characteristics of India’s growth are very much structural rather than cyclical.

More changes to come

Dipojjal Saha, a macroeconomist and product specialist at Ashoka India Equity, cites the infrastructure story as a key element, with a compound annual growth rate (CAGR) on capital expenditure standing at circa 20% since Modi came to power.

Saha said: “90% of India’s railways are now electrified, compared with 30-40% previously. The number of airports has doubled, while the turnaround time at ports has improved rapidly. Previously, some 20 million rural homes had access to tap water, now almost all of them have access.”

The second area bearing fruit is manufacturing, with India having already made strides in both defence and technology. The ‘Make in India’ initiative has successfully reduced India’s reliance on imported goods. India’s government has cut corporate taxes for new manufacturing production and launched production-linked incentive schemes across multiple sectors.

Goldman Sachs India Equity portfolio manager Hiren Dasani said: “Progress has been made since Make in India was first introduced in areas like electronics given fast-growing domestic demand. Capex intensive industries, such as electric vehicles and semiconductors, may have to rely on global corporations as they develop due to a lack of raw materials domestically. Mobile phone supply chains have been shifting from China to Vietnam and India.”

But there are clearly far more societal strides to be made. For example, the minimum wage in India is lower than other Asian economies, while only one in five women are in the official workforce.

Lofty valuations are justified – and this is why

The trouble is that India’s success story is one of the worst kept secrets and this is reflected in valuations. Figures show the MSCI India price-to-earnings (P/E) premium over the MSCI Emerging Markets index is currently between 70% and 80%, whereas the average since 2007 has been closer to 40%.

But there is a strong argument to support those numbers. Not only has growth been justified, given the likes of urbanisation, attractive demographics and the rise of digitalisation, but the de-rating of China has shaken up the composition of the market.

Only a couple of years ago, India accounted for just 10% of the MSCI Emerging Markets index (with China accounting for 35%). India’s exposure has now almost doubled to 18%, while China has fallen to 25%, Saha pointed out.

When you compare India’s valuations versus its own history, it is a different story. “Valuations for the past 10 years in India have been 20.7x, it is currently around a P/E of 19.7x, so they are not stretched. It has also seen the highest earnings growth amongst its peers,” Saha argued.

This bring us back to the aforementioned structural – not cyclical – growth story. Alquity Indian Subcontinent manager Mike Sell said that while India’s P/E has re-rated over the past decade due to Modi’s reforms, valuations are not stretched.

“India has a high P/E because of strong earnings growth over a number of years. The earning per share stand at 17%, giving it a price/earnings-to-growth (PEG) ratio of 1.3x. On a PEG basis, India is cheaper than the likes of Korea, Japan, Mexico and the UK,” Sell said.

“Countries like Korea, Taiwan and Thailand may have a lower PEG, but they are cyclical, not structural stories. India has multi-years of growth, not pockets of opportunity.”

One area that does look more expensive is the small and mid-cap space. UTI India Dynamic Equity assistant manager Ravi Gupta said valuations are at a 25% premium for mid-caps and slightly higher for small. This follows two strong years when firstly, supply chains recovered as businesses started to re-open post-Covid, promptly followed by the fall in commodity prices.

Gupta’s exposure remains around the 35-40% mark in the small and mid-cap space, having taken profits in some areas and reoriented into other parts of this market. “One thing that has helped in the last few years has been the increase in IPOs. It has presented a number of opportunities to investors,” he added.

India’s growth is hard to ignore. The International Monetary Fund expects it to be the third-largest global economy by 2030 as its GDP continues to stand out from its peers. Valuations are a consideration – but experienced active managers should be able to cut through the noise to tap into the opportunities in the region.

The case for investing in India as a standalone allocation continues to grow. Those who may prefer exposure as part of a wider emerging markets portfolio may want to consider the likes of the GQG Partners Emerging Markets Equity or FSSA Global Emerging Markets Focus, which have 29.7% and 24% invested in the country, respectively.

The views expressed above should not be taken as financial advice. Darius McDermott is managing director of FundCalibre and Chelsea Financial Services.

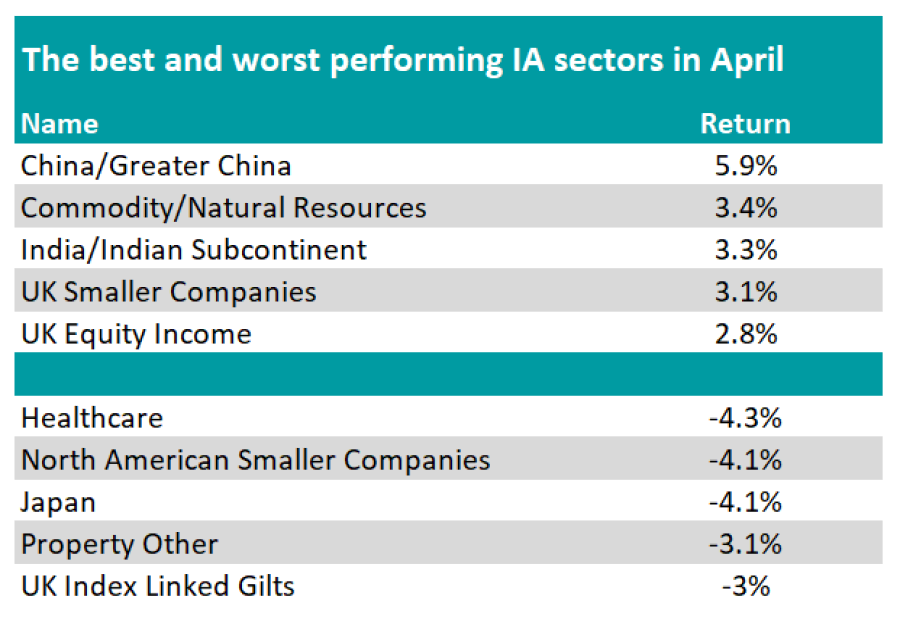

China and the UK strike back, while Hipgnosis Songs returns a record 50.7% in a single month.

Chinese equities recovered from their doldrums and soared to the top of the charts in April, but experts are wondering whether this is merely a “dead cat bounce”.

IA China/Greater China was the best performing sector in April, with the average fund gaining 5.9%.

It is the second time this year, following February, that the sector has claimed the top spot. However, the main reason for this outperformance appears to be the market's cheapness, with Chinese equities trading at nearly 20-year lows.

Ben Yearsley, director at Fairview Investing, posed the question: “Is this a dead cat bounce or are investors starting to see real value in China?”

India – China’s main rival in the emerging markets – also had a robust month. The IA India/Indian Subcontinent sector ranked as the third best performer in April, with the average fund returning 3.3%.

Although its two poster children outshone other markets, the IA Global Emerging Markets sector only returned 1.4% last month, making it the seventh best-performing sector.

Source: FE Analytics

The UK, another unloved and cheap market, also had a strong run in April, with the FTSE 100 hitting an all-time high. As a result, IA UK Smaller Companies, IA UK Equity Income and IA UK All Companies all feature among last month’s six best-performing sectors.

Yearsley said: “BHP’s bid for Anglo American plus other decent results and continued buybacks are propelling one of the most unloved markets higher. Interestingly, some fund managers don’t think the UK market has reacted yet to £50bn a year of share buybacks as it’s pension funds that have been selling to fund the purchases.

“Now they’ve almost run out of UK equities, where will companies get their shares from to repurchase? Will this finally ignite the market?”

At the foot of the table, IA Healthcare was April’s worst-performing sector, followed by IA North American Smaller Companies and IA Japan, which was impacted by the weak yen.

“The Bank of Japan disappointed markets with no further action to either support their currency or up rates. Consequently, the yen was again the weakest of the major currencies falling 3.03% against sterling,” Yearsley said.

Source: FE Analytics

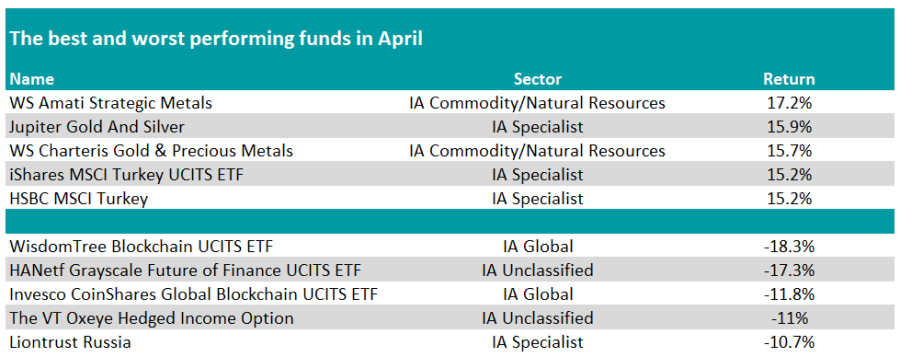

At the fund level, funds specialising in precious metals once again claimed the top spots, mirroring their performance from last month.

WS Amati Strategic Metals led the pack with the highest return at 17.2%. It was closely followed by Jupiter Gold And Silver and WS Charteris Gold & Precious Metals, the latter maintaining its position at the top of the table for a second consecutive month.

Yearsley said: “Gold hitting an all-time high has finally had an impact on gold equities as well as other related areas. Silver has been on a tear as well.

“Also, in the broader commodity space, copper is responding to a shortage in supply and an increase in demand due to decarbonisation and electrification. The price of copper rose about 15% in April.”

Passive funds tracking the MSCI Turkey index also had a strong month.

There was no discernible trend at the bottom of the table. WisdomTree Blockchain UCITS ETF was the worst-performing fund, as it fell 18.3%, while The VT Oxeye Hedged Income Option made its second appearance in a row among the laggards.

“It’s a fund that has featured regularly at both top and bottom of the tables,” Yearsley said.

Source: FE Analytics

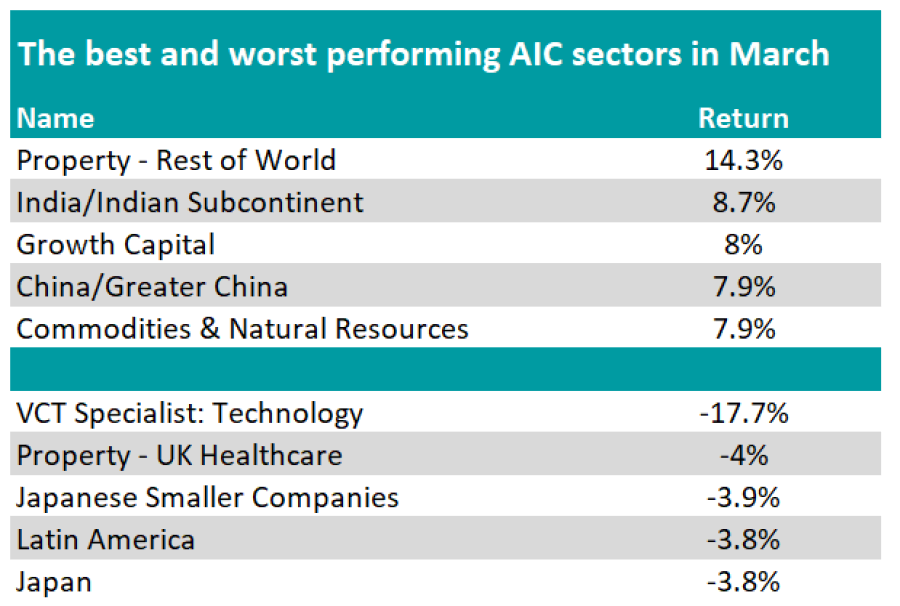

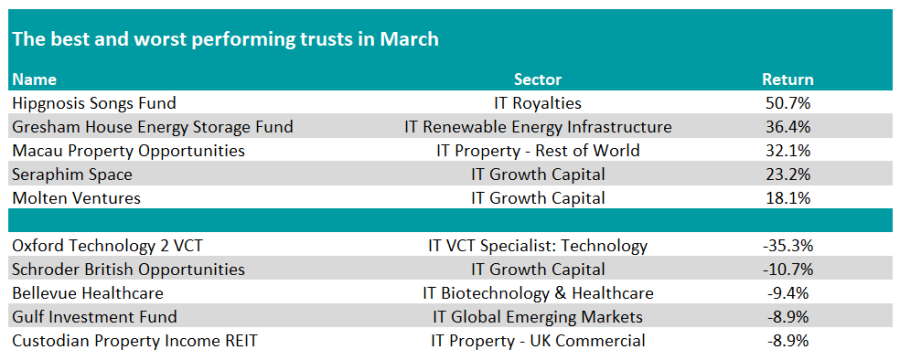

In the world of investment trusts, the IT Property – Rest of World sector claimed the top spot, followed by the IT India/Indian Subcontinent and IT Growth Capital sectors.

Meanwhile, at the bottom of the pile, we find IT VCT Specialist: Technology, IT Property – UK Healthcare, and IT Japanese Smaller Companies.

Looking at individual funds, Hipgnosis Songs Fund took the crown, after returning 50.7% in a single month. The music royalties trust has been at the centre of a bidding war, culminating in Blackstone agreeing on 29 April 2024 to acquire it for roughly $1.6bn.

Yearsley said: “Hipgnosis is finally being put out of its misery with bid and counterbid propelling it to the summit last month with a gain of 50%. Obviously, context is everything and it only means it’s a few pennies above the IPO price. Such is the ignominy it has had over the last year or so. The whole episode does leave an unpleasant taste for many.”

Source: FE Analytics

Other top performers in April include Gresham House Energy Storage Fund, Macau Property Opportunities, Seraphim Space and Molten Ventures.

Conversely, Oxford Technology 2 VCT, Schroder British Opportunities, Bellevue Healthcare, Gulf Investment Fund and Custodian Property Income REIT were the worst performing investment trusts.

Investors could emulate the Sage of Omaha by reinvesting dividends, holding stocks forever and only investing in areas they understand – or by buying Berkshire Hathaway shares.

Berkshire Hathaway’s Warren Buffett is one of the most successful investors of all time but the basic tenets of his approach are uncomplicated and can be adopted by private investors. What’s more, there are several ways to gain exposure to Berkshire Hathaway directly or to funds with similar approaches.

Since the start of Buffett’s career in 1965, Berkshire Hathaway has produced a staggering 4,384,749% return, turning $100 into more than $4.3m. An investor who put $100 into the S&P 500 index in 1965 instead would have made $31,323.

If this makes you want to invest in Berkshire Hathaway, chances are that you already do.

Berkshire Hathaway is the seventh biggest stock in the US, having overtaken Tesla this year, so anyone owning an S&P 500 tracker will have 1.8% in Berkshire Hathway, which falls to about 1% for passive global equity funds.

Investors who want to increase their exposure can buy ‘B’ class shares in Berkshire Hathaway, which is quoted on the New York Stock Exchange, for £330 each and these shares can be held in an ISA, SIPP or standard trading account.

However, Laith Khalaf, head of investment analysis at AJ Bell, pointed out that “Berkshire is a bit of a strange beast, part holding company, part investment portfolio, so it’s set apart from a normal investment trust or fund, though it is still a capital allocation vehicle for Warren Buffett”.

Therefore, some investors might prefer to opt for a fund with a similar investment philosophy to Buffett and there are plenty of choices.

“Lindsell Train also hunts for high-quality companies with competitive advantages and quotes Buffett in its investment philosophy,” Khalaf said.

“Fundsmith’s mantra of ‘buy good companies, don’t overpay and do nothing’ could easily have been penned by Buffett and the publication of an ‘owner’s manual’ was an idea pioneered by Buffett in the 1990s.”

Performance of funds versus sector over 10 years

Source: FE Analytics

Khalaf continued: “Meanwhile, a lesser known fund, SDL UK Buffettology, explicitly seeks to replicate Buffett’s investment style within the confines of the UK stock market.

“Buffett’s pawprints can be found liberally spattered across the investment management industry in one form or another.”

Performance of fund versus sector over 10 years

Source: FE Analytics

Investors could go one step further and adopt Buffett’s principles themselves.

First and foremost, Buffett is an advocate of long-term, buy-and-hold investing. “Our favourite holding period is forever,” is one of his most-quoted sayings.

Khalaf added a word of caution: “Investors should also be wary of letting a long-term view slip into complacency or apathy, which can be harmful if poorly performing stocks or funds in your portfolio aren’t occasionally weeded out.”

Despite being one of the world’s best-known active managers, Buffett is an advocate of cheap passive funds. In his will, he has requested that 90% of the money he leaves to his wife be invested in a low cost S&P 500 tracker and the other 10% be held in short-term government bonds.

For investors who do want to take a punt on active managers, the Buffett way is to opt for high-conviction strategies. As Khalaf explained: “The point is, if you are going to invest in active funds, you should do it properly by choosing a manager who acts with conviction and puts meaningful sums into each of the companies they back, rather than placing a chip in most of the companies on the stock market.”

For investors who do not need to draw an income from their portfolio, dividends should be reinvested. “Buffett likes to receive dividends, even though Berkshire Hathaway doesn’t pay one,” Khalaf said. Instead, Buffett recycles dividend income into new investment opportunities.

“The long-term benefits of rolling up dividends are clear, particularly when investing in a high yield market like the UK, and especially if maintained within the tax sheltering walls of an ISA,” he added.

Finally, never invest in something you do not understand and that applies especially to cryptocurrency. Buffett went so far as to say that cryptocurrencies are “probably rat poison squared” and “they will come to a bad ending”.

The House of Lords has written to the Financial Conduct Authority demanding urgent action to resolve the 'ludicrous' cost disclosure rules for investment trusts.

The House of Lords has lambasted the Financial Conduct Authority (FCA) for misinterpreting European Union regulations on cost disclosure requirements for investment trusts.

Misleading costs are discouraging investors from putting as much as £7bn a year into investment trusts – money that some of the more domestically-focussed trusts could channel into the UK economy.

This has resulted in a material loss of permanent investment into the capital markets via equity trusts and the acquisition of UK real assets by foreign investors at significantly reduced prices, the House of Lords financial services regulation committee wrote in a letter to FCA chief executive Nikhil Rathi, published today.

The letter criticised the FCA’s interpretation of MiFID (Markets in Financial Instruments Directive) and PRIIPs (Packaged Retail Investment and Insurance-based Products). These regulations are compelling investment trusts to report their costs in the same format as open-ended funds.

For investors in open-ended funds, managers’ fees eat into the returns they receive. That is not the case for listed investment companies, where costs do not detract from the share price gain or loss that investors experience. Disclosing costs for trusts in the same way as funds risks confusing investors and makes trusts appear more expensive than they actually are.

“This has created a falsely elevated number for aggregated ongoing cost forecasts,” the committee’s letter stated, “giving misleading information to investors and indicating that costs/expenses are to be deducted annually from shareholdings.”

Baroness Bowles of Berkhamsted, a member of the House of Lords financial services regulation committee, said investment trusts “have given institutions and individuals an opportunity to invest in infrastructure, growth companies and renewable energy” an are “a British success story”.

“This success is under threat by the FCA’s interpretation of EU-retained MiFID and PRIIPs, which is not shared by any other country, and has created an unlevel playing field on an international level. Urgent steps are necessary to resolve the problems that have been created.”

The FCA’s forbearance statement, issued on 30 November 2023, granted investment companies some reprieve by enabling them to provide a factual breakdown of the component parts of their costs, with additional context. This “helped, but does not go far enough”, Bowles said.

Part of the problem involves a central EU database in which costs are recorded. “A potential solution could lie in requiring Authorised Corporate Directors to enter zero into the appropriate column that is for ongoing fund charges, aligning with the practices of EU funds, rather than inputting figures that result in misleading disclosures,” she suggested.

“It is ludicrous that directors and companies are being forced to make misleading statements to investors.”

Trustnet looks at funds within the IA Global sector that have been run by the same manager since 2004 or earlier and have achieved top-quartile returns over the past three years.

The IA Global sector is arguably the most competitive in the Investment Association universe, with 566 funds attempting to make outsized returns.

One way investors could look to whittle down the array of options is to look at veteran fund managers who have delivered time and again – after all, there has been no shortage of hurdles in the world of global equities over the past few decades.

Below, Trustnet researched the funds that have been managed by the same person since 2004 or earlier and have produced top-quartile returns over the past three years, showing those who have been through it all and continue to make top returns.

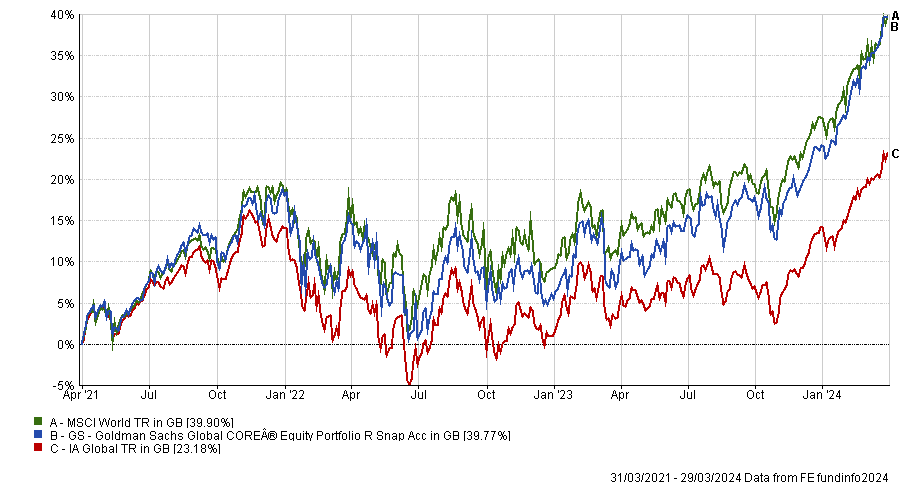

One of those funds is GS Goldman Sachs Global CORE® Equity Portfolio, managed by Len Ioffe since October 2004. In January 2013, he was joined by Osman Ali and Takashi Suwabe.

Their portfolio aims to replicate the same style, sector, risk and capitalisation characteristics as the fund’s benchmark (the MSCI World index), with the underlying stock and country selection responsible for generating outperformance.

Due to the benchmark-aware approach, the fund has a low tracking error. However, it is not a full replication of the MSCI World index. For example, it is underweight Tesla relative to the benchmark and does not hold Exxon Mobil, both of which are top 10 constituents of the MSCI World index.

Furthermore, it has overweight positions in European stocks such as ASML and Novo Nordisk, with both featuring among the fund’s top 10 holdings.

Although it sits in the top quartile of the IA Global sector over three years, it has slightly lagged the MSCI World index. This underperformance can be attributed to recent market returns being driven by a handful of names. Moreover, the fund has been more volatile than the benchmark as well as its sector peers in this timeframe.

Performance of fund over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

The higher volatility relative to the benchmark and the sector has also been a feature of the fund over the past decade. However, it has delivered returns in excess of the MSCI World index in that period, while also ranking among the sector’s top quartile funds.

The other veteran manager to achieve the same feat is Mike Willans, who has been at the helm of WS Canlife Global Equity since 2004 and was joined by Bima Patel in 2018.

They build their portfolio by combining both top-down macro views and bottom-up stock picking. The managers also try to spread their allocation across different sectors and factors to ensure balance and diversification.

Moreover, Willans and Patel may invest in bonds and other collective investment schemes to diversify their sources of return. For instance, the fund currently invests in US utilities tracker iShares S&P 500 Utilities and X Harvest CSI 300, which replicates the performance of the 300 largest companies listed on the Shanghai and Shenzhen stock exchanges.

When it comes to stock selection, the two managers consider factors such as a company’ market position, the strength of its brand, its susceptibility to current market and economic trends and the drivers behind its earnings and dividend growth.

Performance of fund over 3yrs (to last month end) vs sector and benchmark

Source: FE Analytics

Its five largest holdings include Microsoft, Apple, Amazon, Alphabet and JP Morgan Chase & Co, according to FE Analytics.

The fund has also made a top-quartile performance over five years, but sits in the second quartile of the IA Global sector over a decade. Nonetheless, it has consistently been one of the least volatile funds in the sector, both over three and 10 years.

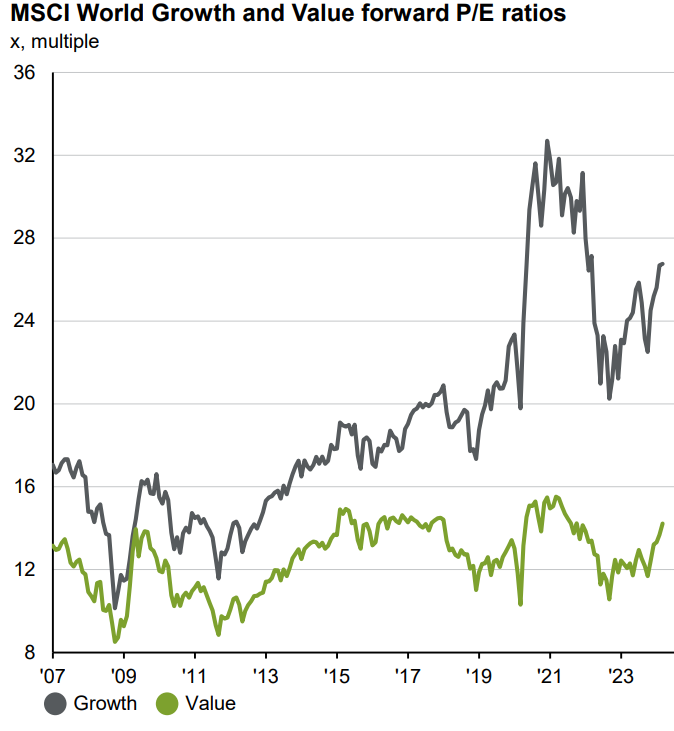

Charles Stanley’s Rob Morgan reveals his favourite value funds to help diversify away from the growth style of investing.

Growth stocks are outperforming once more in 2024 although Charles Stanley thinks investors should ensure they are diversifying their portfolios through some exposure to the value investing style.

Value investing – or buying out-of-favour companies that are trading at less than their true worth – has struggled to keep up with growth investing – or looking for companies with strong earnings potential and prospects for promising expansion – for much of the past decade.

Although the value style outperformed in 2022, when inflation was surging and central banks were hiking interest rates, growth has returned to the fore more recently as investors have started to anticipate rate cuts in the future. But this doesn’t mean investors should pour everything into growth, warned Charles Stanley chief analyst Rob Morgan.

“Recent market moves perhaps suggest growth stocks are starting to crack under the pressure of expectations of interest rates staying higher for longer,” he said. “It’s a reminder to investors not to have a portfolio skewed too much in one direction and to consider rebalancing as different areas perform at different rates.”

With this in mind, below are five funds picks that allow investors to cover the global market with a value approach.

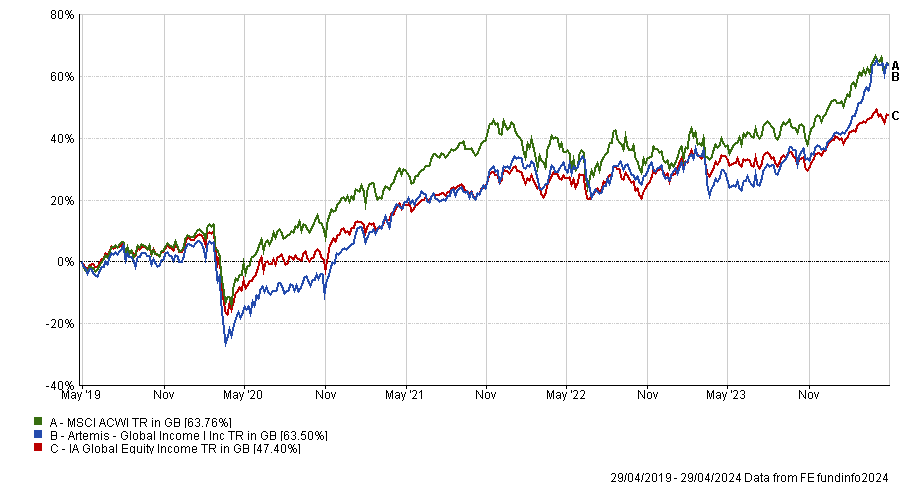

Global: Artemis Global Income

Starting with global funds, Morgan pointed to Artemis Global Income. The £1.3bn fund, which is managed by Jacob de Tusch-Lec and James Davidson, is run with a bias towards value stocks for two reasons: the need to generate income and the managers’ contrarian nature, which sees them favour ‘turnaround situations’.

Performance of Artemis Global Income vs sector and benchmark over 5yrs

Source: FE Analytics

“It therefore provides variety and diversification within an income portfolio or an option for growth investors seeking diversification from more tech-orientated global funds,” Morgan added, as the portfolio’s largest sector allocations are to financials and industrials.

Artemis Global Income is currently in the IA Global Equity Income sector’s first quartile over one, three and five years.

UK: Man GLG Undervalued Assets

Turning to UK equities, Morgan likes Henry Dixon and Jack Barrat’s £1.4bn Man GLG Undervalued Assets fund. The managers look for companies whose share prices do not fully reflect the ‘intrinsic’ value of their current balance sheet and believe conventional equity valuation principles focus too much on forecasted future earnings.

Performance of Man GLG Undervalued Assets vs sector and benchmark over 5yrs

Source: FE Analytics

“The fund is comprised of two types of company: those trading below the managers’ analysis of their ‘replacement cost’ and those whose profit streams they consider are undervalued by the market. They aim to sell assets as they come to be priced at what they consider to be fair value and to replace them with fresh ideas in bargain territory,” Morgan explained.

Man GLG Undervalued Assets is in the IA UK All Companies sector’s top quartile over one, three and 10 years but is second quartile over five years. Presently, it has significant positions in banks, property, infrastructure, construction and insurance with energy and mining also featuring.

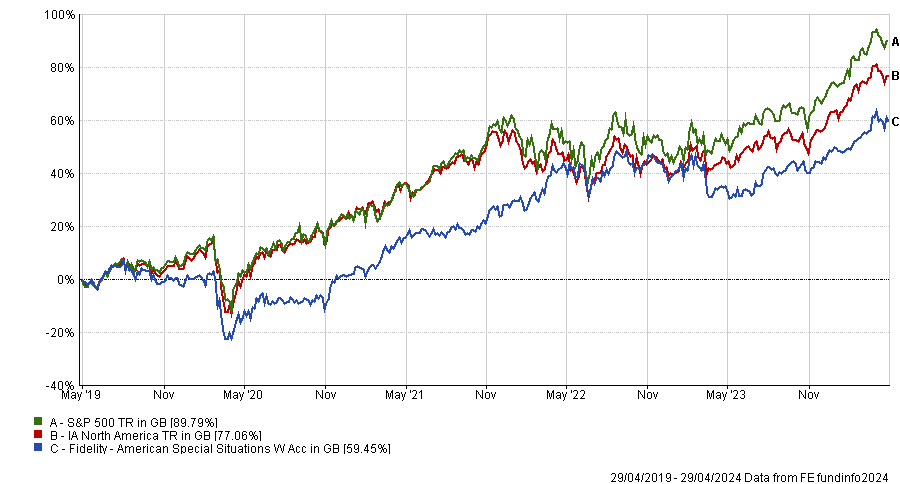

US: Fidelity American Special Situations

In the US, Morgan chose Fidelity American Special Situations, which favours companies that have gone through a period of underperformance and have relatively little value ascribed to their potential. Manager Rosanna Burcheri, who is FE fundinfo Alpha Manager rated, assesses a variety of company factors, including balance sheet strength, asset backing, resilience of the underlying business model and market position, in her investment process.

Performance of Fidelity American Special Situations vs sector and benchmark over 5yrs

Source: FE Analytics

The £633m fund is currently in the IA North America sector’s bottom quartile over five and 10 years but climbs into the second quartile on a three-year view. It’s important to remember that much of the recent past has been dominated by the rise of US large-cap tech companies, many of which are growth rather than value stocks.

“Given the value tilt of this fund we would expect it to have trouble keeping up in an environment where the market is being driven by growth stocks – as has been the case in recent years,” Morgan said. “The fund trades at a sizeable discount to the index on all traditional valuation metrics so it makes a good diversifier to a growth- or tech-orientated US fund.”

Asia: Fidelity Asian Values

In Asia, the pick is the Fidelity Asian Values trust, which was highlighted because FE fundinfo Alpha Manager Nitin Bajaj takes inspiration from legendary US investor Warren Buffett’s style of ‘value investing’, or targeting good companies run by trustworthy management teams and buying them at the best possible price.

Performance of Fidelity Asian Values vs sector and benchmark over 5yrs

Source: FE Analytics

Morgan explained that this often leads the trust to smaller companies that are not widely followed by professional investors and areas that are being widely ignored. Meanwhile, Bajaj likes stocks that display some ‘quality’ characteristics as part of his investment mantra of ‘good businesses, good people and good price’.

Fidelity Asian Values is in the IT Asia Pacific Smaller Companies sector’s second quartile over three years, its fourth quartile over five years but its top quartile over 10 years. The £374m trust is running a large overweight to China (which has struggled in recent years) and financials, consumer discretionary and industrials stocks.

Japan: Man GLG Japan CoreAlpha

Morgan’s final value fund pick is Man GLG Japan Core Alpha, which is managed by Jeff Atherton, Adrian Edwards, Emily Badger and Stephen Harget. It is currently top quartile in the IA Japan sector over one, three, five and 10 years although the Charles Stanley analyst noted that it is not suited to all market environments and can experience periods of underperformance.

Performance of Man GLG Japan Core Alpha vs sector and benchmark over 5yrs

Source: FE Analytics

Man GLG Japan Core Alpha usually performs worse compared to its peers and benchmark when reliable earnings are being prioritised by the market over low valuations. However, Morgan said it is a good option for those who want to invest in unloved Japanese companies or diversify away from the growth style more generally.

He added: “The management team believes cyclicality is a strong influence in virtually every sector of the Japanese market and outperformance can be generated by being contrarian and exploiting extremes of valuation through buying stocks that are unloved and selling them when they become more popular.”

The semiconductor industry is one the most intense in research and development (as a proportion of sales), second only to pharma in 2022.

Semiconductors act as one of the fundamental building blocks for technological advancement. Companies across end markets are continually demanding increasingly complex, high-performing and efficient chips, across an expanding number of applications and different system requirements – all to drive innovation within their own products.

For semiconductors to meet these increasing demands, they need to constantly innovate. At the ‘leading edge’, innovation is focused on shrinking the size of the ‘node’, and thus increasing the number of transistors per chip.

Over several decades, progress in this area has seemingly followed Moore’s Law: that the number of transistors on a chip will double every two years, leading to an exponential increase in computational power and efficiency.

Taiwan Semiconductor Manufacturing Company (TSMC) has been at the forefront of this progress and is able to produce chips at the three nanometre (nm) ‘node’, with a two nm node offering 30% more efficiency expected by 2025.

Even at the ‘trailing edge’ – older, more mature semiconductor technologies – innovation is still important, focused on improving the reliability and efficiency of chips, potentially through material science.

To facilitate this innovation, the semiconductor industry is one the most intense in research and development (R&D) as a proportion of sales, second only to pharma in 2022.

While innovation is clearly a significant cost for semiconductor companies, a high investment allocation to R&D not only creates high barriers to new entrants, but allows the industry to continue growing, not only by providing improved, more complex and powerful semiconductors, but facilitating the development of new technologies in different categories and industries – as seen with the progress made in generative artificial intelligence (AI) across sectors over the course of 2023. Consequently, the semiconductor market has grown rapidly over the past decade.

Two sectors we would highlight where there has been this significant growth in the use of semiconductors are the automotive and datacentre industries.

Growth in the automotive semiconductor end-market (14% annually through 2030), is expected to far outpace the broader sector, with long-term trends such as digitalisation, electrification and autonomous driving increasing the complexity and content of semiconductors within vehicles. Semiconductor content per vehicle averaged around $600-700 in 2021 and is expected to reach $2,000 by 2030.

Semiconductor content roughly doubles from an internal combustion engine vehicle to a battery or plug-in hybrid electric vehicle (EV), and the expectation that EVs (full or hybrid) will make up more than 50% of car production by 2027 is a significant tailwind to demand.

Datacentre semiconductor usage is expected to be the second fastest growth sector over the remainder of the decade (+13% annually). We have seen rapidly increasing demand for cloud computing capacity across industries, not only due to more businesses and industries migrating on-premise infrastructure to the cloud, but the rise of ‘Big Data’ and more data-centric analytics boosting demand for more efficient servers, and thus more complex, efficient and powerful processors.

Furthermore, advances in artificial intelligence, particularly following developments in generative AI during 2023, require specialised hardware that has the ability to handle complex and energy-intensive computations, with datacentres providing the necessary infrastructure for both the training and running of AI systems.

The increasing demands and complexity of the underlying products within these two industries are resulting in greater ‘semiconductor content per device/unit’ (measured as the dollar amount). However, this phenomenon is also present across many other use cases.

Costs associated with fitting more transistors onto a given area are one reason why the semiconductor industry is one of the most R&D-intensive industries. Advancing to smaller technologies becomes increasingly complex, meaning that at each ‘node’ (the minimum distance between transistors on a chip) the cost increase is significant.

Whilst no data is available yet, the three nm node is expected to be $1bn. The more significant cost, however, is the cost of the fabrication module (semiconductor factory), which is expected to be $5-6bn at the five nm node.

The cost of TSMC’s three nm proposed fabrication plant is estimated to be $20bn, highlighting a significant acceleration in the costs required to progress the technology further.

Geopolitical tensions have driven governments to offer significant subsidies to accelerate the onshoring of chipmaking facilities.

The Covid-19 pandemic exposed vulnerabilities in the semiconductor supply chain, with varying lockdown measures across regions driving severe shortages in many areas of the chip markets.

The supply chain disruption exacerbated existing underlying tensions and concerns over national security and supply chain stability. Strained relations between the US and Chinese governments have resulted in sanctions and restrictions over exports between the two countries since 2017, with the US ultimately aiming to limit China’s ability to acquire and manufacture chips at advanced nodes and thus slowing efforts to gain a meaningful foothold in industry and become self-sufficient.

The US’s vulnerability is clear. Whilst accounting for 25% of global semiconductor demand, the US possesses just 12% of global manufacturing capacity. Other regions have also weighed in to obtain their own slice of the rapidly growing and critical industry, with the EU, Japan, Korea and India all offering additional subsidies to incentivise chipmakers to build on their shores.

One concern with government subsidies is that they typically lead to the misallocation of capital. We do not expect this to be the case for the semiconductor industry since the subsidies are coming at a time when companies need to ramp up capacity in order to service the long-term underlying growth trends.

Either way, semiconductor equipment manufacturers such as Lam Research and KLA Corp stand to benefit from these long-term capex cycles.

Despite their superior characteristics, Guinness’ holdings have, on average, typically been in line with the MSCI World Semiconductor Index valuation on a price-to-earnings (P/E) basis.

However, recently a significant discount has emerged. With the exception of Nvidia, all of our holdings are at a discount to the MSCI World Information Technology Index and the MSCI World Semiconductor Index today.

We therefore continue to see good opportunities for holdings in the semiconductor sector and believe they continue to have good pathways for future growth, and potential outperformance.

Dr Ian Mortimer and Matthew Page are fund managers of Guinness Global Innovators. The views expressed above should not be taken as investment advice.

More buybacks mean less dividend growth, Rathbones’ Dobbie explains.

Investors should be prepared for lower dividend growth and special payouts as companies re-direct their leftover capital towards buybacks instead.

Heftier buyback programmes such as the ones UK companies have been carrying out logically result in dividend slowdowns, said Alan Dobbie, co-manager of the Rathbone Income fund.

That’s because when a company chooses to buy back its own shares, the money that it employs to do so cannot go towards special dividend payments or towards increasing the ordinary dividend.

“Companies do have to invest for growth, you can’t just buy back yourself to greatness. But given how cheap so many UK stocks are, it's good that UK boards are thinking about this. Buybacks have had a bad reputation in financial markets but they can make a lot of sense now,” he said.

“However, as a consequence, we’re not seeing the growth in ordinary dividends that we would have done if it wasn’t for share buybacks. They can be a sensible use of capital, but they do add additional pressure on dividends.”

Three things affect the level of dividends, according to Dobbie: the board's confidence in the economic outlook, the dollar-sterling exchange rate, which makes a big difference because many UK companies declare their dividends in dollars, and buybacks.

Since 2020, all three have impacted the UK market, with a sluggish economic outlook, the dollar strengthening and making “quite a big difference” to UK income fund dividend growth, and companies starting to use buybacks “a lot more and quite opportunistically”.

In the past four years, Natwest has reduced its share count by over 20%, and Shell and BP also came close to that figure. The trend is spreading to mid-cap stocks as well, with financial services company IG Group buying back 7.5% of its stock.

“You can calculate a theoretical return on a buyback. For a company like IG Group it's over 20%, so that would be the hurdle rate for any other investment projects they may have,” the manager explained.

“To the management team there, that's a really good use of excess cash, and the question they ask is not ‘why would we do that?’ but ‘why wouldn't we?’”

Dobbie believes that buybacks will continue and could be a potential catalyst to revive the UK market.

“It may be buybacks, it may be mergers and acquisitions that turn things around, or something else entirely. But the much awaited UK comeback might also have already happened – the macroeconomic picture is improving, it looks like we're out of recession, wage growth is at 6% and inflation 3.4%.

“Nobody's going to be waving a flag saying ‘the UK market is now the greatest investment opportunity’ and everybody is going to pile in all at once. It's just a subtle shade less black than the day before and we're more likely to look back in six months or two years’ time and note that the UK has outperformed. At that point, it could be too late already, because things can be quite violent when they turn,” he concluded.

Luckily for income investors, UK dividends don’t seem destined to plummet, despite the uptick in share buybacks.

The latest Computershare Dividend Monitor released last week found the dividends market “healthy but unexciting”, with growth remaining steady at 2% in the first quarter of 2024. The expectation for 2024 is a 1.5% year-on-year increase in regular dividends.

JOHCM UK Equity Income manager James Lowen argued that the impact of buybacks on dividend growth will only be of a short-term nature, with positive repercussions in the long term.

“Over the long term, the anticipated effect is to amplify dividend growth, as there will be fewer shares in issue for a set amount of dividend to be spread across. This is a powerful second derivative effect of buybacks for long-term dividend growth, which we see in numerous stocks,” he said.

“Fund dividend forecasts incorporate a shift towards lower dividends and increased buybacks from 2024, signifying a short-term dip but projecting higher returns in the medium term.”

The manager of the Fidelity European fund explains why investors interested in the defence megatrend should look at the German stock market.

The outbreak of the war in Ukraine has led European countries to reassess their spending on defence and investors to reappraise the pros and cons of defence stocks.

Some believe this could be one of the best investment themes for the long term, but with British defence stocks such as BAE Systems up 194.6% and Rolls Royce growing 290.6% over three years, this investment thematic might well be already on its way.

Performance of stocks over three years

Source: FE Analytics

However, the UK market might not be the right place to benefit from those increase defence spendings, according to Marcel Stötzel, co-portfolio manager of the Fidelity European fund.

One of the reasons is that the UK is already exceeding its NATO commitment to disburse at least 2% of its GDP to keep its military battle-ready. This is also true for France and as such Stötzel does not believe the UK and French defence stocks have much room to grow.

He also highlighted that UK defence companies are more exposed to the US, which he does not see increasing its military spending at the same rate as European countries.

Stötzel said: “The argument that European countries have not, in aggregate, spent 2% of GDP on defence as per NATO guidelines is clear. Some, like the UK and France, have, but others have spent way below that. Germany in particular is the European country that has the most catching up to do.

“The US is not going to see anywhere near that level of increase in defence spending. In my humble opinion, you want to be in and around Germany, because that’s the most obvious candidate for growth in that area.”

However, Germany-listed pure defence names, such as Rheinmetall and Hensoldt have already surged dramatically in recent years and command high multiples. For instance, Rheinmetall trades on a 42x price-to-earnings (P/E) ratio and Hensoldt on 73.7x.

Therefore, Stötzel is not sure whether those stocks are already fully valued or not. Instead, he and FE fundinfo Alpha Manager Sam Morse, have been looking at stocks that haven’t gone up as much yet to try to tap into this theme. This is the reason why they’ve recently added MTU Aero Engines in their portfolio.

Stötzel explained: “It is a German aerospace engine manufacturer, with defence accounting for 10% to 15% of its business.

“Obviously it's not as game changing as if it was a pure defence stock, but we actually like the business as a whole.”

Performance of stock over 5yrs

Source: Google Finance

Beyond defence, Stötzel and Morse have also been looking at the mining sector and introduced Epiroc – a Swedish manufacturer of mining and infrastructure equipment – in the portfolio.

Stötzel explained: “Epiroc makes deep underground mining excavators. If you think about the setup for mining in general, each incremental ounce of ore that comes out of the ground is harder to extract than the previous one.

“That has been a tailwind for Epiroc for many years because it’s becoming increasingly difficult for mining companies to extract ore from the ground. This tailwind is going to be turbocharged by the green transition, as we’re going to need much more lithium, copper and all kinds of different commodities going forward.

“Deep underground mines are the only way to get most of those. For that, you need either Epiroc or their main competitor Sandvik. They are in a duopoly.”

Performance of stock over 5yrs

Source: Google Finance

Epiroc will need to go green itself but Stötzel believes it will enable the company to become more profitable over the long term.

He explained: “Working one kilometre underground with a diesel digger is not great. You need big air filtration systems and it’s tough for your employees. On a 10-year view, Epiroc can go electric and that will be safer and cheaper.”

As a result, Stötzel believes the stock’s dividend could grow at a high single-digit or low double-digit rate over the next 10 years.

Two BlackRock European funds have the best alpha scores in their sector.

One of the main selling points of active investing is fund managers’ ability to beat a reference benchmark, but not all strategies are equally good at that.

Experts measure the success of active decisions through alpha, an indicator for how much a manager has outperformed a relevant index.

Below, we highlight European equity funds that excelled in the past five years by measuring their alpha scores in 61 year-long periods since the beginning of 2018 until today and averaging it.

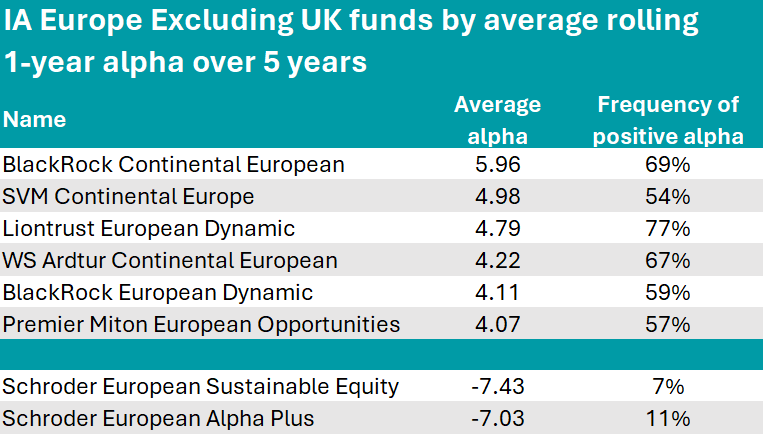

We begin with the IA Europe Excluding UK sector, where the clear winner, standing one whole point above its next competitor, was the BlackRock Continental European fund, with an average alpha of 5.96.

Co-managed by FE fundinfo Alpha Manager Giles Rothbarth and Stefan Gries, this active strategy was described by Rayner Spencer Mills Research (RSMR) analysts as a good core fund.

“BlackRock has an extremely strong European equity team. The two experienced co-managers are backed up by the company’s very large, experienced and stable research resource,” they said.

“Performance has been consistent and the fund is managed with a well-defined investment process which is consistently applied.”

The managers focus on companies with sustainable cash returns and unique franchises. There is a tilt towards growth and a distinct bias towards large-cap holdings, although the fund can invest across all market capitalisations.

Source: FinXL

BlackRock made the list a second time with the BlackRock European Dynamic fund, also managed by Rothbarth. This vehicle is not constrained to any particular style of investing, allowing him the flexibility to take advantage of opportunities.

The fund’s main overweights against the FTSE World Europe ex UK index are consumer discretionary stocks, industrials and technology companies, while it is underweight healthcare and financials.

With an average alpha of 4.79, the £1.4m Liontrust European Dynamic fund stood out for keeping a positive alpha in 47 of the 61 periods considered – the longest among those in the table.

Co-managed by James Inglis-Jones and Samantha Gleave, this five FE fundinfo Crown-rated strategy invests in attractively valued, cash-generating companies run by managers who are committed to using cash flow in an intelligent manner, as noted by Square Mile analysts.

“There is a high representation of quality companies in the portfolio and the longterm performance record of the fund is excellent and suggestive that the managers are identifying anomalously priced securities,” they said.

“We like the managers’ adherence to their process, but this can mean that there will be periods where the market does not reward their stocks. This strategy is unlikely to suit investors who are looking for brief forays into Europe or for those seeking indexlike returns.”

Premier Miton European Opportunities, co-managed by FE fundinfo Alpha Managers Carlos Moreno and Thomas Brown, flanked by Russell Champion, concludes the list.

At the foot of the table, with active portfolio decisions detracting from the funds’ performance, are two Schroders funds, Schroder European Sustainable Equity and Schroder European Alpha Plus, with alpha scores averaging at -7.43 and -7.03, respectively.

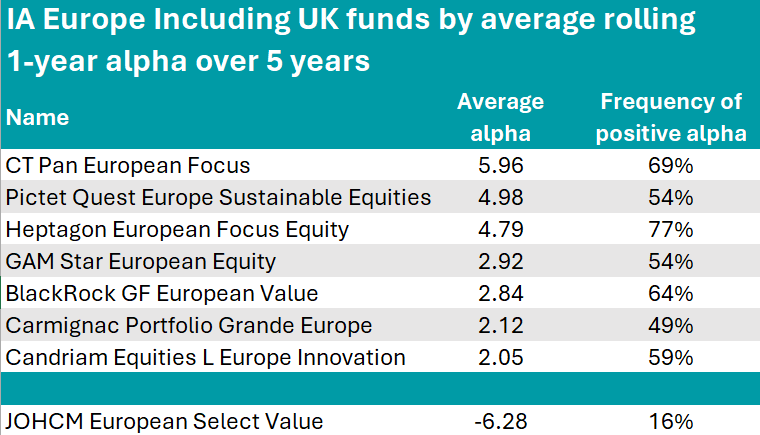

Moving on to the IA Europe Including UK sector, CT Pan European Focus topped the table.

This small strategy, with just £69.4m of assets, is managed by FE Alpha Manager Frederic Jeanmaire, who takes a high-conviction approach, investing in companies whose current share price in his view does not reflect the business’ future prospects.

The portfolio holds 43 stocks, including Rolls-Royce (5.8%), French defence company Safran (5.3%) and French automation and energy management company Schneider Electric (5.1%).

Source: FinXL

The €1.6bn Pictet Quest Europe Sustainable Equities fund was another good performer, achieving a FE fundinfo Crown Rating of five and an average alpha of 5.06. Over the past 61 year-long periods, Laurent Nguyen’s active decisions contributed positively to performance 89% of the time.

Financials and industrials are the key sector exposures, while geographically, the fund is tiled towards the UK (25.7%), Switzerland (15.2%) and France (12.8%).

The €70m Heptagon European Focus Equity managed by Christian Diebitsch came in third with a portfolio of just 22 holdings selected through a bottom-up, low turnover strategy. Its top-three positions are Novo Nordisk (9.3%), ASML (6.7%) and Hermes International (6.2%).

The sore thumb in this sector was the JOHCM European Select Value fund, which had a negative average alpha of -6.28. During the past few years, value strategies in general have struggled.

Sectors previously in this series: UK Equity Income, UK All Companies, Global, Global Equity Income, Sterling bonds, smaller companies, global bonds, cautious funds, balanced and adventurous funds.

After a tough couple of years for sustainable investing, the firm identifies several stocks with the potential to make a lot of money whilst having a positive impact on the world.

Sustainable and impact investment strategies have had a rough few years from a performance perspective, leading investors to question whether it is possible to make money and do good at the same time.

Anna Väänänen, head of listed impact equity at AXA Investment Managers (AXA IM), said investors have “burnt their fingers” in the past two years. “The whole industry has a big issue with performance.”

Investors and clients used to be worried about greenwashing but now they ask more questions about performance. “Now it’s about performance, it’s about tracking error, it’s about the predictability of the performance,” she said.

Some impact investment strategies became unstuck because they invested in small companies that were insufficiently robust to cope with supply chain disruptions following the Covid-19 pandemic, then peak inflation and interest rate hikes.

“They could not swim because they did not have what it takes and they ended up having zero impact,” she observed.

Performance, therefore, was Väänänen’s priority when she joined AXA IM from Mirova in September 2023. She introduced strict minimum criteria for stocks to ensure they fulfil the dual mandate of impact and performance.

Companies must exhibit structural growth, a strong competitive position, operational leverage, a solid balance sheet, proven execution, growing profits and cash flow, a high quality management team and an “interesting” valuation.

Ultimately, she wants to invest in innovative companies that are driving change and are leaders in their sector, be it drug research, precision agriculture or batteries. “We try to identify the leaders of the transition,” she added.

Väänänen helms the People and Planet Equity strategy, which collates the best ideas from three thematic funds: Energy Transition, Social Progress and Biodiversity.

Below, she describes some of her high conviction holdings – companies that have the potential to change the world for the better and at the same time, make a lot of money for their shareholders.

John Deere

The agriculture industry causes 80% of deforestation and uses 50% of habitable land, yet food production needs to increase 50% by 2050 to keep pace with the world’s growing population.

There is a pressing need for agriculture to become more efficient, sustainable and environmentally friendly, and tractor manufacturer John Deere is at the forefront of this.

John Deere has placed cameras in its tractors that take pictures of the ground in real time which are uploaded to the cloud. Artificial intelligence (AI) is used to identify weeds and then the tractor’s sprayer is programmed to target the weeds alone, reducing herbicide use by 70%.

This initiative is creating regular software revenue for John Deere that diversifies its income from sales of large farming machinery. Its tractors can also analyse the quality of soil and then provide nutrients or irrigation in a precise way.

Digital twins

Another theme in the portfolio is the creation of digital twins, enabling anything from medicine to infrastructure to be tested in the digital sphere.

Dassault Systèmes is using a digital replica of the human brain to test neurological medicine and improve its understanding of Alzheimer’s and Parkinson’s disease.

Bentley Systems creates models of the natural environment including ecological data, which it uses to test whether its bridges can withstand extreme weather events. The company also uses its models to research the impact of infrastructure on the natural environment, for instance how would chopping down a forest affect local water levels.

National Grid

National Grid may be listed in the UK but more than half its business is on the US east coast, where the grid network is suffering from years of under-investment. National Grid is upgrading the grid system to protect it from natural disasters and to incorporate renewable energy.

SAP and tech exposure

About 30% of the People and Planet Equity strategy is held in IT and software but that is a broad church. “I don’t want to go too much into any one theme but the truth is that IT is driving change at the moment,” Väänänen said. “If you want to have impact then IT, healthcare and industrials will be the core three elements.”

SAP is an example of a tech stock in the portfolio with sustainable credentials. It provides software to help companies with nature-based reporting and it is a leader in enterprise resource management. SAP has been moving its licences to the cloud and has enhanced its growth prospects by cross-selling products.

The level of the credit spread, which represents the premium for taking on additional risk of default, is eye-wateringly low.

High yield and investment grade credit markets continue to look very attractive on a multi-year horizon. In fact, we find the market as attractive as it has been in nearly two decades. High yield looked great at the tail end of 2023 with the yield-to-worst on the Bloomberg US High Yield Corporate Index pushing over 9%.

At end of March 2024, it was 7.7%, which is still above 15-year averages. Likewise, yields in investment grade credit also look appealing. The yield-to-worst on the Bloomberg US Corporate Investment Grade Index is above 5%, again a multi-year high. This still represents a good starting point and is also one of the main reasons we are positive on bonds this year.

Spreads are skinny, which may become an issue if we don’t achieve the immaculate disinflation

Within credit markets however, the level of the credit spread, which represents the premium for taking on additional risk of default, is eye-wateringly low. Looking at the Bloomberg US High Yield Corporate Index, credit spreads sit at 320bps, which is the lowest that it has been in the past 15 years.

In an asset class such as high yield, this is important as it is the asset class at most risk of defaults. The picture is exactly the same when we look at investment grade credit.

This differentiation between yields and spreads has been very topical in the past 12 months. We realize that the attractiveness of fixed income is the all-in starting yields. It is important to be aware, however, that of this headline yield, credit spreads now represent a smaller proportion compared to history.

To put it in perspective, credit spread is only 42% of the overall yield that we can now extract from the high yield market and the rest is from government bonds. And the picture is even more stark in investment grade credit, where spreads are just 17% of the overall index yield.

Why does this matter?

We are not bearish on the economic outlook per se. In fact, we think growth will be reasonable going forward. However, we are aware that corporate credit is a ‘mean reverting’ asset class. There is a minimum amount of default risk that needs to be baked into credit spreads in order to compensate us as investors for that risk.

We never know what the future holds, but we know that when we see these levels of credit spreads, the cushion that we have in credit markets against any sort of exogenous shocks is minimal. In other words, it could take very little in the news for the market to suddenly wake up and panic and for credit spreads to sell off.

Furthermore, at current spread levels, we think that the market is pricing in an immaculate disinflation ahead of us, the Federal Reserve manages to achieve the perfect soft landing, and inflation lands at 2% in the next year, while employment and growth remain resilient.

This certainly is one of the possibilities. In fact, this scenario has increased in probability exponentially over the past 12 months. However, it is not the only scenario and there are a few more possible paths that the global economy can take.

Not all of them have the same probability of occurring. What is important, however, is that any other economic scenario ahead of us could prove that either government bonds, high yield or investment grade credit (if not all) are incorrectly priced at current valuations.

Possible scenarios – four scenarios among many in 2024:

Being very flexible is key to capturing attractive bond yields while navigating pitfalls. When we look at the bond market, we see multi-year wide index level yields. However, we also see multi-year tight credit spreads that could sell off in all but one scenario.

This makes us want to: 1) definitely be exposed to bond markets in order to extract that yield that we have not seen in decades but, 2) we want to be exposed to the part of the markets that looks cheaper (yields), while minimizing exposure to the part of the market that looks like it has little further room to outperform (spreads) at this point in time.

For this reason, in our strategic bond strategies, we maintain a headline yield of near 7% in the portfolios but have tactically reduced our credit risk exposure at the moment. We do not have an immediate catalyst for a spread sell-off, however we know that one always comes.

We stand ready to increase our credit risk once we see better compensation for default risks, while in the meantime we continue to enjoy the overall high income that we can now extract from bonds.

Alex Pelteshki is co-manager of the Aegon Strategic Bond fund. The views expressed above should not be taken as investment advice.

For investors who believe there is more room to rally, there are some options worth looking at, says Kate Marshall.

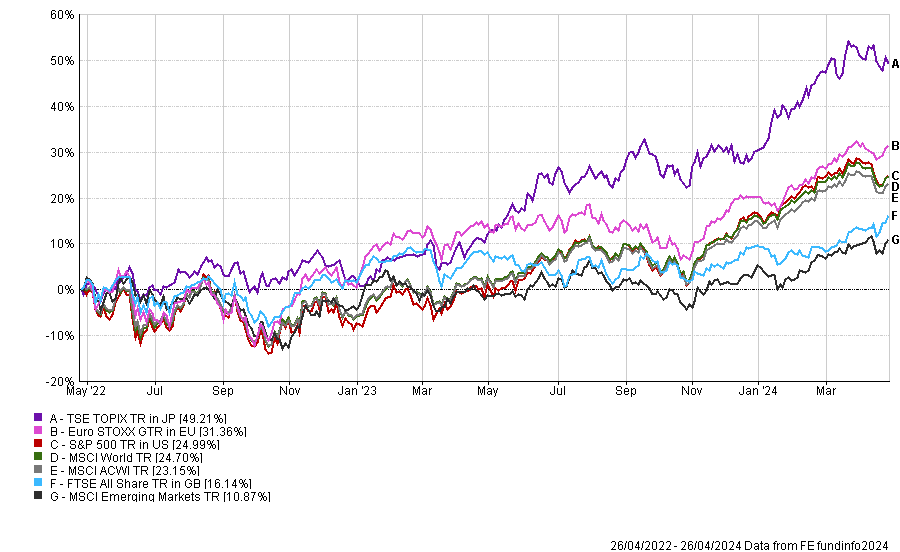

Japan’s stock market has been on a trajectory of new heights, with the Nikkei 225 index hitting an all-time record high this year – the first time it has achieved this in 34 years.

Yet much of the returns have been in local currency thanks to the weakening of the yen. Indeed, over two years, the TSE Topix index – another popular Japan equity benchmark – has been the best performing major market in local currency terms, as the below chart shows.

Its 49.2% gain is almost double that of the much ballyhooed US S&P 500 index, while the European Euro STOXX index took second place, up 31.4%.

Performance of indices over 2yrs

Source: FE Analytics

For UK investors the returns have been more muted. In sterling terms, the Japan index drops down the pecking order substantially.

Indeed, Euro STOXX is top with a return of 33.4%, followed by the S&P 500 (26.6%) and the broader MSCI World (24.2%), which is largely dominated by the US names. The TSE Topix sits in fourth with a total return of 22.2%.

Despite this, returns have still been strong. Kate Marshall, lead investment analyst at Hargreaves Lansdown, said investors will now have to ask themselves whether they’ve missed the boat or if Japan’s market has further to go.

“Like the US, which has been led by the ‘Magnificent Seven’, Japan has benefited from a narrow group of stocks performing well, dubbed the ‘Seven Samurai’. This includes some of Japan’s largest companies, including car maker Toyota and semiconductor companies such as Tokyo Electron,” she said.

“In some cases, their valuations have become stretched. But this doesn’t apply to the entire market. Small and medium-sized companies, on average, currently look better value. And, as a whole, Japan’s market still looks good value compared with other global markets and its own history.”

There could be more catalysts for future growth ahead. For example, Marshall highlighted the end of negative interest rates earlier in 2024 could be followed by another rate hike later in the year if inflation remains around 2% and wages continue rising.

“This could be good news for economic activity, partly because there’s a huge amount of savings in Japan, most of which hasn’t been earning anything in interest. Higher rates could change this, boosting spending and stimulating the economy,” she said.

“However, higher rates could mean that cash becomes more attractive relative to equities for local investors, as we have seen in the UK in recent years – it is a fine line that the central bank will have to navigate.”

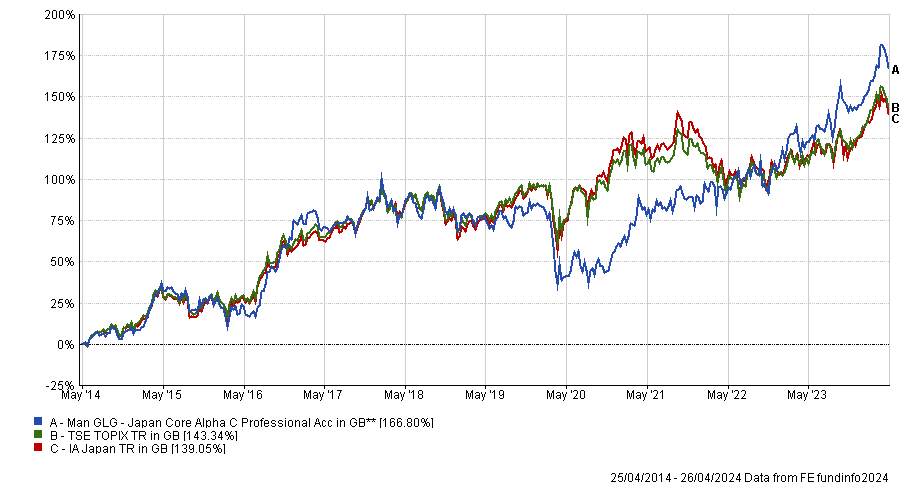

For those wishing to get in now, Marshall highlighted three potential fund options. The first is Man GLG Japan Core Alpha managed by Jeff Atherton and Adrian Edwards alongside recently appointed co-managers Emily Badger and Stephen Harget.

The £2.2bn fund focuses on larger Japanese companies, using a contrarian approach often known as 'value investing'. They buy out-of-favour companies and gradually sell them as they recover.

“The fund could work well in a global equity portfolio designed to provide long-term growth. Its focus on large companies means it could sit well alongside a Japanese equity fund focused on medium-sized or smaller companies,” she said.

The Man GLG fund has been a top-quartile performer in the IA Japan sector over one, three, five and 10 years and was the third best performer since April 2021.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

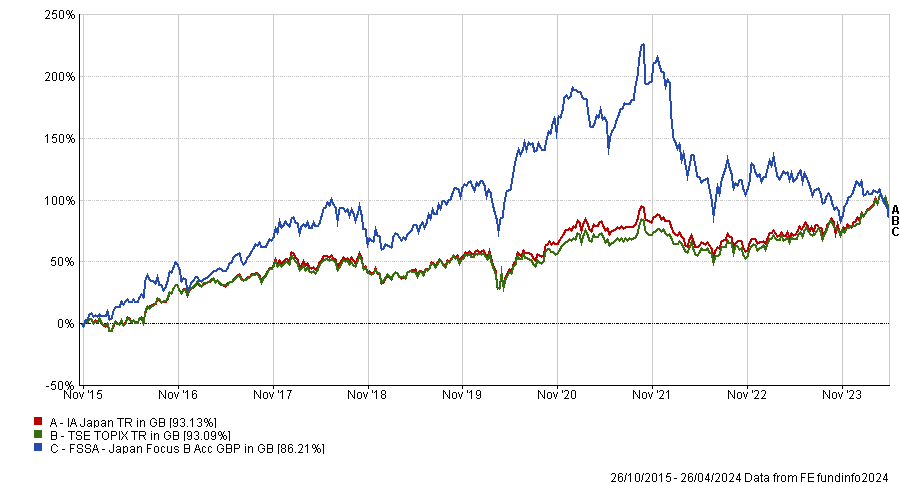

Second is FE fundinfo Alpha Manager Martin Lau and Sophia Li’s FSSA Japan Focus fund. At £81.6m it is much smaller than its Man GLG rival.

It invests with a quality-growth style across the large and mid-cap range of the market, as well as backing more domestically focused Japanese businesses.

“The fund could help diversify a global investment portfolio. Its focus on high-quality companies with the potential for above-average earnings growth means it could work well alongside other value-focused funds,” said Marshall.

It’s performance however has not been so sharp. Indeed it has been a bottom-quartile performer in the IA Japan sector over one, three and five years. Much of this has been over the short term, with the fund down 9.6% in just the past month.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

Over three years it has lost 31.3%, although since launch in 2015 it has done slightly better, climbing to the third quartile of the sector. A year ago, the fund had been the fourth best performing fund in the sector – before its recent fall from grace.

Lastly, for those unwilling to take the risk with an active manager, iShares Japan Equity Index is Marshall’s preferred option for simply tracking the market.

“It provides low-cost exposure to large and medium-sized companies in Japan and aims to track its benchmark, the FTSE Japan, by investing in every company in the index,” she said.

“An index tracker fund is one of the simplest ways to invest. This fund could be a great, low-cost starting point to invest in Japan in a portfolio aiming for long-term growth.”

Alpha Managers Peter Rutter, Nico de Walden and James Clarke are setting up shop together, having generated top-quartile returns for RLAM.

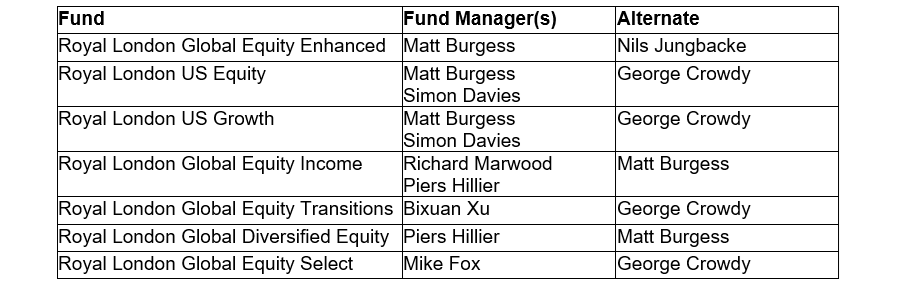

Peter Rutter, head of equities at Royal London Asset Management (RLAM) and an FE fundinfo Alpha Manager, is leaving to start his own business. Four RLAM equity fund managers are joining him: Alpha Managers Nico de Walden and James Clarke, along with Chris Parr and Will Kenney.

Piers Hillier, RLAM’s chief investment officer, will take over from Rutter at the helm of the global equity team. In this capacity, he will be supported by three senior colleagues: Matt Burgess, head of quant strategies; Richard Marwood, co-head of UK equities; and Mike Fox, head of sustainable.

Rutter, Clarke and Kenney manage the £4.9bn Royal London Global Equity Diversified fund and the £803m Royal London Global Equity Select fund. Both funds have generated top-quartile returns over one, three and five years. They have FE fundinfo Crown Ratings of four and five, respectively, in recognition of their high alpha, low volatility and consistently strong performance.

De Walden manages the £1.2bn Royal London Global Equity Income fund, which is a top-quartile performer over one and three years with a five-crown rating (the top score), while his £1.2bn UK Equity Income fund is top quartile over one, three and five years with a four-crown rating. He also runs the Royal London £1.3bn UK Dividend Growth fund, which is a top-quartile performer over one and five years but second quartile over three years.

Parr runs the £369m Royal London US Growth Trust, another fund that is top quartile over one, three and five years, as well as RLAM’s US equity strategy.

RLAM announced leadership changes to some of its funds as a result of the departures.

Hillier will take over the popular Global Equity Diversified fund from Rutter, Clarke and Kenney, with Burgess as his deputy. The Global Equity Select fund has been handed to Fox, with George Crowdy as back-up. A full list of manager changes is below.

Hans Georgeson, RLAM’s chief executive, said: “We remain committed to offering a first class equity capability and will continue to invest in the team. Piers brings huge experience to the leadership of our global equities capability, supported by an extremely talented team that also bring many years of expertise in equity markets.”

China, India, South Korea and Indonesia all received votes.

If you had to invest in just one country, which one would you pick and why?

Trustnet posed this question to the nominees for the FE fundinfo Alpha Manager awards in the emerging markets and Asia Pacific (ex-Japan) category. All four managers and teams who answered picked a different country but what they had in common was an emphasis on finding high quality but underappreciated companies.

Invesco’s Charles Bond: South Korea

“Given our contrarian and valuation-focused approach, we would choose South Korea as our favourite market,” said Charles Bond, who co-manages Invesco Global Emerging Markets. The fund has more than 15% in South Korea (a 4% overweight versus the benchmark).

“South Korean shares are some of the cheapest in the world, with both world leading businesses (e.g. Samsung and Hyundai) and domestic sectors (financials) trading at steep discounts to peers elsewhere in the world,” he explained.

“Many of our South Korean holdings trade on fractions of book value, often with underappreciated asset values (cash, land or stakes in affiliates) and dividend yields of 6%-plus. Dividend yields are compelling, not because pay outs are high but because valuations are low, with plenty of room for dividend growth if pay outs continue to rise, as they have been in recent years.

“Perceptions of lower corporate governance standards are the main reason for this extreme cheapness in our view. However, we believe minority shareholder rights have been improving over the last decade, with the government’s recently unveiled ‘Corporate Value-Up’ programme providing a significant stimulus for this trend.

“Emulating measures in Japan, the South Korean government is seeking to improve corporate returns on equity following the growth of domestic equity ownership, which should boost stock market valuations.”

GQG Partners: India

GQG Partners Emerging Markets Equity has a 30% allocation to India, held in 18 companies spread across eight sectors.

Rajiv Jain, Brian Kersmanc and Sudarshan Murthy, who run the fund, have been overweight India for some time, reflecting their belief that many companies in India are exhibiting “a high potential for durable future earnings growth while trading at attractive valuations”.

“We believe India is in the early stages of credit, property and infrastructure cycles that will drive economic growth, improve the country’s competitiveness on the global stage and increase the earnings power of select companies,” they said.

Fidelity International’s Nitin Bajaj: Indonesia

Nitin Bajaj, who manages Fidelity Asian Smaller Companies and Fidelity Asian Values, said he does not pick countries and that regional allocations in his funds are just an outcome of stock selection. “My process is to construct a portfolio bottom-up, owning a bunch of good businesses, run by good (competent and honest) management teams at a good price that offers ample margin of safety,” he explained.

However, he is finding a lot of opportunities in Indonesia, where the stock market “provides the best mix of growth, quality and valuations” that are integral to his investment approach. “As a result, the fund’s exposure to Indonesia is at its highest over 10.5 years of my management tenure.”

Bajaj has invested in a “mix of banks and select consumer companies that offer fairly high and sustainable returns while being available at reasonable valuations”.

“Indonesia has some of the strongest banking franchises with conservative underwriting culture. They have stable asset quality and benefit from structural growth as penetration levels are increasing from low levels,” he explained.

“The consumer companies we own in Indonesia are also high-quality franchises with market leadership. This gives them strong pricing power and ability to generate margins that are higher than global peers over the long term.”

AllianceBernstein’s Sammy Suzuki: China

Sammy Suzuki, head of emerging market equities at AllianceBernstein, picked China.

“While we do not expect a quick recovery at a macro level, China is home to over 700 listed companies only counting those in the MSCI index. The question for us is whether we can find attractive companies. With significant pessimism, the market offers very attractive yet overlooked investments,” he explained.

The AB Emerging Markets Low Volatility Portfolio, which he manages, is modestly overweight China.

“The transition towards green energy perversely should be positive for energy and materials given restricted supply. This would benefit commodity exporting countries. At the moment, we believe that investing in those commodity-exporting countries offers better risk/reward than investing in commodity companies,” he said.

Suzuki has a positive outlook for emerging markets more broadly as the twin headwinds of rising global rates and a strong US dollar moderate.

“Many emerging market companies are capitalising on structural trends such as innovation in artificial intelligence (AI) and digitisation, deglobalization and reshoring, changing consumption behaviour and the energy transition – often at lower valuations than their developed market counterparts,” he pointed out.